Asia's WealthTechs Vie For a $700bn Bonanza

Fierce market competition will cut asset management fees to the bone.

Asia is becoming wealthier by the day, and in the next five years, an astounding $700 billion in personal finance assets will be looking to WealthTechs to manage their money.

In yesterday’s article (below), I showed how Asia is leading the West payment innovations. Today, we see how Asia will eventually do the same with WealthTech.

One driver for the WealthTech boom is that younger, newly affluent clients are comfortable with mobile-based wealth managers. This is creating a battle for assets that high-fee incumbents can’t win.

That’s why Asia’s incumbent banks and wealth managers would be wise to partner now with WealthTechs or prepare for even bigger losses in the future.

Once these clients are gone, they will never return; certainly, none will ever pay high fees!

👉TAKEAWAYS

🔹 Digital First Asia is pushing wealth tech:

➣80% of respondents expressed a clear preference for leveraging digital solutions

➣59% citing benefits such as cost-effectiveness

➣61% greater transparency and control

➣57% personalized investment strategies.

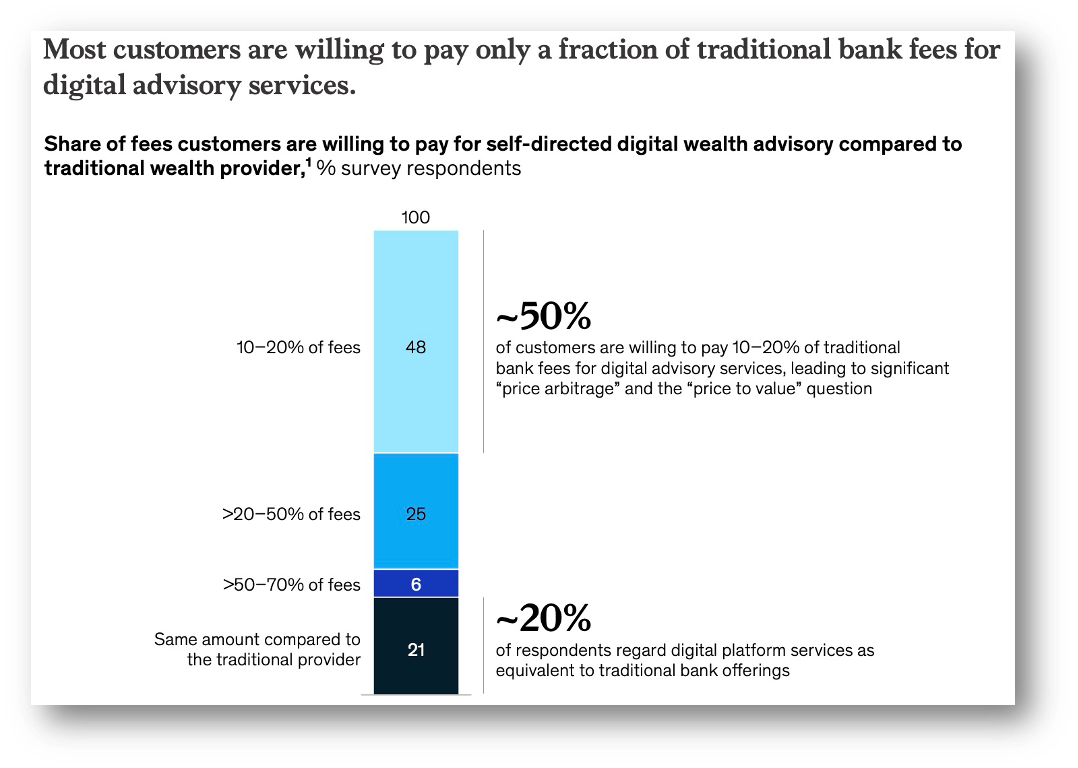

🔹But young digital customers demand cost-efficiency

➣🔥50% of the survey respondents said they were willing to pay only 10 to 20 percent of the fees charged by incumbents!🔥

➣Most of these respondents were younger than 45 and within the mass and affluent segments.

🔹 And many still need human assistance:

➣80% of respondents said they trust digital wealth platforms,

➣45% reported they still prefer some form of human assistance for complex decisions

👊STRAIGHT TALK👊

McKinsey does a great job showing the changing societal perception that digital financial services are as safe and reputable as incumbents.

This change in perception, particularly for younger investors, shows how the “fear factor” over digital financial services is declining fast.

However, McKinsey misses how Asia’s payment services contribute to WealthTechs and the normalization of using digital financial services.

The biggest contribution instant payment platforms make to WealthTech is making it easy to move money.

Digital payments mean there is no longer the need to tie your money to a single financial provider out of convenience, bringing a decreased sense of customer loyalty.

That decrease in customer loyalty will hit both incumbents and WealthTechs hard.

Incumbents will have a hard time convincing clients to pay their high fees, while WealthTechs will be under constant pricing pressure to cut fees to the bone.

If this sounds like a harsh environment for Asia’s WealthTech, it is! The only way out of this is to innovate, and that’s what Asia is good at.

Please restack!

Readers like you make my work possible! Subscribing is free, and I use the same business model as public broadcasting, where you can get all of my writing for free. If you like the content, please buy me a coffee by subscribing. Thank you!

Sponsor Cashless and reach a targeted audience of over 50,000 fintech and CBDC aficionados who would love to know more about what you do!