BIS: Stablecoins Do Not Support Trust in Money and Threaten Financial Integrity

Is the BIS anti-stablecoin, or does it know something the industry doesn't?

I post daily, but deliver to your inbox every Sunday. Browse past newsletters HERE. Book Rich. Bring the speed of Asia to your next event HERE

Read me first

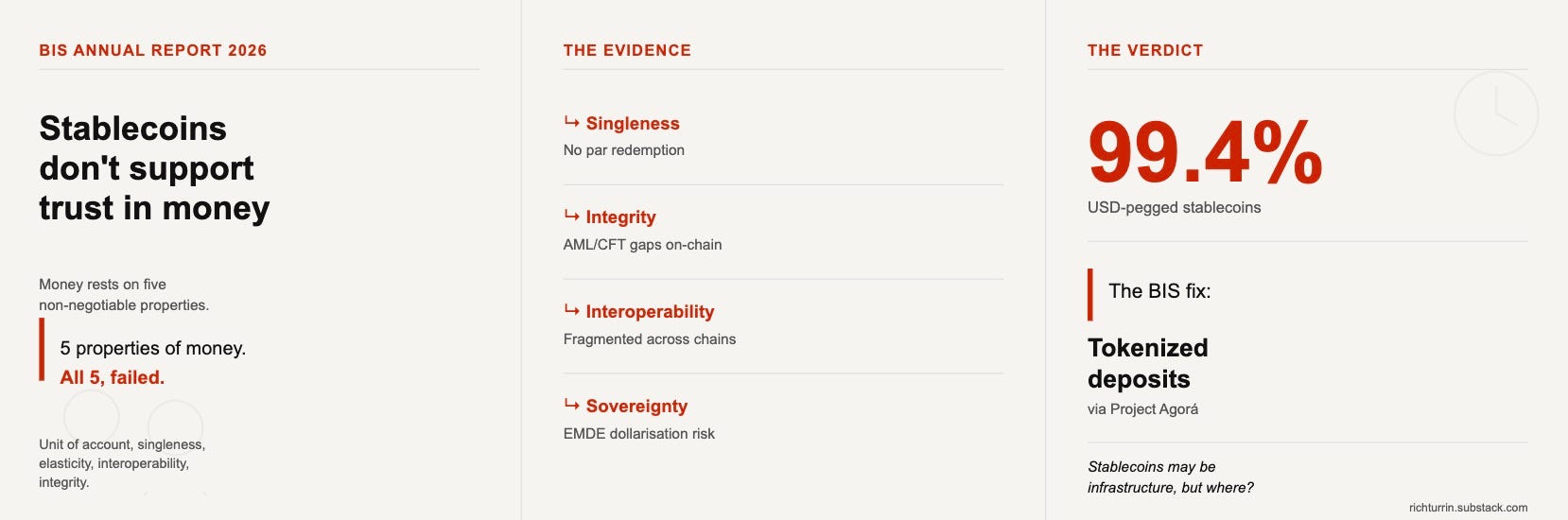

The BIS just declared that stablecoins do not support trust in money and use in illicit transactions threatens financial integrity. Its replacement isn’t a better stablecoin, it’s central bank money in the form of deposit tokens.

Spoiler alert: the BIS doesn’t believe that stablecoins can be fixed. Instead, it recommends central bank money through bank-issued tokenized deposits moving cross-border on the BIS’s own Agorá platform.

This will, of course, create a furor among stablecoin proponents who claim the BIS is biased and outdated.

Perhaps, but there’s a real possibility the BIS knows something about money that an industry treating the lack of par redemption as a feature, not a bug, hasn’t figured out yet.

Let’s build the BIS’s arguments against stablecoins from first principles. The BIS suggests money rests on five non-negotiable properties: a common unit of account, singleness, elasticity, interoperability, and integrity.

Strip out any one, and you don’t have money, but something that resembles it.

The BIS’s five main problems with stablecoins:

1. They don’t behave like money (violates singleness)

↳ The plumbing doesn’t connect. Stablecoin transfers never touch a central bank balance sheet, so par exchange isn’t guaranteed.

