TradFi Adopted Crypto's Technology, But Not the Libertarian Dream

TradFi will be the beneficiary of the last decade of crypto evangelism.

I post daily, but deliver to your inbox every Sunday. Browse past newsletters HERE. Book Rich. Bring the speed of Asia to your next event HERE

Read me first

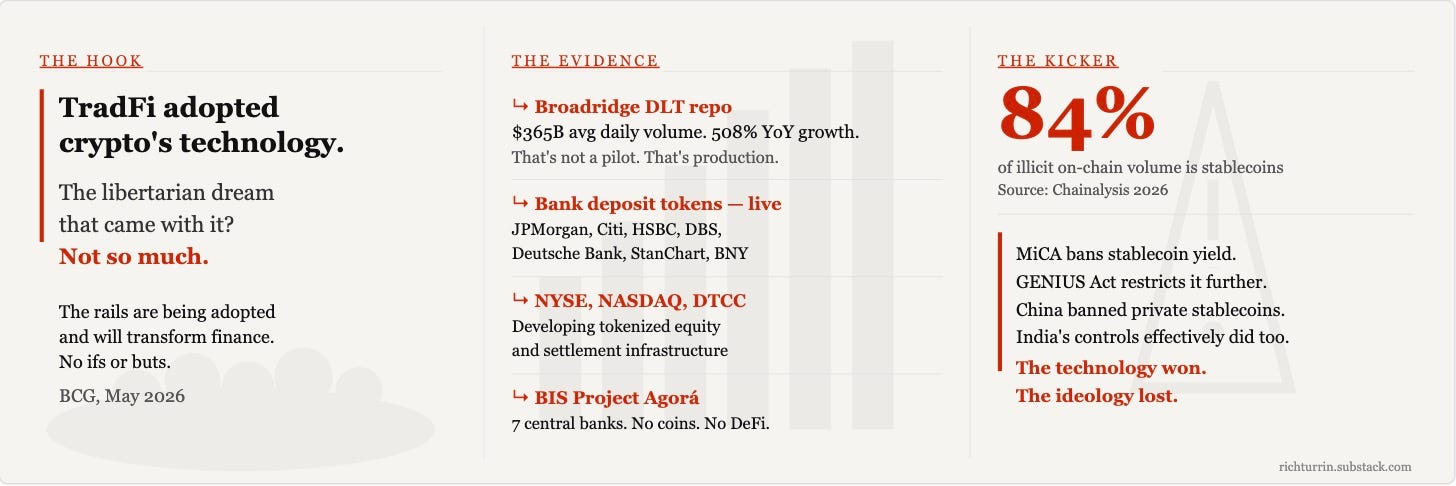

BCG just confirmed what many of us have suspected: crypto technology is winning, but crypto itself is the odd one out.

The technology and rails are being adopted and will transform finance, no if’s or buts. The coins, not so much.

