Britcoin explained: the Digital Pound is a design masterpiece!

Understand how the digital pound protects privacy and delivers payment innovation!

“Britcoin,” the not so official moniker for the “digital pound” central bank digital currency (CBDC), is coming! While the Bank of England (BoE) and UK Treasury haven’t committed to launching Britcoin, they actually do have a timetable! Should the government decide it wants Britcoin it will be ready to go by the end of the decade or earlier.

This is not a dress rehearsal. The BoE and Treasury know that the world is changing and that digital currency will be a necessity for the innovations it will bring! So my advice is to look for a digital pound by 2028! Prediction made!

Download my marked-up versions of the digital pound publications on these links. Consultation Paper: here Tech working paper: here

The digital pound documentation is absolutely the best CBDC paper that I have read to date! I give the BoE teams a lot of credit for going the extra mile in explaining CBDC and how they are going to build it.

The BOE’s documentation is in two parts, the first is a “Consultation Paper” that outlines the BoE’s rationale for Britcoin and its thinking on CBDC. The second “Technology Working Paper” explains some of the basic design requirements and some fascinating specifications.

My coverage of Britcoin will be divided into two parts to match the two publications. My goal is to pull out the key parts to help the reader get a better idea of what the UK’s CBDC will look like.

SPOILER ALERT:

If you understand what the digital pound looks like, you’ll also have an excellent background for understanding the digital euro and the digital RMB. The reality is that all of these CBDCs share more architecture in common than you would think! That’s not supposed to scare you, but shows how CBDCs share a common design language centered around the belief that you should keep your relationship with your bank. Central banks will not have your “account” or be your banker. Still, “the devil is in the details,” and these three CBDCs make many different design choices!

My prediction is that we will have a digital pound by 2028!

Part 1: Why create the digital pound and its design philosophy

We’re going to have the Britcoin CBDC by 2028, and to counterbalance going “cashless” the UK is going to enshrine the right of access to CASH for all in the UK!