↳ The proof shows up in price. Secondary market values drift from par, and redemptions get gated, which the BIS says looks more like an ETF share than money.

2. Financial integrity is structural, not fixable with a patch (violates integrity)

↳ Stablecoins account for a significant share of illicit on-chain activity. Pseudonymity and unhosted wallets undermine KYC and AML/CFT compliance.

↳ Multifunction cryptoasset intermediaries borrow against stablecoin activity off-chain, creating deposit-like liabilities without the capital or supervision banks carry.

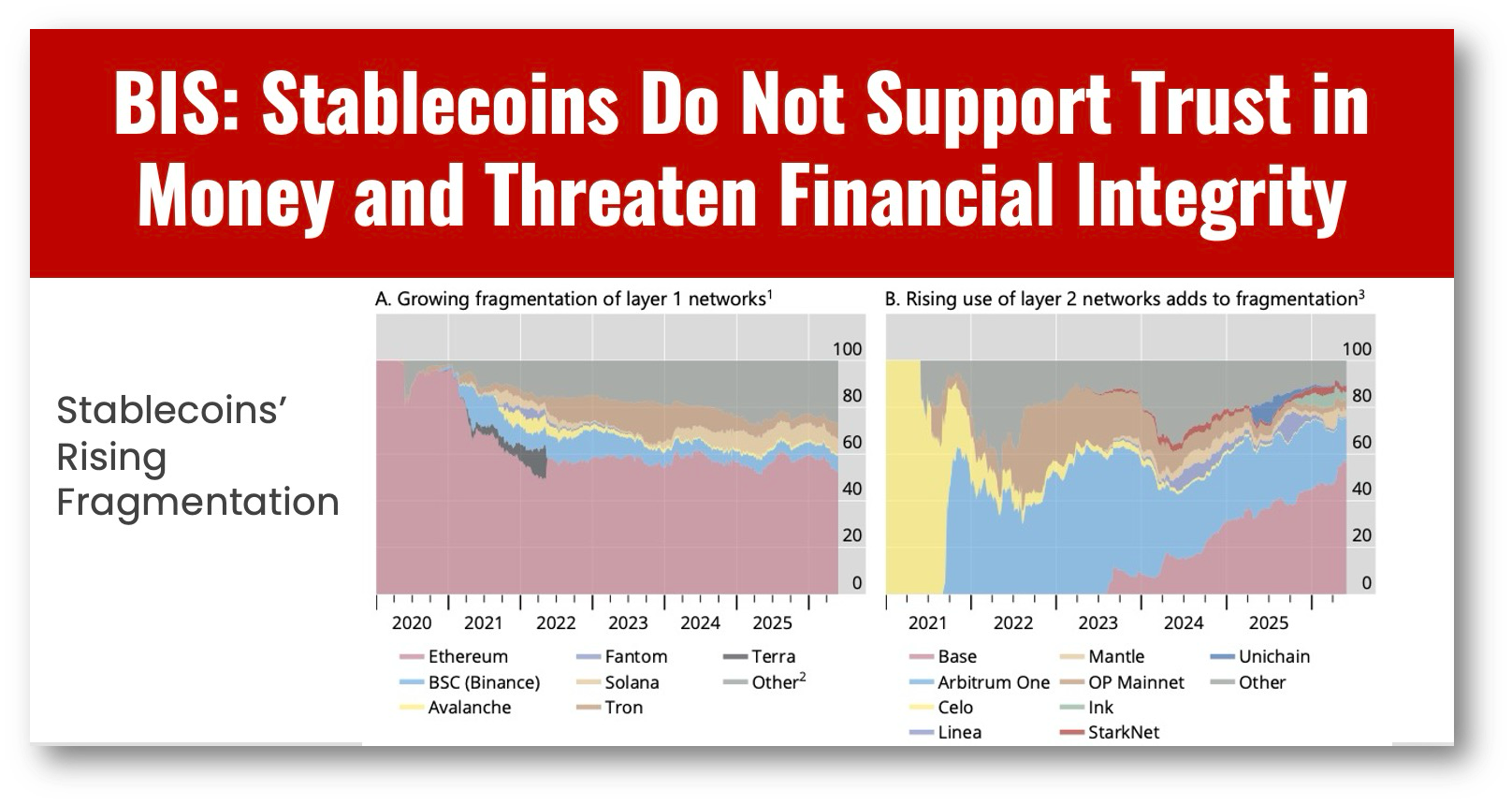

3. The rails are broken (violates interoperability)

↳ Public permissionless blockchains have been fragmenting, not consolidating, across both layer 1 and layer 2 networks since 2020.

↳ The same stablecoin issued on Ethereum and Solana is two separate, non-transferable tokens. Moving value between them risks permanent loss.

4. Macro-financial spillover risk (violates elasticity)

↳ Every reserve scenario the BIS models, bank deposits, treasury bills, or central bank reserves, weakens the banking sector’s funding position and could tighten credit.

↳ Sizeable redemptions could hit money markets and funding conditions directly.

5. Stablecoin dollarisation in EMDEs (problem of monetary sovereignty)

↳ Foreign stablecoins could reshape capital flows, exchange rate dynamics, and challenge monetary sovereignty in emerging markets.

↳ They’re a ready substitute for domestic currency even where foreign currency deposits are restricted, since digital bearer-like tokens are hard to wall off.

But before readers think I’m a shill for the BIS, let’s look at this report’s biggest blind spot.

The BIS built a strong case against where stablecoins stand today. It didn’t fully account for how fast that ground can shift.

The report cites ongoing regulatory measures, the GENIUS Act, Hong Kong and Singapore frameworks, and acknowledges that issuers are already freezing addresses and using blockchain analytics to fight illicit activity.

What it doesn’t fully engage with is the pace of private-sector fixes like improved bridge security or Ubyx stablecoin clearing that are chipping away at its own fragmentation critique in real time.

Still, the questions that the BIS raises are real, and their use as a primary cash transfer system between financial institutions seems remote, despite claims by proponents that they are “infrastructure.”