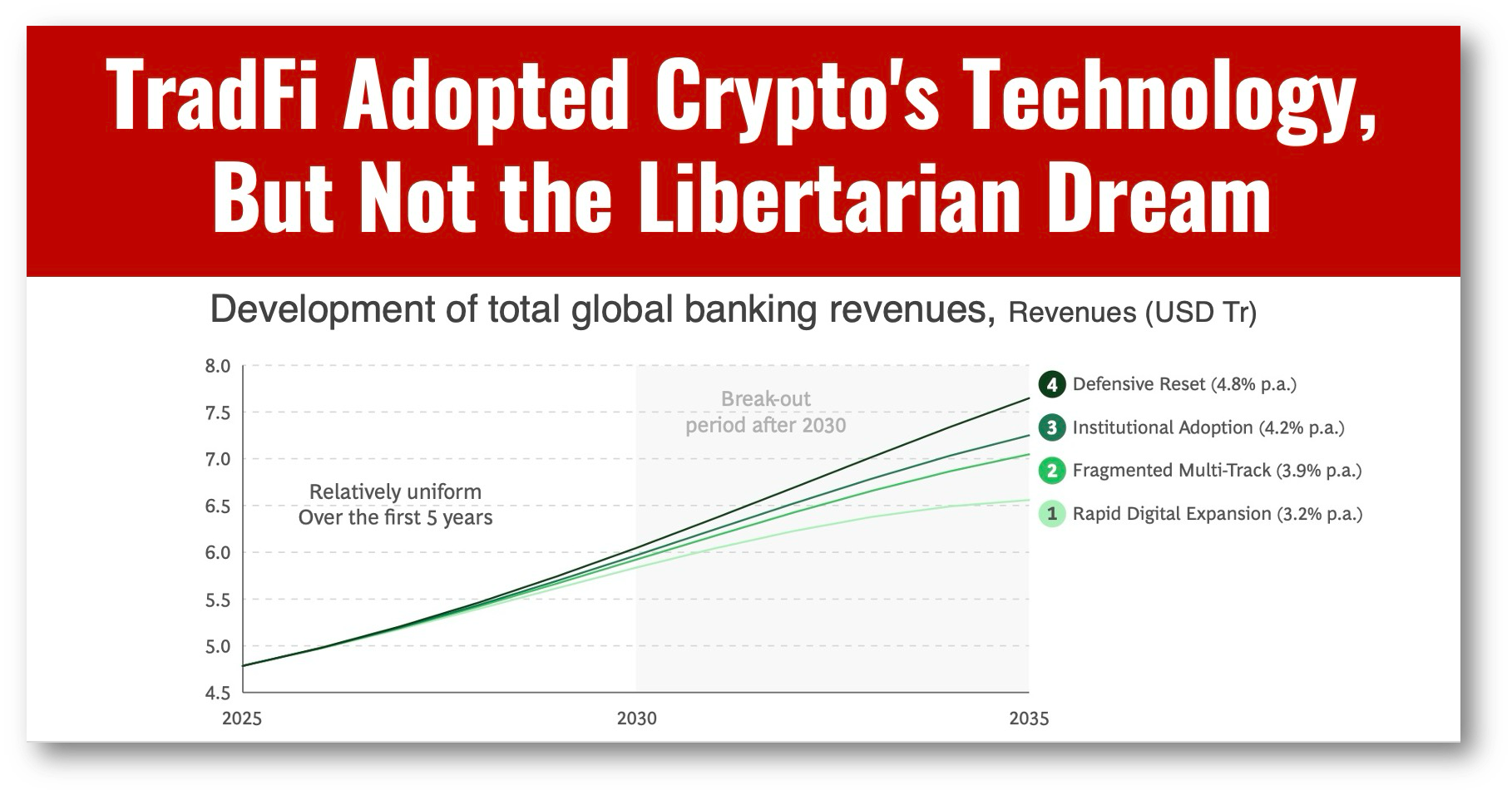

BCG’s May 2026 flagship report, “The Future of Digital Assets,” maps four scenarios for how this plays out, and none of them are the libertarian dream that crypto espoused just a few years ago.

What’s emerging is institutional capture of DLT infrastructure, with banks deciding the terms of engagement.

The tension at the heart of the report is whether DLT is destined to become a better plumbing layer for the same old financial system, or a genuinely new architecture?

BCG calls this the “meta-level question” and refuses to answer it.

I’m less shy and will say that it’s much better plumbing for TradFi, because regardless of whose rails are used tradfi will ultimately control access. They are not loosening up their grip.

Here’s what that looks like across BCG’s four scenarios:

1️⃣ Private-led expansion — Stablecoins reach 10-20% of M2. Challengers and DeFi win. Traditional banks face 10% smaller balance sheets, 14% lower revenues, 30% lower profits by 2035 versus the no-digital-asset base case.

