Fragmentation in European Payments As Rivalries Heat Up

European payments are changing fast, and the digital euro will be a disruptor.

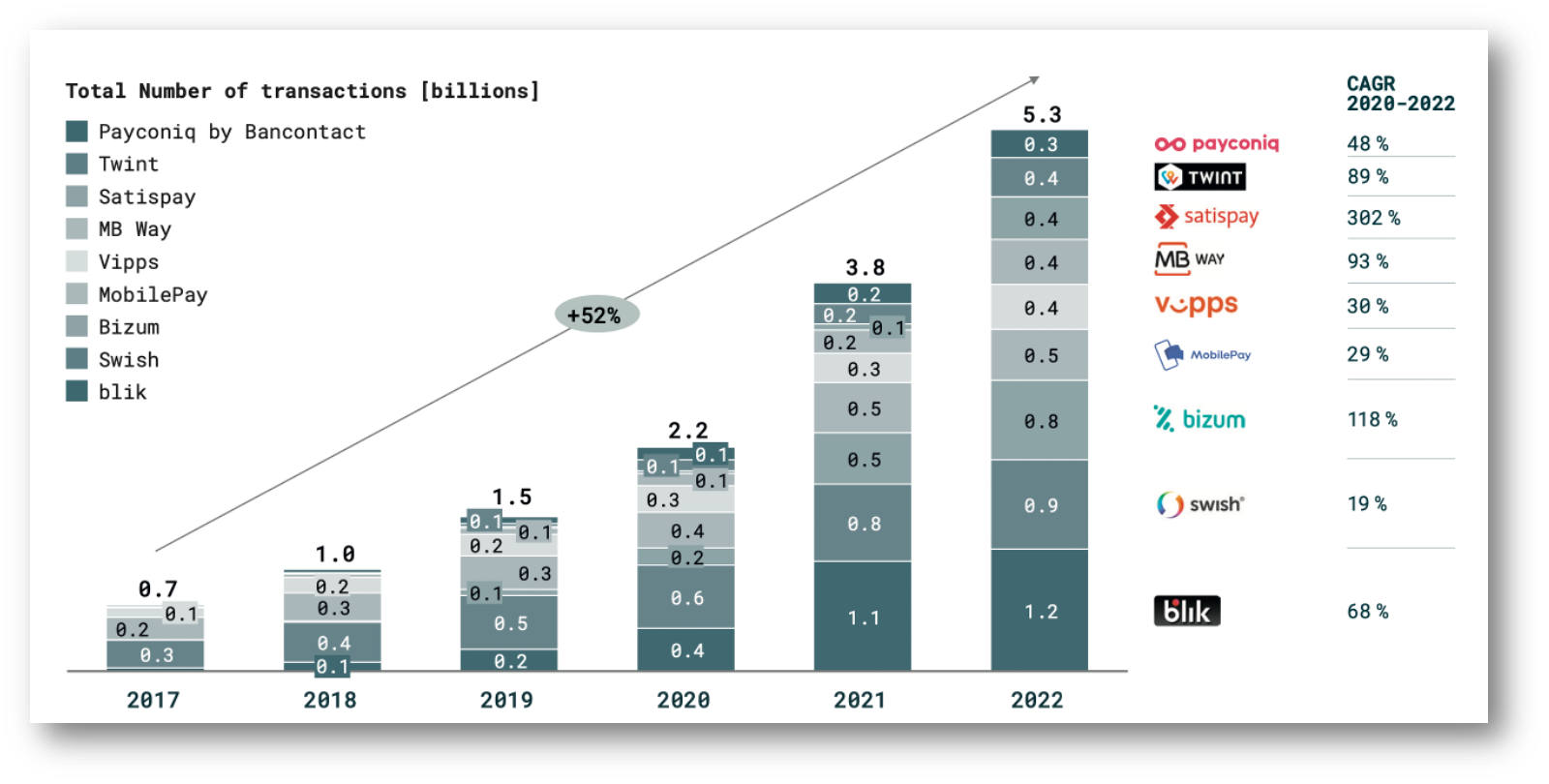

Kudos to Arkwright Consulting for producing the best report yet on the EU payment system, which shows that digital wallets are growing at 52% while cards are up a mere 9% over the same period!

While digital wallets may be taking a bite out of cards, as they are across the globe, Europe faces fragmentation in that each nation has a national payments champion.

There is no pan-EU digital wallet yet unless you factor in the US’s Apple Pay and Google Pay, which work on US credit cards. So, for the moment, the EU doesn’t have a single system that works everywhere.

The ECB is well aware of this, and one rationale for the digital euro is to develop a native payment system that is not dependent on US cards or big tech.

👉TAKEAWAYS

Arkwright Envisions Three Scenarios for EU Payments:

1. Single European solution: The emergence of a dominant European mobile payment method likely led by the EPI, subject to decisive political backing and adequate financing.

2. Multi-country clusters: Cross-regional clusters formed through the expansion and consolidation of existing systems, supported by technical harmonization and inter-operability, e.g., through industry alliances such as the European Mobile Payment Systems Association (EMPSA).

3. Continued fragmentation: Persistent fragmentation with numerous local options and bank-specific apps, with international wallets and payment schemes remaining the common solutions throughout the region.

Leading EU payment providers show an astounding 52% CAGR over the period, beating that of credit cards at 9%.

👊STRAIGHT TALK👊

So which scenario, or better yet, which scenarios, will the EU get?

How about all of them, with an emphasis on fragmentation?

If that sounds like a mess, it is! But there is good news, at least from my point of view!

The EU is getting a single pan-EU digital wallet solution! Fear not, the digital euro is coming to the rescue! While we still have to wait until roughly 2029, it’s coming.

I confess I’m not quite sure why Arkwright didn’t mention the digital euro could it be an oversight?

So what about “multi-country clusters?” Arkwright does a fabulous job of explaining the European Payment Initiative (EPI), which now spans Benelux, France, and Germany and will expand as it launches its “wero” mobile wallet.

As great an idea as the EPI is, it isn’t going to supplant individual nations' payment leaders, who are already deeply embedded in the economy. See below.

For example, look at Sweden’s SWISH with 78% market share, could EPI replace it? No way, the best EPI can hope for is some form of interoperability.

If the EU learned anything from watching digital wallets in Asia –and that’s a big ask– they should know that payments are highly localized.

Until the launch of the digital euro’s pan-EU payment system, a hodgepodge of companies will fight for local digital wallet dominance.

And when EU citizens cross borders, there’s always Visa…..

…..at least until the digital euro launches.

Thoughts?

Share this article with friends, on social media, or substack. Try it! It’s the nicest way to say thanks!

For all those who have shared Cashless, you have my special thanks!

Joining our community through a simple email subscription is more than just a step, it's an exciting journey down the rabbit hole to our future. You’ll be glad you did!

Sponsor Cashless and reach a targeted audience of over 50,000 fintech and CBDC aficionados who would love to know more about what you do!

Agree, the absence of digital euro in their analysis seems like an oversight. Likewise, no mention of MiCA “stablecoins”, which could also become a valuable tool in the European cross-border payments market.