Stablecoins may be infrastructure, but it remains to be seen where.

👉Foundational properties of money

Common unit of account

The unit of account is the numeraire in which value is denominated. What’s key is the collective agreement to use the same unit for economic calculation, the language of value that places disparate transactions on a common footing.

Singleness

Singleness means claims denominated in that unit redeem at par with central bank money, with finality. One dollar, euro, yuan or peso is worth the same as any other in settlement, including under stress. Even a tiny deviation from par may pass in fair weather, but it disintegrates the moment stress hits. Together with the unit of account, this is what makes money information-insensitive, an asset that passes hand to hand with no questions asked.

Elasticity

Liquidity has to expand and contract with system-level need. Tax dates, quarter-ends or shifts in risk appetite generate abrupt swings in demand for settlement balances, and a rigid supply turns a soluble liquidity shock into a solvency crisis. Central banks prevent that by supplying intraday credit and standing ready with backstops, and commercial banks replicate the same elasticity one layer down.

Interoperability

Interoperability lets network effects compound instead of splinter. When platforms interoperate under common standards, each new user expands who can be paid at par without delay, lowering costs and deepening trust. Fragmented systems do the opposite, trapping liquidity and eroding the perception of singleness. It’s money’s connective tissue, carrying the unit of account across rails, domestically and across borders.

Integrity

Integrity means preventing illicit activity in the monetary system, money laundering and terrorism financing chief among them. When compliance and consumer safeguards are embedded at the user interface, payments flow at par with no questions asked. Without it, lapses propagate as fast as payments do, eroding trust and ultimately fragmenting the networks built on it.

HAND CURATED FOR YOU

🚀 Asia moves fast. So does this newsletter. I curate only the best fintech, CBDC, and AI insights from 50+ sources weekly so you stay ahead of what’s coming West. Subscribe and never fall behind.

If you know someone who would like this newsletter, please share it with them and help grow our Asia, CBDC, and AI aficionados community!