Bottom Line: Forget Banks—Crypto & Asset Managers Rule Tokenization

Banks have too much to lose to drive the tokenization revolution.

This is my daily post. I write daily, but send my newsletter to your email only on Sundays. Go HERE to see my past newsletters.

HAND-CURATED FOR YOU

Tokenization is coming, but not from the direction you think. Asset Managers and crypto exchanges are diving in, leaving banks once again on the sidelines as crypto exchange Kraken begins offering 24/7 trading of tokenized US equities.

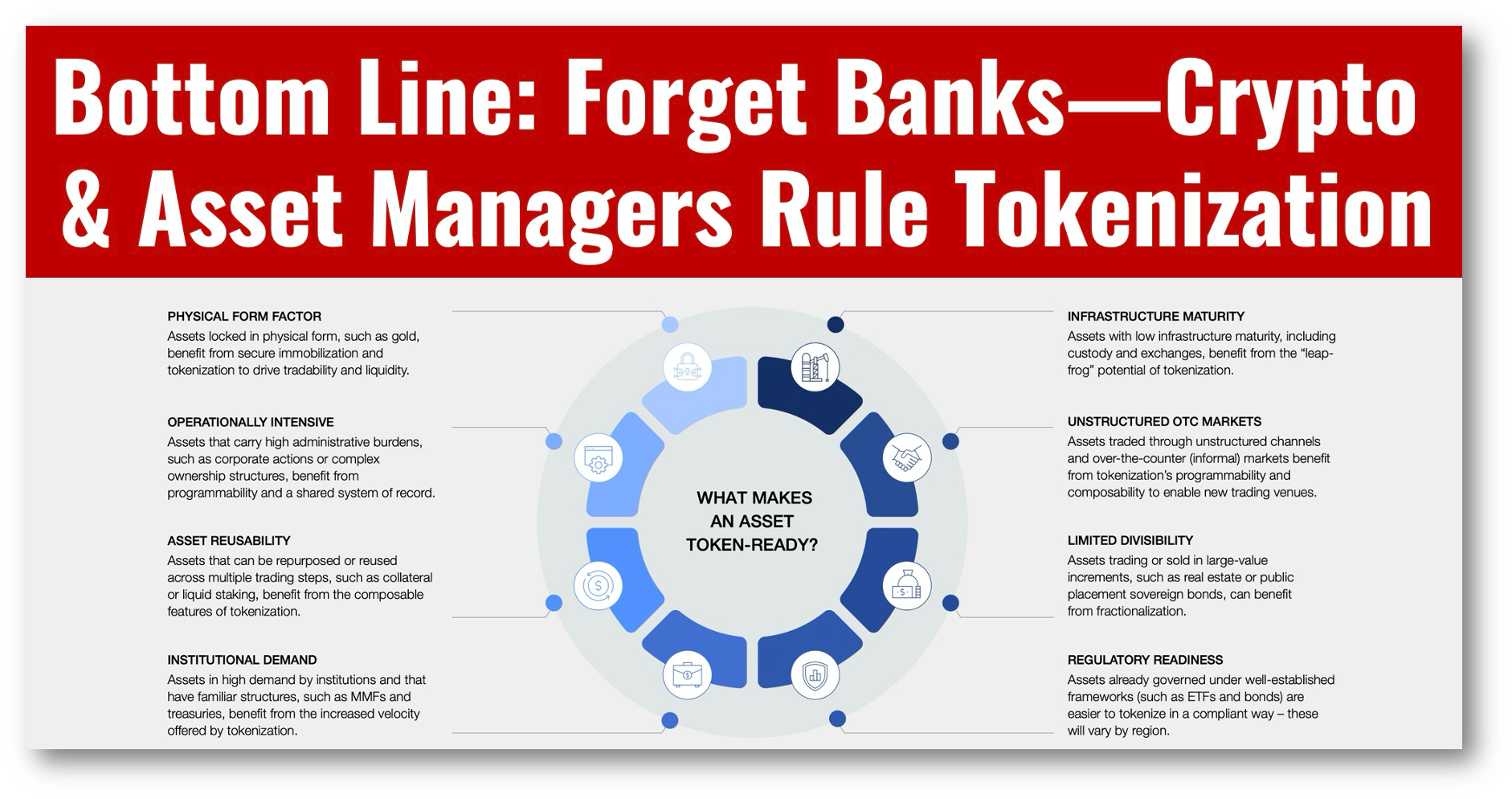

The WEF presents a refreshingly hype-free report on tokenization, which goes into fabulous detail and is worth your time, but it doesn’t capture the battle on the street.

We’re all waiting for tokenization, and it’s happening all around us, but we’re looking in the wrong places. The battle is already over, and banks lost.

Banks and traditional exchanges won’t be driving tokenization, as they have too much invested in legacy systems and receive far too much in fees and commissions to jeopardize them.

In contrast, crypto and asset managers have the most to gain from tokenization, and you can look to both to drive the process, as they are already doing so.

Let’s look at two examples.

First Crypto exchange Kraken announced last week that it is launching tokens of U.S. equities, which will trade around the clock, giving non-U.S. investors exposure to high-profile U.S. stocks. Backed by xStocks, the trading will be backed 1:1 by real shares and settle instantly using the Solana blockchain.

This kind of bold leap may not surprise readers, who may expect crypto to always be one step ahead and one step away from being illegal. In this case, however, Kraken is simply brilliant in launching xStocks.

This brings us to our second example, BlackRock, the world’s largest asset manager with a gravitas few can ignore.

Larry Fink, the CEO of BlackRock, wrote last week in a letter to investors that: “turning financial assets, including stocks, bonds, and real estate into digital tokens that trade online -- will be a key to driving the democratization of private market assets.”

Fink wants more clients, and tokenization will bring them, so BlackRock runs BUIDL, a tokenized money market fund for institutional investors with a market cap of $3 billion.

