CBDCs in the news: APAC leading, Cross-border transfers coming soon, decrease US financial exclusion by 93%

AI Bill of Rights or Wrongs?

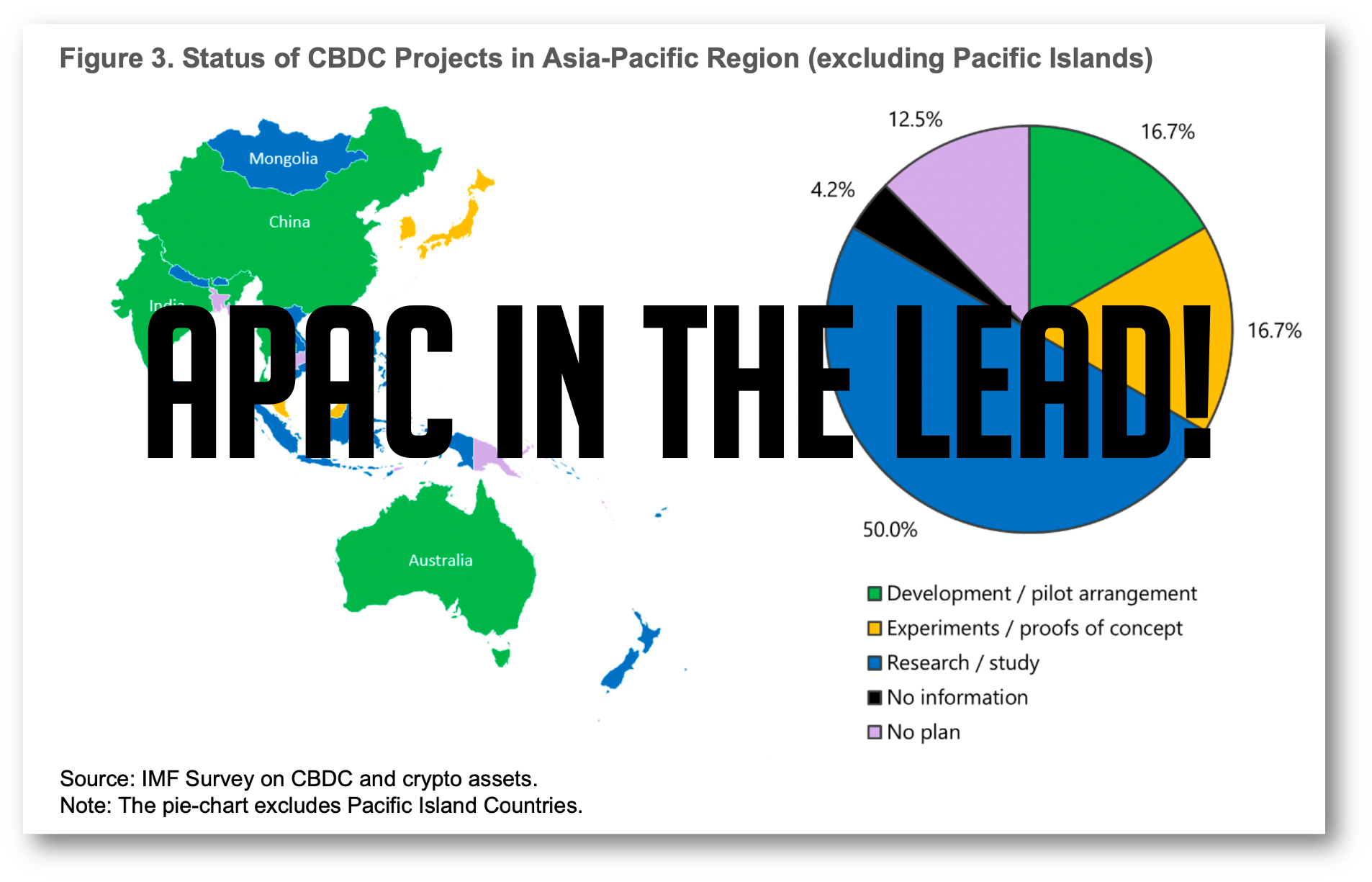

1. IMF Says APAC leading on CBDCs

2. Cross-border CBDC transfers

3. US AI Bill of Rights or Wrongs?

4. US CBDC decreases exclusion by 93%

1. IMF Says APAC leading on CBDCs

The IMF confirms that Asia is at the forefront of CBDC and digital innovation!