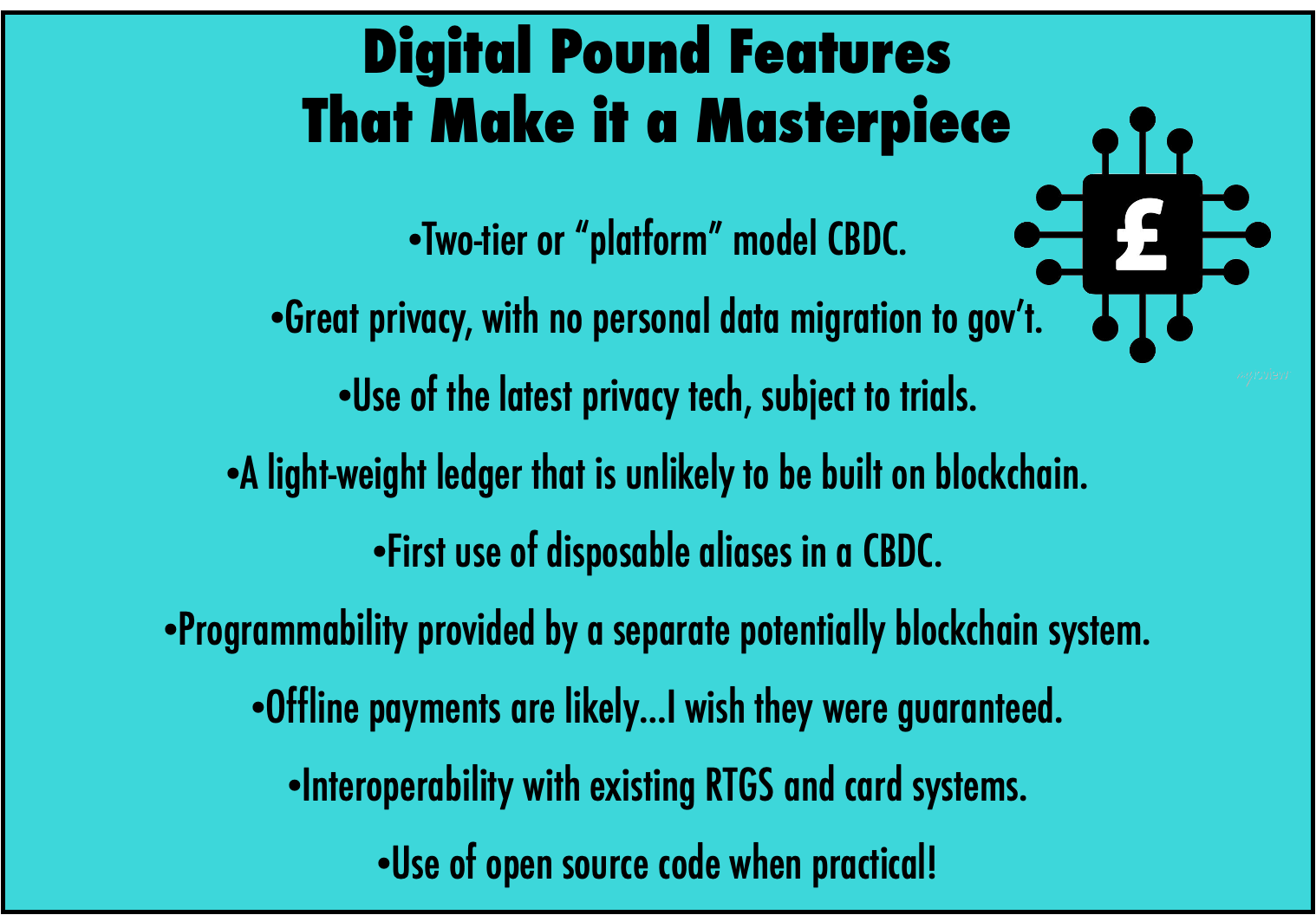

Key features of the digital pound from the BoE, Treasury report.

The Bank of England (BoE) and Treasury are hard at work on “Britcoin,” while a new law that guarantees the right of access to Cash is going through Parliament!

The law will “defang” conspiracy theorists who claim CBDC is a plot by “Davos man” to eliminate cash and, while unrelated, compliments the CBDC project! Let’s just say that the BoE and Treasury got lucky!

The Financial Services and Markets Bill will ensure that cash access is maintained throughout the UK. A response to closing bank branches and increased use of digital payments. If passed, which appears likely, it will mollify those who are afraid that CBDCs are a government plot to eliminate cash. Link to article: here

Key points in the consultation paper:

1️⃣ The BoE’s CBDC rationale mirrors the ECB’s for the digital euro:

To sustain access to UK central bank money – ensuring its role as an anchor for confidence and safety in our monetary system;

To promote innovation, choice, and efficiency in domestic payments as our lifestyles and economy become ever more digital.

2️⃣ No love of crypto:

“Uniformity and safety could be threatened by a combination of lower cash use and the emergence of some new forms of private digital money.”

Private digital money has two primary problems:

1. Walled gardens and closed loop systems are closed payment systems controlled by the system operator.

2. Convertibility may be costly, complex, slow, or impossible between different forms of digital money.

3️⃣ The BOE guardedly accepts stablecoins, unlike the ECB:

“Even if there were a systemic stablecoin that is backed by liabilities of the central bank and looks economically similar to the digital pound, a significant case for the digital pound would remain.”

Britcoin promotes universal access to central bank money and innovation.

BoE shockingly admits: “Britcoin need not be the dominant form of money!”

4️⃣ PRIVACY:

The BoE, as the operator of the payment system, would not have access to personal data.

The private sector would interact directly with end users and would hold the customer’s information as banks do now.

Only anonymized personal data would be shared with the BoE.

Small cash payments are anonymous, but larger value transactions require more data collection to mitigate financial crime. This is identical to the “tiered KYC” requirements of both the digital euro and digital RMB.

The digital pound would have at least the same level of privacy as a bank.

Enhanced privacy could allow users to benefit from sharing personal data.

5️⃣ Other critical features:

Non-interest bearing.

OFFLINE capabilities!

Limits on holdings of Britcoin between £10-£20,000.

The inclusion of financially excluded groups is a priority.

Takeaways:

BRITCOIN IS GREAT! Congrats to the BoE and Treasury for not just having the vision to prepare the UK for the future but doing it in a public fashion!

Privacy with the digital pound will be better than what you have today with your banks!

