Digital Dollar Comments: The Good, the Bad and the Ugly

The banking lobby and stablecoin Circle fire the first shots on the US CBDC and miss!

Comments to the Fed’s digital dollar report are in and at first glance they show the “Good Bad and Ugly.” For the record I am no fan of the Fed’s long-awaited report on a U.S. central bank digital currency (CBDC) and proclaimed that it read like a high school book report. I wrote about the report in great detail: here.

The Fed’s report on CBDC was published at the end of January and the comment period officially closed on May 20, 2022 meaning that we can now look at what representatives from banking, stablecoins, and crypto had to say about the report!

For those who may not recall the Fed sought public comments to a list of questions on Pages 21 and 22 of the report. My analysis in January as to why the Fed asked such basic questions has proven correct:

“By asking these questions, the Fed gives a gift to the banking sector whose lobbyists will go into high gear by finding disaster scenarios for each. This will help the Fed delay its CBDC for years and build one as favorable to banks as possible. Call me paranoid? Just wait until we get a review of the commentary! Banks loathe CBDCs, and their lobbyists are set to pounce.

My full analysis of this report is available on substack: Here

The Ugly: American Bankers Association

The ABA loathes the digital dollar but they resort to what author Mark Twain refers to as “Lies, Damn Lies, and Statistics” to make their case! Predictably, the ugliest response of them all!

It’s no surprise that the American Bankers Association (ABA) was going to come after the digital dollar with knives drawn. They did not disappoint and proved that my comments from January were correct! Download ABA response: Here

Their conclusion should not be a surprise:

As we have evaluated the likely impacts of issuing a CBDC it has become clear that the purported benefits of a CBDC are uncertain and unlikely to be realized, while the costs are real and acute. Based on this analysis, we do not see a compelling case for a CBDC in the United States today.

Rather than tear into the ABA’s document line by line I’m going to show you why their principal statistic is not just a lie or a damn lie, but what Twain would call statistics.

So here is the ABA’s cornerstone argument against the digital dollar where it predicts an end to banking as we know it: Pg 7

“ABA’s analysis suggests that deposits accounting for 71% of bank funding would be at risk of moving to the Federal Reserve. This could increase the average cost of funding for banks by approximately 170 basis points. Such an increase in average funding costs would be unsustainable and would undermine the economics of the banking business model."

