Banks’ Timely Counterattack: RLNs As Innovation Platform Not CBDCs

Bank Regulated Liability Networks counter CBDC disintermediation

UK Finance released the results of the experimentation phase of the Regulated Liability Network (RLN) and found that RLNs are a viable innovation platform that provides real benefits to users.

While I couldn’t agree more, that RLNs provide a giant leap forward in settlement technology, I can’t help but view them as banks’ response to the threat of disintermediation from CBDC.

While RLNs provide capabilities beyond CBDCs and are, in essence, a tokenization platform for all regulated assets, not just bank deposits, banks wouldn’t be pushing them without the threat of disintermediation, and their end game is to ensure bank domination of the sector.

Whatever you think of CBDC, they deserve a debt of gratitude as they provided the impetus for banks to pursue this welcome modernization of their payment and settlement infrastructure.

👉TAKEAWAYS

🔹 Platform for innovation:

-The key conclusion from the Regulated Liability Network (RLN) Experimentation Phase is clear: the UK could benefit from a platform for innovation that delivers functionality not currently available in the market.

-The platform for innovation does not aim to be the sole solution in the payments industry; rather, it seeks to complement and function alongside other existing initiatives to enhance the overall payments ecosystem.

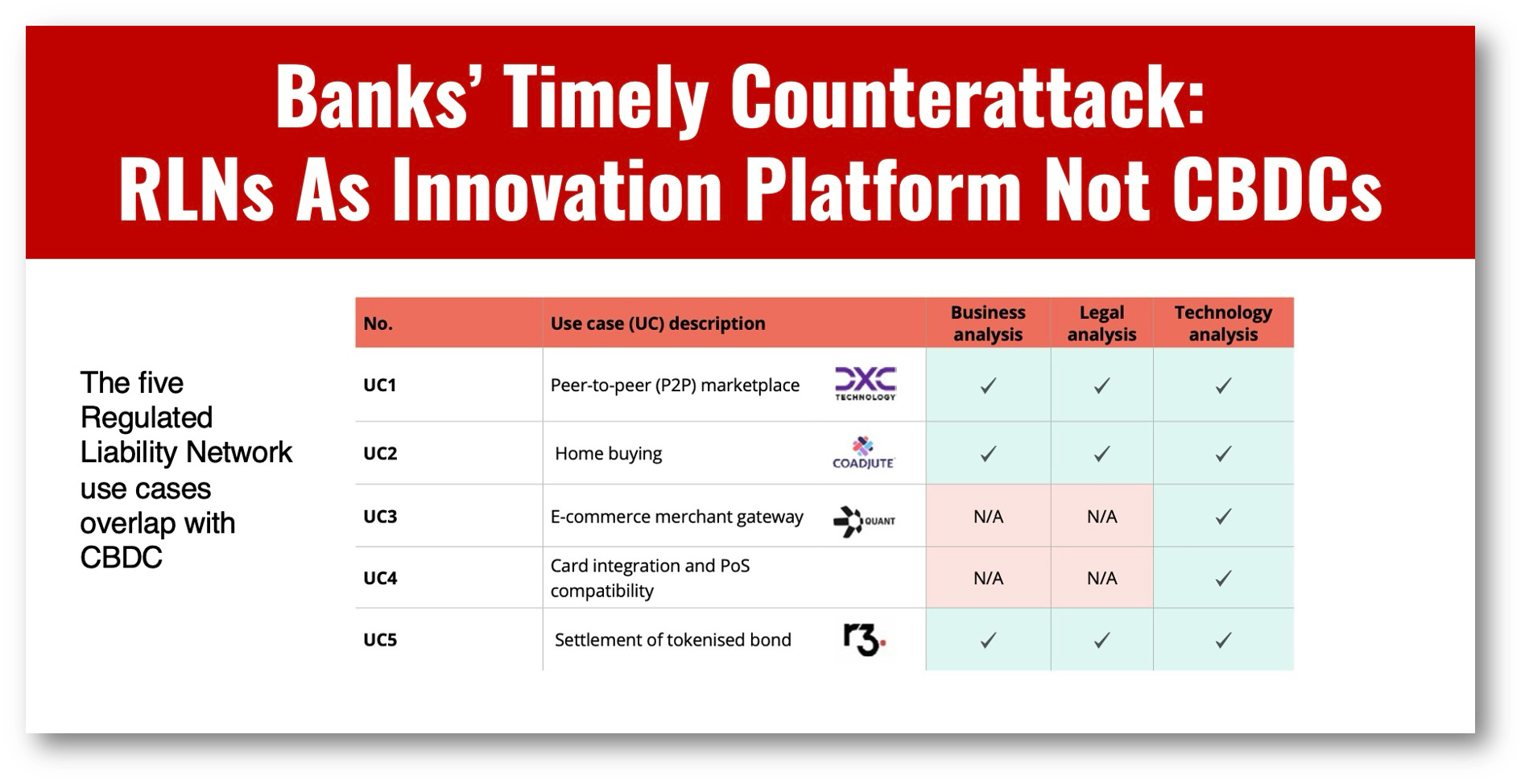

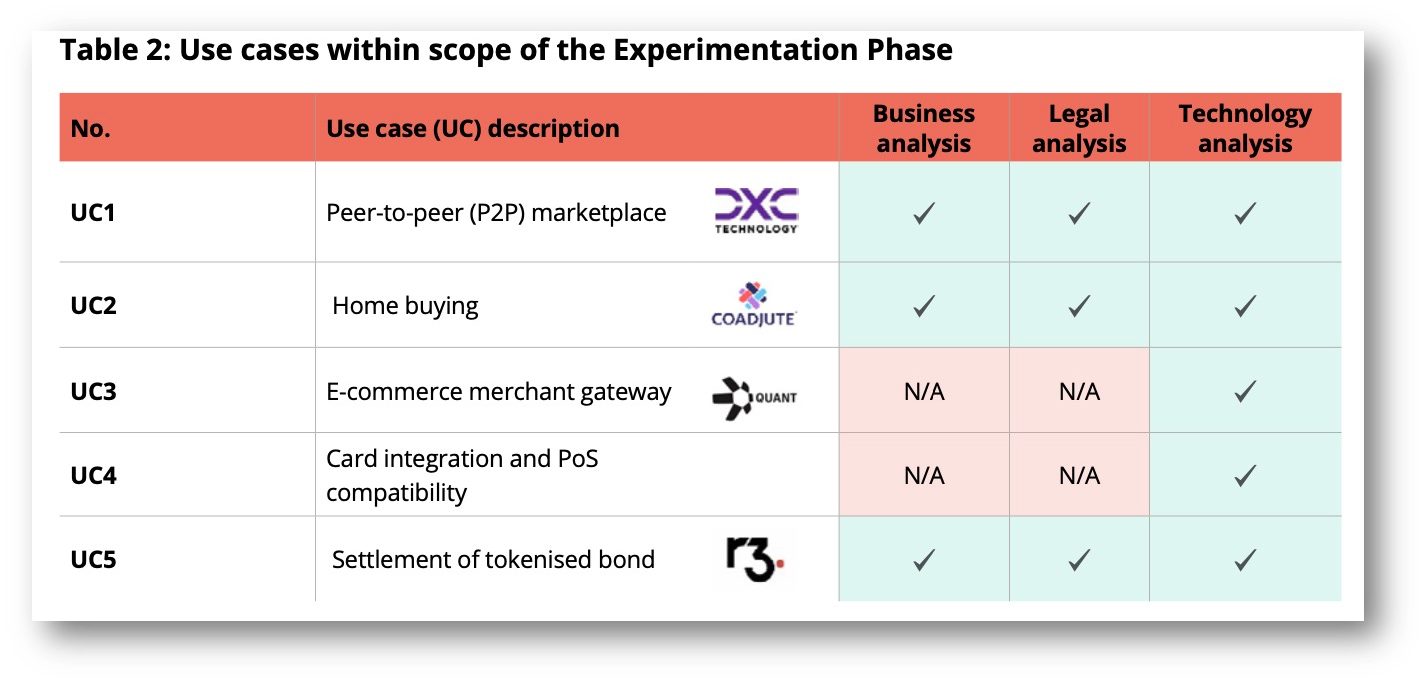

-The Experimentation Phase tested this platform across four different retail use cases and one wholesale use case to demonstrate how it can deliver 14 foundational capabilities, some of which are new (e.g. programmable payments) and cannot be easily delivered by current systems.

🔹 Benefits of the platform:

-New functionality not currently available in the UK market (such as programmable payments and locking/ unlocking of funds) could transform the customer journeys and business processes across a range of use cases.

-The Experimentation Phase identified over 40 potential business benefits that could apply to a range of stakeholders

-Innovators can connect to a platform for innovation via a single, common point of access. This provides a common interface to established institutions, FinTechs, payment and settlement systems and other innovators.

👊STRAIGHT TALK👊

Banks’ interest in RLN networks is fundamentally good, and it will likely lead to a unified platform on which they can tokenize assets to realize the 40 business benefits that they claim in the report.

I salute the 11 banks that took part in the trials and support their efforts.