2️⃣ Fragmented multi-track — Everyone builds, nobody connects. Regional banks and local challengers gain ground. Global platforms lose. Liquidity pockets form, not markets.

3️⃣ Institutional digital evolution — Tokenized deposits and wholesale CBDCs dominate. Global G-SIBs and large asset managers win. DeFi loses. This is the BIS “unified ledger” scenario wearing a business suit.

4️⃣ Constraint and defensive reset — Regulatory backlash or a larger crisis resets the whole experiment. Conservative incumbents survive. The innovation ecosystem doesn’t.

Institutional use cases for crypto technology are impressive and clearly going mainstream:

↳ Broadridge DLT repo: $365 billion average daily volume, 508% year-on-year growth

↳ J.P. Morgan, Citi, HSBC, DBS, Deutsche Bank, Standard Chartered, BNY — all live on tokenized deposits

↳ NYSE, NASDAQ, and DTCC are developing tokenized equity and settlement infrastructure

Still, this is not the DLT the crypto natives imagined.

The regulation that the crypto community touts as crypto going mainstream also brings the cage of securities and banking regulation.

The best example are stablecoins. The freedom that defined stablecoin’s early days is quietly being legislated away: MiCa, the GENIUS Act, China’s ban, and India’s currency controls shut off both economies.

Can anyone blame them when stablecoins now account for ~84% of illicit on-chain transaction volume globally?

So yes, stablecoin regulations are legitimizing the tech, but also removing its regulatory arbitrage advantage, and reducing its use in fraud.

But the most important project of all that crypto was not invited to? BIS Project Agorá connects seven central banks using tokenized deposits. DLT architecture, purpose-built to reinforce the existing two-tier banking system.

Agora has no coins/tokens, no decentralization, and most definitely no disintermediation.

The technology won. The ideology lost.

That’s why, at Bangkok’s Money 20/20, stablecoin purveyors are now dressed in jackets, courting bank clients, not crypto whales.

Which brings us to the real question the report doesn’t dare ask:

If crypto technology wins but the coins lose, who actually benefits from a decade of crypto evangelism?

Is it the banks that waited on the sidelines before adopting it, or the builders who paved the road?

👉A Ten-step Guide to Managing Digital Assets

Make an explicit strategic choice — pick a base-case scenario and define your ambition: defensive participation, scaled competition, or infrastructure shaping.

Quantify what is at risk and what is addressable — model revenue pools at risk, revenue pools addressable, and capital and liquidity effects under tokenized settlement. Without numbers, digital assets stay abstract.

Decide where to compete in the stack — client interface, product layer, or infrastructure. Multiple pilots without architectural coherence is a strategic error.

Protect the core while building the future — reassess liquidity stress assumptions, intraday funding requirements, and collateral mobility impacts. Parallel rails will exist for years.

Elevate risk and custody to first-order strategy — clear intervention authority, wallet-based AML monitoring, and explicit governance over key management. In programmable markets, controls sit inside the product, not around it.

Architect for optionality, not prediction — modular ledger-agnostic architecture, vendor exit paths, configurable compliance controls. Lock-in converts uncertainty into structural dependency.

Sequence with discipline — avoid isolated pilots and uncontrolled scaling. Speed matters, but architectural integrity matters more.

Align governance with automation speed — assign one accountable executive sponsor, centralize DLT platform ownership, institute board-level review tied to scenario monitoring.

Choose your ambition archetype — defensive integrator, scaled participant, or infrastructure shaper. Drift between models is the highest-risk posture.

Revisit core assumptions annually — where does irrelevance risk exceed execution risk? Are you preserving optionality or accumulating hidden lock-in?

HAND CURATED FOR YOU

🚀 Asia moves fast. So does this newsletter. I curate only the best fintech, CBDC, and AI insights from 50+ sources weekly so you stay ahead of what’s coming West. Subscribe and never fall behind.

If you know someone who would like this newsletter, please share it with them and help grow our Asia, CBDC, and AI aficionados community!