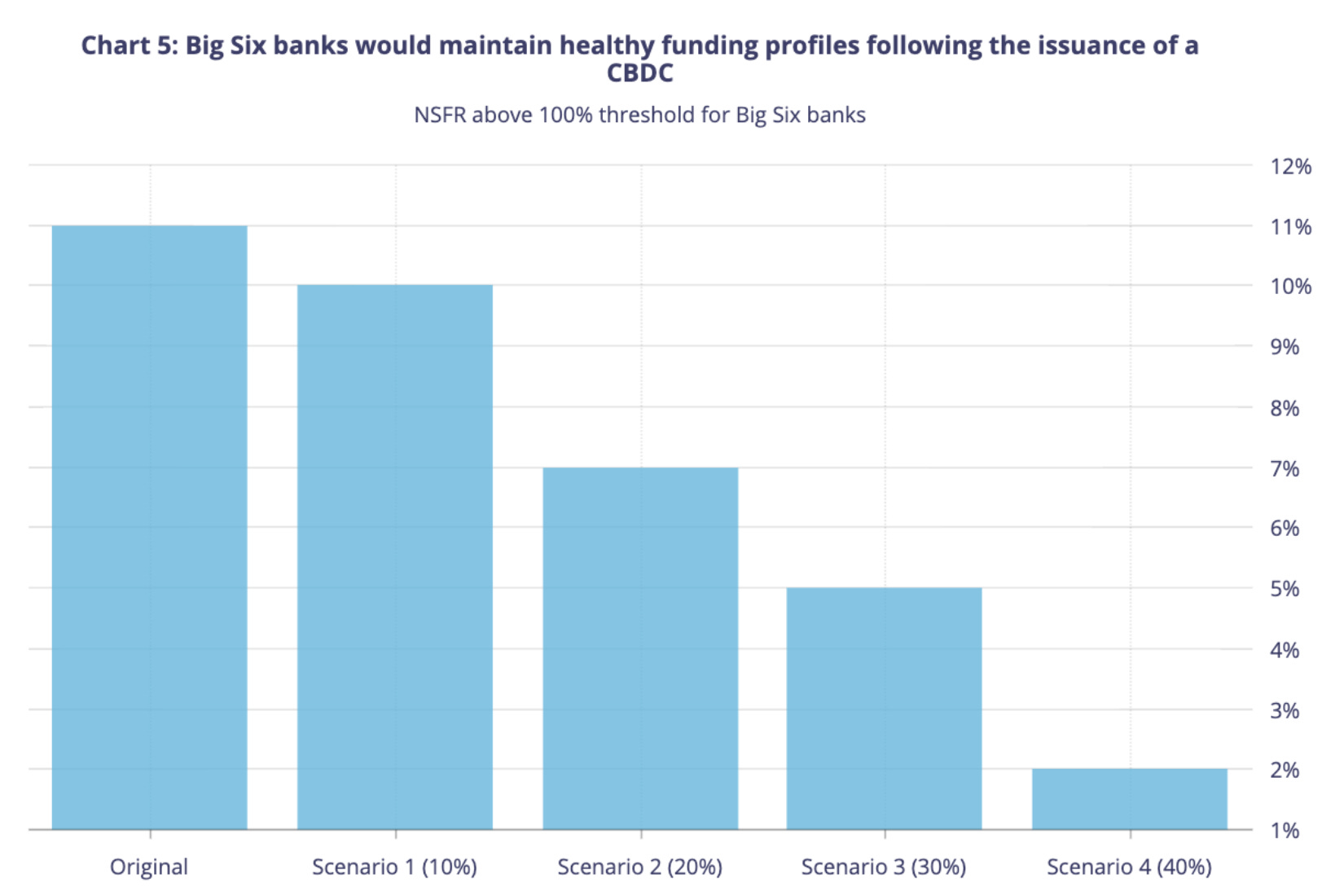

Imagine my surprise with the 71% number! Just the other week I wrote about Bank of Canada’s analysis showing that critical bank reserves would not be severely impacted by a CBDC!

Bank of Canada scenario analysis of a CBDC on bank deposits show that even under the most severe scenario where 40% of deposits migrate to CBDC bank funding is still healthy. Note that the Bank of Canada considers a 40% runoff of deposits worst case. Full report: Here

The ABA’s “analysis” how they got 71%

So let’s look at the -sophisticated- analysis that the ABA conducted in the appendix of their report: Pg 20

The ABA considers CBDC will impact both Transaction Accounts and Savings. The average of the orange and blue segments above is 71%. ABA response: Here

ABA’s logic is as follows:

"As of year-end 2021, banks held $16.9 trillion of transaction and savings account deposits on their balance sheets—reflecting 71% of total industry funding." (see above)

Now watch as the ABA goes for the kill shot!

"In the extreme case, where all transaction account and savings account deposits are converted into CBDC, the banking industry would lose 71% of its funding and would need to fill that hole with alternative sources"

The ABA’s 71% figure which they pass off as “analysis” assumes all bank deposits in the United States will convert to CBDC!

Since when are ALL DEPOSITS going to convert to CBDC? This isn't “extreme” but absurd! Just for comparison, we have the Bank of Canada considering a 40% conversion of deposits an extreme event.

What is amusing is that the ABA gives us numbers that we can use to refute this 71% claim within the report! On pg 7 they show what the real impact will be:

“Our estimates suggest that a CBDC account capped at just $2,500 would drain $446 billion in deposits to flow out of the banking system. A cap of $10,000 would lead to over $1 trillion in deposits leaving the system.”

So using the ABA’s figures the actual impact will be far less than placing “71% of funding at risk.” Using the ABA’s own figure of $16.9 trillion (rounded to 17) the impact will be:

$446 billion = 2.7% of $17 trillion in bank deposits

$1 trillion = 5.8% of $17 trillion in bank deposits

Let’s make it clear the assumption for CBDCs across the planet is that they have spending limits just as your credit cards have today. This is the norm, not unusual as the ABA suggests.

According to ABA’s own estimates, a digital dollar would have a 2.7% or 5.8% impact on bank deposits! Now lets go in for the “kill shot” ourselves. For comparison, these figures all fall within the Bank of Canada’s mildest scenario which shows the impact of a 10% reduction in deposits! The ABA is protecting the banking industry even if it means misrepresenting the figures.

The ABA's key statistic of claiming that “71% of bank funding is at risk” is beyond what Twain would call a “lie” or even a “damned lie.” Their entire argument against CBDC is based on a dishonest assumption of its impact on bank reserves.

Ironically, the ABA does actually give the real figures for CBDC impact on deposits because they are so modest no one would take them seriously! So they simply lied and used the more dramatic 71% figure.

The ABA should be ashamed of themselves!

The Bad: Stablecoin Circle

Stablecoin Circle also takes shots at the Digital Dollar in a response that is not as ugly as the ABA’s but is certainly bad. Circle is going for a power grab in the ultimate contest over who will issue your digital money, government or corporations by requesting that Circle receive “digital legal tender status.”

Download Circle’s response to the Fed: Here

First, let me say that I quite like Circle! They are the best of all stablecoins and I will gladly use them for payment because the Fed's CBDC is years away!

