Financial Inclusion in Africa and the Mid East Won't Come From Mastercard but India's UPI!

India style "Digital Public Infrastructure" is better than Mastercard!

I have nothing personal against Mastercard, but what Africa and the Mid-East need are payment systems modeled after India’s UPI, not Mastercard.

Cards as digital payment are wholly unfit for bringing nationwide inclusion. They are private companies and can never fully serve public interests when the rural poor are considered nothing more than unprofitable.

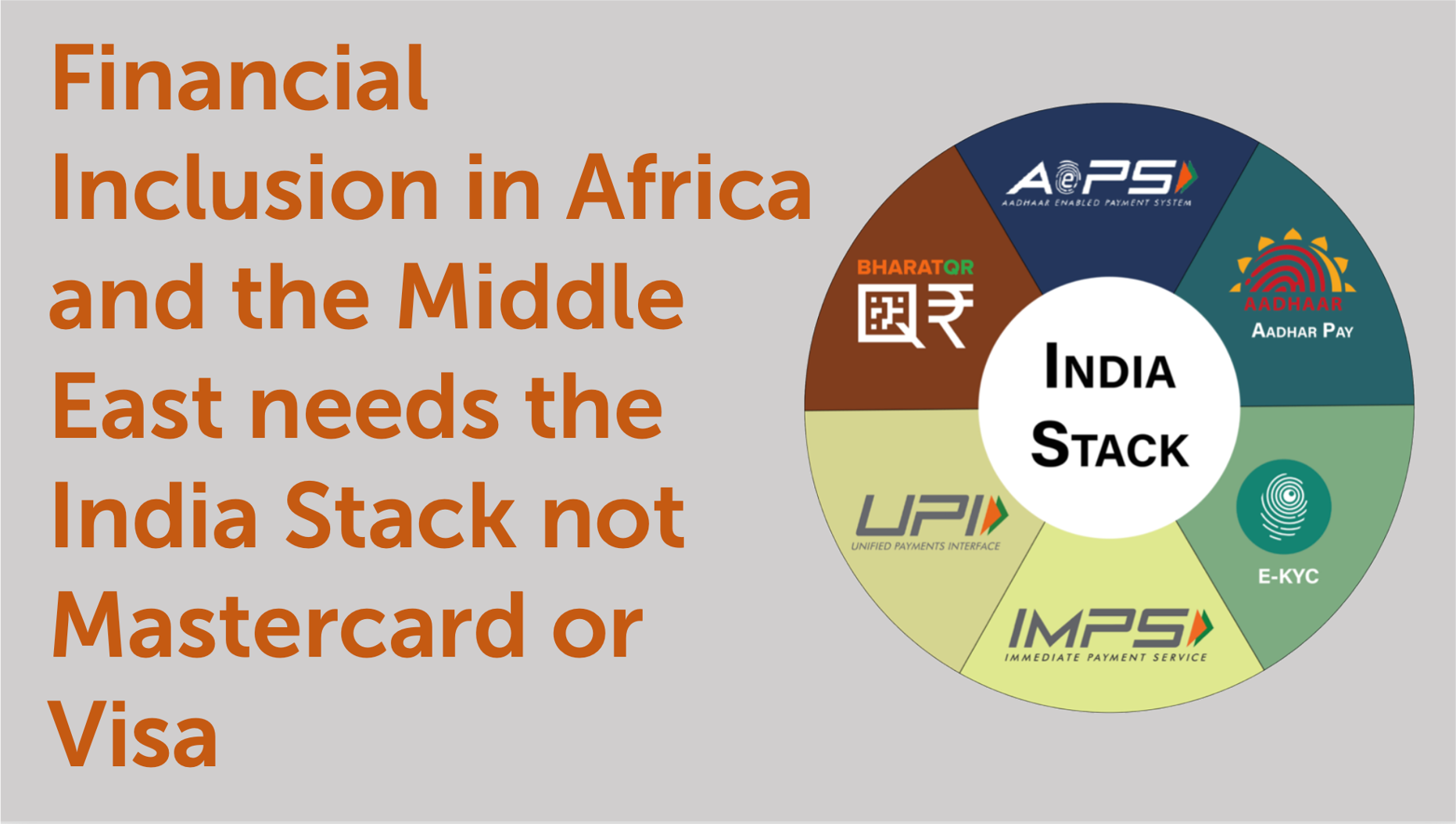

Africa and the Middle East need “The India Stack,” which has a proven record of bringing UPI payments to over 1.4 billion people through digital public infrastructure shared by all.

Fortunately, report author OMFIF points this out, even though I’m sure Mastercard, who paid for the study, probably wanted it deleted!

👉TAKEAWAYS

Below are the roadblocks to inclusion, followed by my analysis on how UPI solved these problems!

1. Low levels of financial and digital literacy among citizens and enterprises are noted as the main barriers to financial inclusion.

🔹Same as in India! Cooperation with public-sector payment providers greatly helped India’s financial literacy problems. Telecoms and payment companies spread UPI and literacy!

2. Economic sustainability in financial inclusion is vital, but not a top priority for survey respondents as only one-third said their financial inclusion strategies are aligned with this principle.

🔹 This is the problem, individual commercial payment providers are trying to figure out how to make money when the government should support key elements of the system.

3. An integrated financial system with interoperability is critical for inclusion, yet challenges related to infrastructure, access and costs persist.

🔹 There can be no more interoperable system than nationwide digital public infrastructure! This is no worry at all in India!

👊STRAIGHT TALK👊

The India stack was behind India’s UPI revolution, and has proven success in a developing nation.

UPI’s “secret sauce” is government-sponsored “Digital Public Infrastructure” (DPI) and the belief that banks and governments can collaborate on payments.

With all due respect to Mastercard (MC), it’s hard to see how cards will ever bring the large-scale advances in financial inclusion the regions require.

Cards suffer from two real problems: first, they charge a percentage on each transfer, and second, they generally need a bank as an intermediary.

Card companies like MC have worked on non-bank-based stored value cards with low transfer fees. The report highlights MC Farm Pass which it trialed in rural areas. This is great, but there is no way Mastercard can do what a UPI or PIX did

The OMFIF must have fought with MC to put this sentence in:

”India's digital public infrastructure – the India Stack – had been recognised as a potential model for countries seeking to boost levels of financial inclusion. The India Stack is interoperable and allows private companies to build apps integrated with state services, allowing consumers to access a wide range of services.”

I'm sorry, but Africa and the Mid-East don’t need Mastercard; they need India’s UPI and “The India Stack.”

Thoughts?

Thank you to all my subscribers who have been sharing Cashless! You are now the No. 1 driver of subscriptions!

Join the community by subscribing! You’ll be glad you did! All it takes is your email!

Share