That said, there is substantial overlap with CBDCs in the five use cases the RLN experiment focused on and this shouldn’t be seen as accidental.

CBDC can accomplish all five use cases, and it is hard to view aspects of this RLN experiment as banks attempt to ensure their centrality in payments in the future and, with it, their ability to maintain control over fees.

To the author’s credit they claim that the RLN “seeks to complement and function alongside other existing initiatives.” This is code for the Bank of England’s CBDC initiative.

One has to ask a fundamental question: Does a bank-controlled system better serve financial innovation, or should we look to new innovators who can bring fresh ideas to the marketplace?

CBDCs, are "Digital Public Infrastructure" and provide equal opportunities for innovation to the entire marketplace, not just those that banks deem worthy of their interest.

Despite my concerns, I want to be clear that I support RLNs and think that they deserve our support as one of many new technologies modernizing payments and settlement.

The key is that RLNs should be one of many initiatives!

You made it this far, so subscribe! Here are the six benefits waiting for you when you subscribe:

Save time: Get the expert insights on Central Bank Digital Currencies (CBDC), AI, Payments, and Financial Inclusion that you need to stay ahead of the curve, all delivered directly to your inbox weekly;

Know the future and profit: Get real payback from a unique point of view directly from Asia that focuses on how the region is “leapfrogging” the West and showing you the future;

Be prepared: CBDCs are no longer theoretical but coming soon, so keep up with the latest developments on the digital euro, yuan, sterling and dollar;

Manage your personal AI risk: Don’t be disrupted; be the disruptor. In-depth analysis of how our AI revolution impacts finance so that you can be in front of this great transformation, not behind it;

Stay objective, avoid hype: My writing doesn’t follow corporate diktats. It’s a message that doesn’t conform with mainstream media and is gritty, practical, hype-free, and, on occasion, controversial;

Stay safe: My writing is trusted by nearly 60,000 executives, innovators, investors, policymakers, journalists, academics, and open-minded crypto hodlers daily.

Readers like you make my work possible! Subscribing is free, but I am honored when readers opt for a paid subscription to recognize my high-quality writing and help keep it flowing. Thank you!

Sponsor Cashless and reach a targeted audience of over 50,000 fintech and CBDC aficionados who would love to know more about what you do!

Share