Circle’s main points are summarized here:

Many of the potential benefits of a CBDC detailed in the discussion paper are already being met by existing blockchain-based payment system innovations.

Bringing stablecoins like Circle’s USD Coin (“USDC”) under common-sense regulatory guidelines would ensure proper supervision over an asset that is already achieving many of the Federal Reserve’s objectives in a potential CBDC.

If a digital asset behaves like a currency or payment system, it should be afforded the benefits of digital legal tender status or conformity with well-laid money transmission, e-money, financial markets infrastructure and prudential rules.

Still Circle's comments demand reply:

Circle is not being forthcoming about the bigger issue of whether corporates or gov’t should issue your money? Circle believes that no digital dollar is needed and that stablcoins should fill this role. Profiting on your payment is their right. So now we’ll have banks, cards, and stablecoin companies all profiting off our payments. Where is the "disintermediation" we were promised?

CBDCs are necessary gov’t infrastructures like bridges and roads. Taxpayer support for CBDC is no different than paying for the treasury which issues notes.

Circle’s request to grant stablecoins “digital legal tender status” is a power grab and the most absurd thing they ask for! The US's official legal tender must be issued by the gov’t and outsourcing this job to Circle is simply insane.

Stablecoin use must be the payer or receiver's choice! Declaring Circle “legal tender” would give it official status and would mean that you would have to accept a stablecoin for payment which is demonstrably inferior to cash! No one should be forced to accept a stablecoin or forced to use a CBDC!

Circle claims that CBDCs would potentially hurt inclusion! Circle’s logic is astounding: “because the public’s confidence in government institutions and banks has been declining, a CBDC could make the unbanked or underbanked even less likely to engage with financial institutions.”

So Circle thinks that delivering aid payments, a real example of inclusion, via stablecoin would be better received than a US digital dollar? Get real! Can you imagine the confusion? I got “Circle” in the mail from the government what’s that?

Circle is a great stablecoin, and I hope to use it soon to pay for things in the US. I like them! Is that positive enough for crypto fans who declare I am biased? Still, they are another corporate that wants your payments just like Visa or your bank. I want a digital payment system fit for the digital era that frees me from profiteering, data brokers, and risk a right shared by all citizens.

Stablecoins are corporate-issued money and will -always- be inferior to gov’t issued CBDCs. Putting your cash in stablecoins even if the companies are banks is no substitute for a Fed-backed digital dollar. I’ll spare you the details and send you to the FDIC’s list of failed banks: here

This long list says more than I ever can why CBDC will always be superior to stablecoins! Even if stablecoins are regulated as banks their is no guarantee that a stablecoin won’t end up on the FDIC’s list of failed banks someday.

A CBDC in your digital wallet will never end up on this list and that is why stablecoins will always be inferior to CBDC even if more convenient for certain tasks.

The Good!: Crypto, Stellar

Finally a brief comment on the best response I saw from of all places cryptocurrency firms “Stellar” issuer of XLM coin.

Stellar’s response to the Fed can be found: Here

Stellar’s response was the most upbeat of them all saying:

Can a CBDC promote financial inclusion? We think so.

A well-designed CBDC could have a positive effect on inclusion and the economy by expanding access to and usage of affordable financial services.

I give credit to Stellar for actually acknowledging the good a CBDC can do in promoting inclusion. I find it refreshing given Circle’s poor attempt to shed doubt on CBDC’s ability to assist with inclusion.

Stellar goes on to make a point that neither the ABA or Circle makes:

“A CBDC expand modes of payments beyond financial institutions”

This is a great point because the ABA’s commentary assumes that CBDC users will be routed through the banking system. This is clearly in the ABA’s interest but not in the interest of financially excluded CBDC users.

With CBDC we will have the ability to expand at least basic banking services to mobile phone providers and even large retailers like Walmart. The idea behind CBDC is to give the excluded access to financial services in new more convenient venues that are not banks.

Let’s face it if the excluded aren’t going to banks today in the US, it’s unlikely that centralizing CBDC services at banks will do much for them. The whole idea behind CBDC is to allow a limited degree of banking without banks. Note my use of the term “limited” which in most cases means low-value transactions for our most vulnerable.

So kudos to Stellar who wins the title of “good” compared to “bad” and “ugly.”

Rich Turrin is the international best-selling author of "Cashless - China's Digital Currency Revolution" and "Innovation Lab Excellence." He is an Onalytica Top 100 Fintech Influencer and an award-winning executive previously heading fintech teams at IBM following a twenty-year career in investment banking. Living in Shanghai for the last decade, Rich experienced China going cashless first-hand. Rich is an independent consultant whose views on China's astounding fintech developments are widely sought by international media and private clients.