Proclamations of a “dystopian” future because of CBDCs are simply not true, and if you watch closely are from people selling either crypto, gold, or survival bunkers!

The new Financial Services and Markets Bill will mandate maintaining cash access and will defang conspiracy theorists!

BoE's guarded acceptance of stablecoins is actually a first and stands in contrast to the European Central Bank’s less favorable opinion!

The US Federal Reserve still suffers from a “crisis of vision” on CBDC. The European Central Bank and Bank of England put the US efforts and research to shame! Harsh, but sadly true!

Part 2: Technical Foundations for the Digital Pound

(Have no fear not too technical)

There is an old saying in the marketing business that to sell a steak, “you need to sell the sizzle not the steak.” Where the sizzle is the mouth-watering sound of the steak hitting the hot grill, which makes people want to buy. The two papers from the BoE are similar and the Technical Foundations paper lays out far more “meat” or detail about the digital pound than the first, which sold the sizzle!

My coverage of this section will be intentionally incomplete. This is a very long document, and the best I can do is to bring some of the more exciting features to light.

1️⃣ The Two-Tier CBDC is now called a “Platform”

The central bank “core ledger” run by the BoE is separated from users by putting banks and other financial entities in between. This means you, the user, do not have an account or direct relationship with the central bank.

Whether called “platform,” “two-tier,” or “intermediated,” the intent is the same, allow banks or new “Payment Interface Providers” (PIPs) to service CBDC users.

The two-tier or platform design also allows for greater privacy as the central bank can be kept away from personal user data, so it cannot connect users with payments.

A rose is a rose by any name.

Platform is another way of saying “two-tier” CBDC.

2️⃣ Design Considerations

The BoE recognizes a total of six primary design decisions. I will leave the following four decisions for the reader to explore in the document: Security, Resilience, Extensibility, and Energy Usage. These are all critical components but pale before the two that I will cover:

Here’s to Privacy:

The BoE makes it clear that neither it nor the government will have access to users’ personal data. The exception is for law enforcement, who can access the data as prescribed by law. This is precisely what we have now with your bank.

The BoE says that the CBDC would not be anonymous due to the need to prevent financial crime. This is a contradiction of their position in the first paper that promoted “tiered” levels of anonymity with small payments remaining anonymous. This needs clarification.

The exploration of “privacy enhancing technologies” (PETs) like zero-knowledge proofs or encrypted data processing is laudable! The BoE is showing it’s going for high-tech privacy. I commend them. That said, all PETs increase system complexity or impact other system parameters.

Performance and Blockchain is unlikely:

In a surprise move, the BoE claims that the UK only needs 30,000 transactions per second (TPS) as the performance level! Wow, that’s low!

The design specifications will be for 100,000 TPS

For scale, look at these comparisons. Alipay at its peak, processes 520k TPS, while Visa and MasterCard networks are in the 50-70k TPS range. The PBoC design spec for the e-CNY was for 300k TPS.

What is interesting is that with 100k TPS as a target, modern DLT solutions might just work! BUT…..

Likely No Blockchain or DLT:

-Permissionless blockchain: “presents privacy and scalability challenges that might limit its ability to meet requirements for a CBDC.“

-DLT: “it would still be challenging to achieve very fast transaction processing given that the central bank [would need to operate a notary node which] would likely be a bottleneck on that network, as well as a single point of failure.”

3️⃣ The Basic Britcoin Model…..looks like the digital yuan:

While I don’t want to strike fear in readers’ hearts, the basic model looks a lot like the PBoCs for the digital yuan! The biggest similarity is the prominent separation of servers into three separate units covering programmability, Alias (personal identifiers), and Analytics. (see tan, green, and pink boxes below) That the PBoC and BoE envisioned the server separation similarly is not a surprise but a necessity of privacy designs that shield your personal payment data from the state. While it may surprise some readers, China’s e-CNY is privacy protective!

Understanding the pieces:

Core ledger: This is the “engine room” whatever system the BoE chooses, blockchain or database, the encryption and decryption of payment data will happen here. The BoE will provide the “minimum necessary" functionality.

Analytics: Interestingly, this is not for gov’t AML or fraud investigations but for system status and performance data. The BoE apparently will leave AML to banks. This is unlike the ECB and PBoC, which use analytics servers to look for fraud.