Download “IMF: Toward Central Bank Digital Currencies in Asia and the Pacific”: Here

Please don’t blame me if I take great joy in this article. For at least the last two years I have been claiming that all eyes should be on Asia's CBDC development.

The good news is that the IMF just concluded I was right! True, there have been other surveys that claimed this, however, none with the gravitas of the IMF.

In early 2022, the IMF conducted a survey in the Asia-Pacific region, covering 36 Asian economies. This is the widest survey of APAC with 20 more jurisdictions than surveyed by the BIS.

Here are there findings:

➣Fact I. The Asia-Pacific region is at the forefront of CBDC exploration

A full 83% of the 36 nations surveyed are either researching, experimenting or developing CBDCs!

➣Fact Il. Interest in CBC development has clearly been on the rise in Asia-Pacific.

China, Singapore, and Hong Kong SAR have been the frontrunners even in a global context, thanks to their technological advantage and relatively mature private sector digital payment platforms. This was followed by a number of Asian economies flocking to the CBDC arena during 2018–22, as the global initiatives on digital currencies accelerated.

➣Fact Ill. Central banks in Asia are interested both in wholesale and retail CBDCs.

The motivation for developing wholesale CBDCs focuses on enhancing payment system efficiency and security, particularly for cross-border transactions, while reducing transaction costs. The report sites projects Dunbar and mCBDC in Singapore and Hong Kong.

➣Fact VI. The key drivers for countries' interest in CBCs differ by income group.

High-income countries are generally more interested in the ability of CBDCs to enhance the efficiency and safety of the payment system as well as to satisfy the growing demand for digital cash. For middle-income countries promoting financial inclusion and financial stability are important drivers.

➣Fact VIl. While there is a significant interest in CBCs, very few countries are likely to issue CBDCs in the near to medium term.

Only two countries in the region—India and China—are very likely to issue retail CBDC in the near term. 💥37% of the world’s population! 💥 So CBDC are coming to APAC but not overnight!

➣Fact X. The landscape of CBDCs in the Asia-Pacific region is intertwined with crypto assets.

Like it or not CBDCs owe a debt to crypto! In 2021, Asian emerging markets accounted for 16 percent of total crypto asset transfers in the world. Lower-income countries have crypto transactions amounting to greater than 20% of GDP!

Takeaways:

CBDCs are coming to APAC and are a natural consequence of both digital innovation and high crypto adoption

Wealthy countries want payment efficiency while the poor want financial inclusion.

China's CBDC program kicked this off!

Adoption will be faster than the IMF predicts!

2. Cross-border wCBDC transfers in two parts: Privacy and SWIFT

Download Part 1: “Privacy in Cross-border Digital Currency: Here

Download Part 2: “Connecting digital Islands”: Here

The SWIFT document contains 3 parts: 1) SWIFTS’s CBDC document, 2) An extract from the BIS explaining the 3 mCBDC models, 3) SWIFT’s Tokenized Assets document.

Part 1: Privacy

Trans-Atlantic cross-border wholesale CBDC transfers are coming, and privacy will be built-in from the start, but it won’t be easy.

Atlantic Council explains wholesale cross-border CBDC transfer privacy in the clearest and most understandable way yet.

I will warn you this document is technical, but it shows in detail how messy cross-border CBDC transfers will be and why they will not happen overnight!

Next, in part 2, we’ll look at x-border transfers with SWIFT’s innovative new entry! A much lighter read!

