Bank Innovation Lags Behind: Running to Stand Still

Banks still struggle with the basic building blocks of our digital world.

Banks are running as fast as they can with their digital innovation, but most are standing still as the digital world speeds by them.

The “Innovation in Retail Banking Report” is a great read and shows how banks, after over a decade of digital transformation, are still struggling.

That isn’t to say bankers aren’t working hard; they likely are, and a small group (11% in the chart above) are doing well. That leaves 16.4% in the “loser zone” and 69.1% in “Limbo.” Being in limbo means they have no discernable trend that allows us to predict whether they will be winners or losers.

What is shocking is that, given the amount of time banks have had and the number of management consultants who have impressed upon them the importance of digital, the vast majority are behind.

The recommendations for how banks need to “drive their innovation agenda” remain the same today as they did a decade ago. The advice doesn’t change and focuses on banks being Agile, changing their People and Culture, and building Ecosystems. While bank culture may be changing, it is a slow process, and the vast majority don’t do anything fast, which kills most agile processes. Building ecosystems is a tough job for the majority of banks that are digitally behind.

Banks’ inability to do anything fast is a serious problem. They are “running to stand still” while their customers have ever higher digital expectations. This is a real problem because while a bank may tout its latest digital feature, customers' response may be, “So what?” Access to all of big tech’s latest products has turned customers into digital connoisseurs and big techs encroachment into banks’ payment territory doesn’t help.

Banks, for the most part, are focused on better digital offerings, becoming a financial marketplace, or building digital advisory services. These are certainly reasonable aspirations if they can handle the basic technology required to pull this off.

I am stunned that 28.5 percent of respondents want to build a superapp, given the impossibility of success and the herculean nature of the task. Why do bankers waste their time on superapps? It is an interesting fixation that, as we’ll see in the next chart, is completely unrealistic.

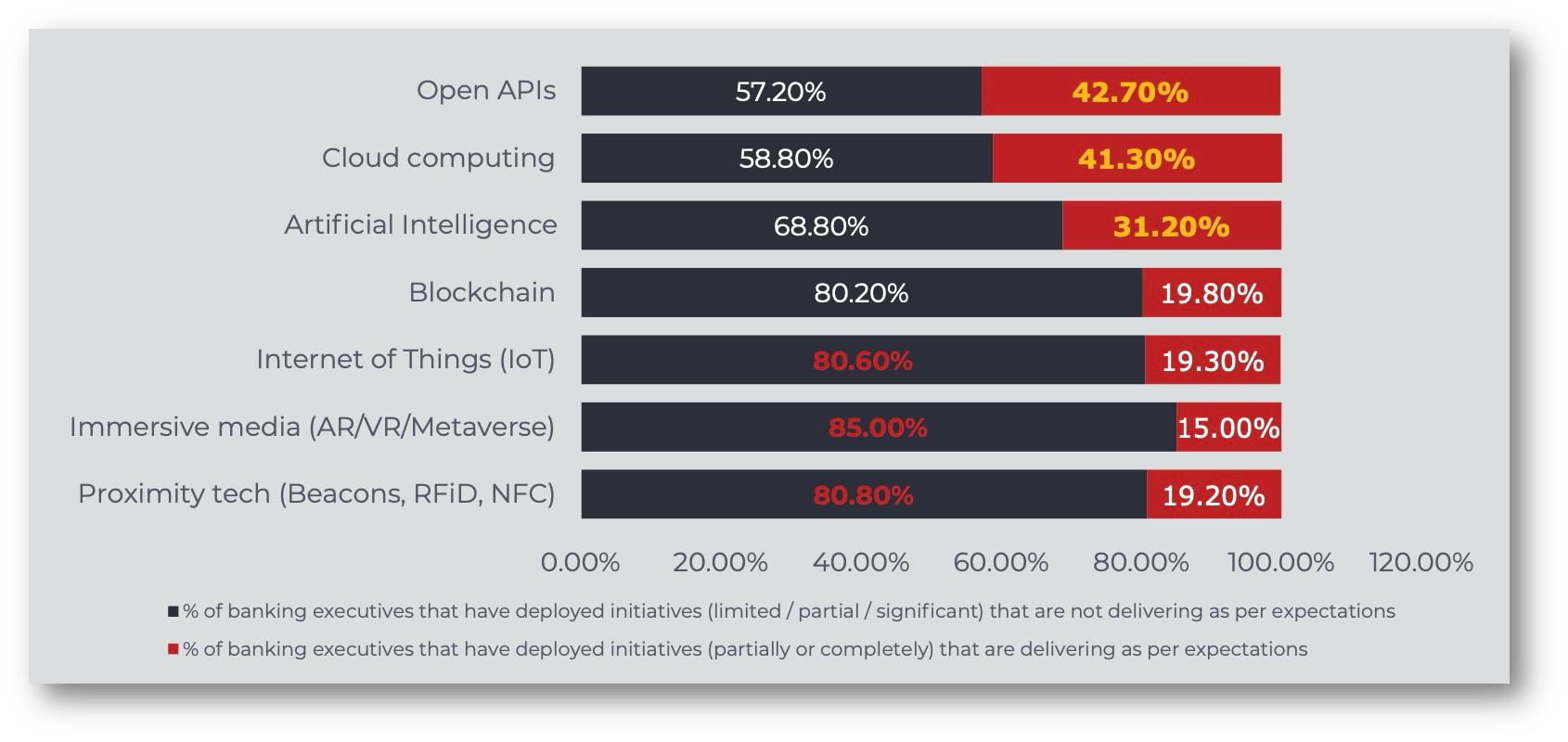

Now, for those who say I’m being too harsh on banks, look carefully at the chart above: 57% of banks can’t even build an “open API” that works to expectations, and 58% have difficulty with the cloud.

Consider these numbers and think that nearly a third of bankers want to build a superapp? Are you stunned at the level of disconnect? I am!

How can many of these banks achieve their stated goals of building digital marketplaces and advisory without mastering the most basic building blocks of our digital world?

The chart above provides further proof of banks’ innovation difficulties. It shows how digital initiatives are not delivering as expected in virtually every business category except for one of seven.

As the author of a book on innovation, failure or not delivering as expected doesn’t always mean disaster, and some of these banks may turn their innovations into success. So I will try to be the optimist.

Banks are behind in so many areas of innovation and having so much difficulty mastering basic digital skills that it shows that they are running to stand still.

Readers like you make my work possible! Please buy me a coffee or consider a paid subscription to support my work. If neither is possible, please share my writing with a colleague!

Sponsor Cashless and reach a targeted audience of over 55,000 fintech and CBDC aficionados who would love to know more about what you do!