Alias Service: This ensures that users remain “pseudonymous” by separating out personal identifiers from data passed to central bank systems. These identifiers include not just your name but your digital wallet identifier. The BoE is experimenting with “disposable aliases” that can be used short term. This is a first in CBDC design!

API Layer: The API is a data gateway that allows banks (PIPs) to build wallets and service their users. All data traffic with the BoE systems travels through the APIs. What makes APIs interesting in the context of Britcoin is that with programmability, the API need to both push and pull payment instructions.

Devices and payments: The target devices are: Smart devices, smart cards, e-commerce websites, and PoS devices. Frankly, there’s nothing new here that Alipay hasn’t already perfected. The ability to use smart cards offline is likely the most significant technical challenge.

-Device verification for connected devices would be through an online PIN where the PIN is encrypted and verified online. For offline devices, a “consumer device customer verification method (CDCVM) is necessary. This is a biometric or pin used to authenticate the user.

Interoperability: The ability to connect with the UK’s existing payment systems is considered critical. The UK already has the “Faster Payments System," which is a real-time gross settlement (RTGS.)

Programmability: The BoE will not pursue “bank-initiated” programmable functions. This means the BoE will not have the ability to program its CBDC, but banks (PIPs) certainly can. The BoE is making it clear that programmability is a necessary function for future innovations, but the government will NOT program your money.

-The BoE makes a key design decision by stating that programmability will not be built into the core ledger but exist separately. Ethereum and Avalanche blockchains are being considered! That is slightly different from PBoC design specs that build programmability into the actual token.

-From a privacy and control perspective, the BoE’s hands-off approach to programmability is superior, but the PBoC gains in being able to program aid payments or disaster relief, a stated CBDC goal.

Offline Payments: Here, the BoE is clear that it wants offline payments, but it is concerned over their security and their complexity. BoE is rightly concerned about “double spend,” but If the PBoC can handle it, I have faith that the BoE can find a solution as well!

-PBoCs solution for small offline transactions is to use device verification as security and check for double-spending transactions after they have been processed.

So here are the features that I think set apart the digital pound that will make it a “design masterpiece.” My only misgiving is I wish the BoE would commit to the offline payments feature! If China can do it so can the BoE!

Takeaways:

Technically the BoE’s CBDC is a masterpiece.

The BoE is going for high-tech solutions at virtually every design juncture.

The BoE’s documentation makes an excellent read for anyone who wants to understand CBDCs.

Privacy is being pursued using the most advanced tech available. We do not know what tech will be adopted, but even the lowest-tech options are excellent at preserving privacy.

REMEMBER: The BoE will not have your personal data, which remains with your bank!

Keeping programmability in Britcoin but denying the government ability to use this function is a good compromise. Anti-CBDC zealots, however, may not be appeased.

Remember that the ECB recently declared that there would be no programmability in the digital euro!

That the BoE is guarded about using blockchain (DLT) is telling, but I wouldn’t rule anything out yet!

See how deep the “cashless” rabbit hole goes!

Subscribed

My work is entirely supported by reader gratitude, so if you enjoyed this newsletter, please do both of us a favor and subscribe or share it with someone. You can also follow me on Twitter, or Linkedin for more. If you want to learn more about Innovation Labs or China’s CBDC, check out my website richturrin.com which is full of videos, interviews, and articles. The best way to make sure you see the stuff I publish is to subscribe to the mailing list here on Substack, which will get you an email notification for everything I post.

Everyone, including platforms that disagree with me, has my permission to republish, use or translate any part of this work or anything else I’ve written (except my books) with credit given to me and this site (richturrin.substack.com) free of charge. For more info on who I am, what I do, and where I’m going, check out richturrin.com

Rich Turrin is the international best-selling author of "Cashless - China's Digital Currency Revolution" and "Innovation Lab Excellence." He is number 4 on Onalytica's prestigious Top 50 Fintech Influencer list and an award-winning executive previously heading fintech teams at IBM following a twenty-year career in investment banking. Living in Shanghai for the last decade, Rich experienced China going cashless first-hand. Rich is an independent consultant whose views on China's astounding fintech developments are widely sought by international media and private clients.

Please check out my books on Amazon:

Cashless: HERE

Innovation Lab Excellence: HERE