Let’s start from the basics. The total cross-border flow is estimated to reach $156 trillion in 2022 and more than $250 trillion by 2027. The system we currently use is based on correspondent banking which is slow and expensive.

CBDCs are seen as the solution to this problem. Even the anti-CBDC zealots begrudgingly acknowledge their utility in wholesale transactions.

CBDC privacy is different for each

The problem is how to put systems together that ensure privacy when CBDCs carry different data depending on domicile and whether they are account-based, or token-based. Even harder are the different legal requirements of what data can be transferred.

For example, the EU’s GDPR laws enshrine privacy and data transfer standards as rights for all residents, while the US privacy laws differ by state and industry sector.

This is a solvable problem but one that needs much thought and careful integration of differing systems. This is why it is hard to ignore SWIFT. They are already working within each of these jurisdictions and have a clear lead.

Spoiler alert for Part 2!

Given the complexity of CBDCs from a technical and legal point of view can you see where SWIFT might still add value?

So what do we need to do to build a cross-border CBDC system:

🔹Central banks must agree on messaging formats, data frameworks, and AML/CFT requirements. This is very doable for the US and EU but watch as China and the West disagree!

🔹The privacy-transparency trade-off, which gives users adequate protection from excessive data transfer and enforcement the ability to tackle illicit flows, also needs standardization. The goal will likely be to mirror the data transfers we have today, but what happens if a CBDC contains more data? Can it be encoded, removed, or hidden? What if it has less?

🔹 One CBDC design choice comes into focus. Token-based CBDCs using the UTXO model are slightly more compatible with privacy mechanisms than account-based models (but not always). Tokens are harder to trace back to an account. This technical specification, however, is unlikely to be standardized!

Part 1, Takeaways:

I know that this was a challenging read and that it may not be for everyone.

If we want the miracle of cheap and immediate cross-border transfer that CBDCs promise we have to work through the details which are very thorny.

If you sense that there’s much work to do, and that this is far more complicated than a Bitcoin transfer, I’ve done my job!

Part 2: SWIFT

SWIFT’s “ground-breaking” cross-border CBDC transfer system will keep it in the game for years

SWIFT recognizes that CBDCs represent both an existential threat and a tremendous opportunity and is innovating to ensure its continued dominance in cross-border transfers.

“But CBDCs were supposed to get us off SWIFT.”

Many reading this will be saying, “CBDCs were supposed to get us off SWIFT.” That is true, many CBDCs can and will transfer without using SWIFT’s systems, and not just those of China and Russia.

SWIFT by virtue of its dominant position, however, will have a big role to play in CBDC transfers and isn’t going away. Their innovation teams are working overtime to adapt to CBDCs and with this project, we see that they’ve “cracked the code.” What will be disruptive for SWIFT is that it will not be “the only game in town” anymore. Their monopoly is over and it can never be undone.

🔹What SWIFT built:

• A BIS Model 2 “interlinking” mCBDC system. (Above or BIS on pg 19 of PDF) Interlinking means that each CBDC is connected to another via an interface. Each CBDC has to be connected, not to a single network (Model 3), but with each and every other CBDC.

The number of interfaces increases geometrically with each CBDC added which is why the BIS has issues with this type of system (pg21 blue). The system is complex, while CBDCs promised simplicity.

🔹 How does it work?

• SWIFT is building off the strength of its ISO 20022 payment systems already installed by clients. It uses existing systems to interact with CBDC "connector gateway." The gateway is "a single entry and exit point for cross-border payments to and from the CBDC network." A form of CBDC bridge.

The connectors are custom-built, and SWIFT does not provide details. This is “the secret sauce” and how SWIFT will connect account-based CBDCs to tokenized is a mystery but is technically achievable.

🔹 Is it any good?

• Yes it is! I prefer the BIS’s single platform design (Model 3 above) but SWIFT’s built-in infrastructure gives it a huge advantage! Banks will likely require minimal changes in their systems and that is HUGE. Bank back offices are breathtakingly complex.

