Fast Payments are ROCKING the World: Four Key Features Turn Users Into Fans!🤟

Fast payment success as in Brazil, India and China, is design dependent

Fast payments ROCK! 🤟 They are taking the world by storm and are at the forefront of the digital payment revolution.

The BIS looks at fast payment systems in 13 countries and breaks down success into four key areas that help convert users into fans.

What’s not to like? Secure, low-cost instantaneous payments are easy to love unless you’re a bank!

That’s why they’re taking off, bringing inclusion to developing economies and unparalleled convenience to developed ones.

👉TAKEAWAYS

The BIS recognizes four key features for adoption:

1. User focus

One extremely successful way to focus on users is to use payment “aliases” to make payments easy and intuitive. Aliases can be anything from a mobile phone number to a national ID, e-wallet number, or corporate ID for businesses.

This is one reason why systems like Brazil’s, Pix, and India’s UPI took off. Both allow payment aliases without a bank to make and receive payment.

Other features like cross-border payments and standardized apps can also keep the focus on users.

2. Infrastructure

“Adoption of fast payments tends to be more widespread when the central bank owns the FPS.” The best examples are FedNow, PIX, and UPI, where the government provides specialized real-time gross settlement systems.

But there is no rule to this! Sweden and China do well with private systems!

3. Rules

Unsurprisingly, when non-banks are allowed to participate, there are more users in fast payment systems. Who gets to participate is dependent on the rules, and non-bank users are not always welcome.

Banks own Sweden’s Swish/BiR, so non-banks are not allowed. This may be fine for advanced economies, but M-pesa in Kenya wouldn’t have worked without local non-bank kiosks.

4. Governance

“Because payment systems have characteristics of a public good, these aspects can reflect the ultimate objectives of an FPS and thus affect end-user adoption.”

I love the use of the term “public good” because that is exactly what digital payment should be. As an example, look at how India views UPI as “public infrastructure!” (See my article on India’s DPI below.)

It is important to note that UPI views itself as a partnership with the private sector and has banks in consultative groups. This contrasts with Sweden or even China with fully private systems.

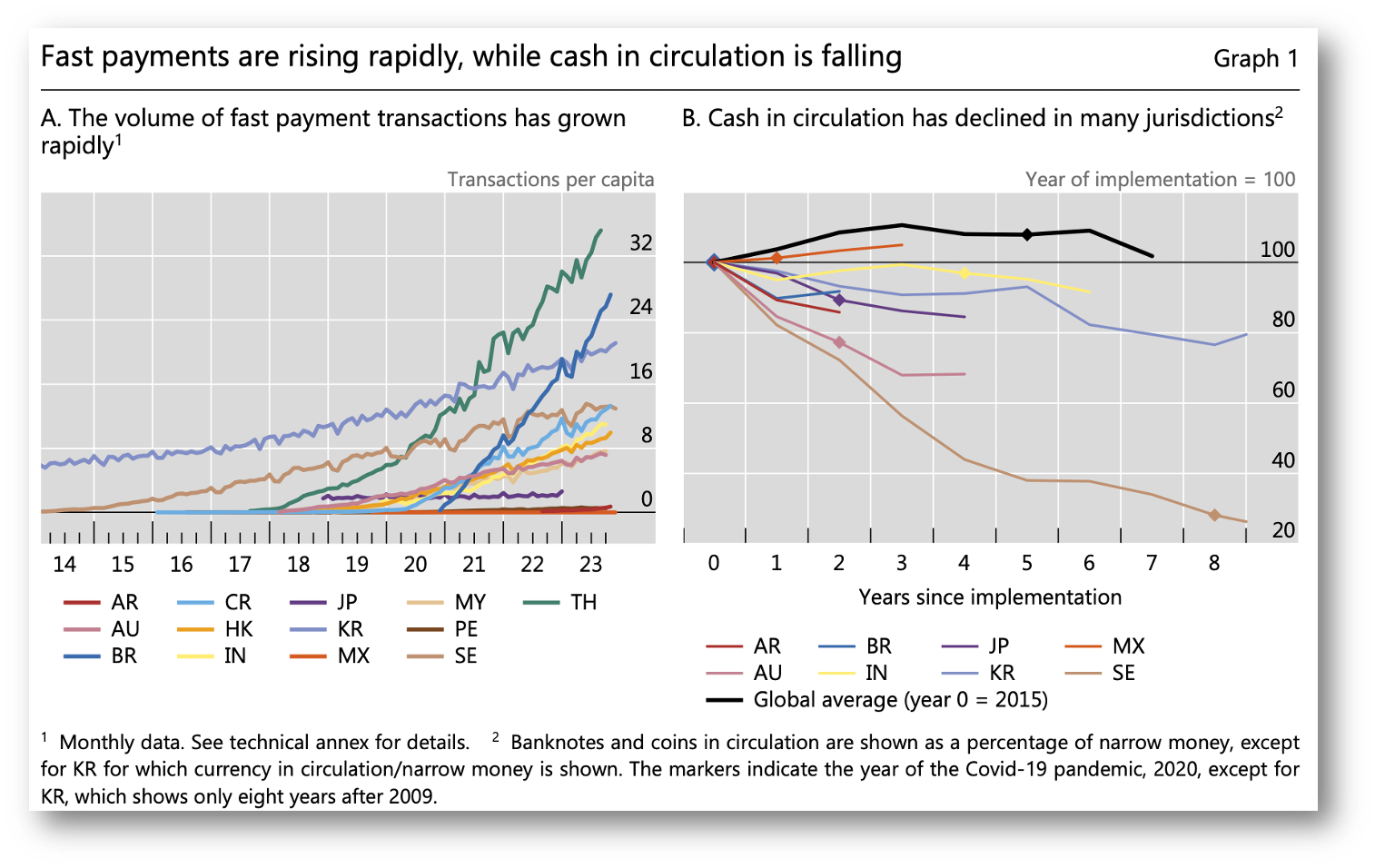

Watch as for both developed and developing nations cash in circulation is declining as fast payments take off. Look how cash circulation collapsed in Sweden (SE) in the graph at right.

👊STRAIGHT TALK👊

There is no “magic formula” that will make fast payments successful.

Each country is rolling them out on their own in accordance with their needs for both users and technology. What works in Brazil may not work in Sweden!

Despite their being no formula the BIS is clear that systems owned by the central bank with non-bank payment service providers seem to work best.

Surprised?

Don’t be! Banks loathe fast payment systems, and the struggles between India’s banks and UPI are legendary. Banks can’t make money if payments are free.

Unless the central bank gets involved banks won’t push for cheap payments or allow non-banks to participate in their monopoly. It’s only logical that banks would resist these changes.

One final thought. Fast payments are distant cousins to CBDCs, and if people love fast payments, they’ll love CBDCs. Features like offline payments and programmable payments will be game-changers!

Thoughts?

Hey, do you have anything to say about my articles? I and others in our “Cashless” community would love to hear it!

Don’t pull your punches. Tell me why I’m right or wrong, but don’t miss this opportunity to leave a comment!

Thank you to all my subscribers who have been sharing Cashless! You are now the No. 1 driver of subscriptions, and prove that word of mouth still works better than X!

Join the community by subscribing! You’ll be glad you did!