Proof enough?

Tokenization is coming, but don’t expect it to arrive with a big bang from an exchange or bank. Instead, watch crypto and asset managers who will adopt it organically to give clients what they want and deserve.

👉Barriers to tokenization adoption

🔹 Traditional financial infrastructure

A challenge faced by financial services institutions is reconciling the books and records of tokenized systems with their internal books, which can result in possible discrepancies or disputes regarding the official claim of the asset. Addressing challenges such as these requires a staged approach to secure transactions between traditional and tokenized systems.

🔹 Global standards

Global tokenization adoption requires robust, harmonized standards. Five critical areas that would need to align for widespread usage are roles and responsibilities, token standards, cashless and settlement, cross-chain interoperability, and reference data. ERC-20 tokens remain dominant but lack compliance features, leading to the rise of ERC-1400 and ERC-3643 (T-REX).

🔹 Cross-chain interoperability

Financial services entities had adopted at least 72 distributed or programmable ledgers as of May 2025 and driven 10 market forces that are accelerating the deployment of individual networks. These networks are not all inherently interoperable and the importance of cross-chain interoperability is underscored to realize inter-network activity.

🔹 Secondary markets

Secondary markets are critical to liquidity, yet tokenized assets struggle to establish market depth. Many tokenized assets could not yet attract sufficient secondary trading volume, leading to illiquidity and difficulty in accurate pricing.

🔹 Privacy and compliance

Fragmented identity verification limits the growth of tokenized financial products. Standardized KYC is estimated to improve onboarding efficiency by up to 90% in fund management. On-chain identities offer potential but raise privacy concerns. On-chain identity enforcement often follows allow—or deny-list models. Allow lists enhance security but limit inclusivity, while deny lists are more open but require constant monitoring to mitigate risks from malicious actors.

If you know someone who would like this newsletter, please share it with them and help grow our Asia, CBDC, and AI aficionados community!