🔹 The elephant in the room:

• SWIFT’s new system will support sanctions. In about 2 years all of the BRICS nations will have CBDCs and clearly, some will not want to use SWIFT. Those that do will combine it with other transfer systems like Hong Kong's mCBDC. Nations can use more than one system in theory. In practice, will using one mean ejection from the other?

Takeaways:

SWIFT delivered a “breakthrough” mCBDC system, I credit their innovation team! See also their solution for tokenized assets!

The system's weak points are that we don’t know how SWIFT will build connector gateways to connect CBDCs and that they need to build a lot of them!

Currency bifurcation is real, some nations will choose neutral non-sanction systems.

“If you build it they will come.” Yes they will, but SWIFT isn’t the only game in town anymore.

3. US AI Bill of Rights or Wrongs?

The White House’s AI Bill of Rights is a step in the right direction but what’s not in the bill is more important than what is!

Download: here

First, let me say that I am delighted that the US is finally doing something even if it’s just a “white paper!” That the US is FINALLY looking to set policy on AI, and Data is fundamentally good. That said, let me be blunt, this document is long overdue and is a mere white paper, not a set of laws! This is essentially a nice PowerPoint without the force of law behind it.

This is a POLICY, not regulation: “The Blueprint for an AI Bill of Rights is not intended to, and does not, create any legal right, benefit, or defense, substantive or procedural, enforceable at law.”

The Blueprint’s goal is to protect people from AI with five sensible guidelines. That they are sensible and not in the least controversial, or complete, is perhaps their greatest weakness:

The five guidelines:

People should be protected from unsafe or ineffective automated systems.

They should not face discrimination enabled by algorithmic systems based on their race, color, ethnicity, or sex.

They should be protected from abusive data practices and unchecked use of surveillance technologies.

They should be notified when an AI system is in use and understand how it makes decisions affecting them.

They should be able to opt out of AI system use and, where appropriate, have access to a person, including when it comes to AI used in sensitive areas such as criminal justice, employment, education, and health.

What was left out

Surprised by anything in these five guidelines? Not me and I view that as the problem.

So for fun, I'm going to propose guidelines 6-8 and yes these are controversial! But why were these left out?

6. Data Monetization: People should be protected from unreported and non-consensual data monetization. Data entrusted to AI’s should remain the property of the user and not be sold to data brokers without express consent.

Wouldn’t that be nice? The issue with data is that it doesn’t belong to you and you have no “rights" as to its use and no claim on any profits made from its sale or transfer.

7. Data localization: They should be made aware when data is stored outside of the US and be given an option to opt-out of systems where either the data or AI are in jurisdictions not subject to the guidelines.

I put that in because of the TikTok, WeChat and Alipay bans. Treat all foreign data storage equally!

8. Data segregation: They should be made aware when technology companies with suites of services combine data across services in an AI. Only data from the relevant consented service may be used.

This would challenge big tech's model by creating walls between their services. Google couldn't mine your browsing and email and use them in an AI. I can dream, can’t I?

Takeaways:

-This is a white paper, tone down your expectations but at least it's a start.

-The exceptions for law enforcement and the military basically let them do whatever they want. Be afraid.

-We need AI and data REGULATIONS, not white papers. The EU and China have them why not the US?

4. US CBDC decreases exclusion by 93%

A US CBDC can decrease the US’s financial exclusion by 93% without impacting bank deposits.

Next time you hear Fed Governors like Waller or Kashkari, both noteworthy CBDC opponents say, “CBDCs are a solution in search of a problem,” tell them to read their own Fed's research! Download: here

The Fed’s Bank of Dallas released a report this September stating that a CBDC could decrease the US’s unbanked by 93% with NO impact on bank reserves.

This research paper is a technical read, but let me take you through the basics.

Goal of the model:

Analyze the impact of introducing a CBDC on financial inclusion, and its potential adverse effect on bank funding in the USA.

The model focuses on two CRITICAL CBDC design parameters: 1) the fixed cost of CBDC usage and; 2) the interest rate it pays.

The goal is to find the best combination of cost and interest rates to increase financial inclusion.

What they showed by varying cost and rate:

1️⃣ Choice of money whether CBDC or bank depends on your wealth. Richer households prefer to hold deposits, which carry a higher interest, while poorer households prefer to hold paper money, remaining unbanked, despite carrying a zero nominal interest rate, for it carries no fixed cost.

2️⃣ CBDCs with high fixed costs (and high-interest rates) are adopted by wealthy deposit holders and increase inclusion by raising deposit rates. That is a big surprise. Why?

The poor are less attracted to the CBDC but are attracted to increased yield on deposits. So the number of unbanked decreases and has no impact on bank deposits because increased rates attract money.

In the US a CBDC 30% more expensive than the bank will increase inclusion by 71% due to increased yield with no impact on bank deposits

3️⃣ Optimal solution: CBDCs with low fixed costs (and low-interest rates) are adopted by cash holders and directly increase inclusion with no bank impact. Why no impact on deposits?

A CBDC with a low fixed cost allows to attract a large quantity of poorer workers, formerly paper money holders, which increases inclusion, all the while minimizing the mass of richer workers switching from deposits to CBDCs, which mitigates an impact on bank deposits.

In the US a CBDC 50% cheaper to use than the bank will decrease financial Exclusion by 93% with no impact on bank deposits!

Two more reasons why we need a CBDC:

The introduction of a CBDC provides additional competition, forcing banks to decrease their margins, thereby reducing the pass-through between the deposit and the loan rates.

Think more banks will help inclusion? Tripling the number of banks in the model would reduce the fraction of unbanked workers by only 30%!

Takeaway

Still think CBDCs are a solution looking for a problem?

Fed governors are callously writing off the 7 million (5.4 percent of total U.S. households) that are unbanked, and an additional 24.2 million or 18.7 percent of U.S. households have bank accounts but still rely on alternative forms of financial services, such as check cashing and money orders.

The Fed continues to be blind to advances in China, India and Brazil where digital payment clearly has a positive impact on inclusion.

Bonus read: Bain’s Technology Report 2022

People LOVED this tech report on LinkedIn with nearly 30,000 views!

No picture but download: here

I know why they loved it! Bain’s Technology Report 2022 focuses on what tech matters most a refreshing change from focusing on overly optimistic estimates of how big the market will be in 10 years. Does anyone believe these made-up numbers? Instead, Bain talks about the value proposition and strategy behind individual technologies.

This 80-page report is expansive and likely covers tech outside your comfort zone. This is why it is why I enjoyed it so much.

Three great sections that I highlight in the report:

🔹 Web3 Could Rewrite the Rules of User Identity pg 15

🔹 US-China Decoupling Accelerates, and Shockwaves Spread, pg 23

🔹 Customer Success: The Next Frontier of AI, pg 42

Takeaway

Kudos to Bain for not telling us these are trillion-dollar markets, but instead focusing us on what is likely to add near-term value.

Thanks for reading!

If you got this far I’m sure that you want to go down the rabbit hole, so subscribe!

More of my writing, podcasts, and media appearances here on RichTurrin.com

Rich Turrin is the international best-selling author of "Cashless - China's Digital Currency Revolution" and "Innovation Lab Excellence." He is number 4 on Onalytica's prestigious Top 50 Fintech Influencer list and an award-winning executive previously heading fintech teams at IBM following a twenty-year career in investment banking. Living in Shanghai for the last decade, Rich experienced China going cashless first-hand. Rich is an independent consultant whose views on China's astounding fintech developments are widely sought by international media and private clients.

Please check out my books on Amazon:

Cashless: (https://amzn.to/3RcC6PB)

Innovation Lab Excellence: (https://amzn.to/3C35Mcr)