Part 1: Geopolitical Fault Lines Dim Central Bank's Love of CBDC

CBDCs contribution to a fragmented payment system gives some banks pause.

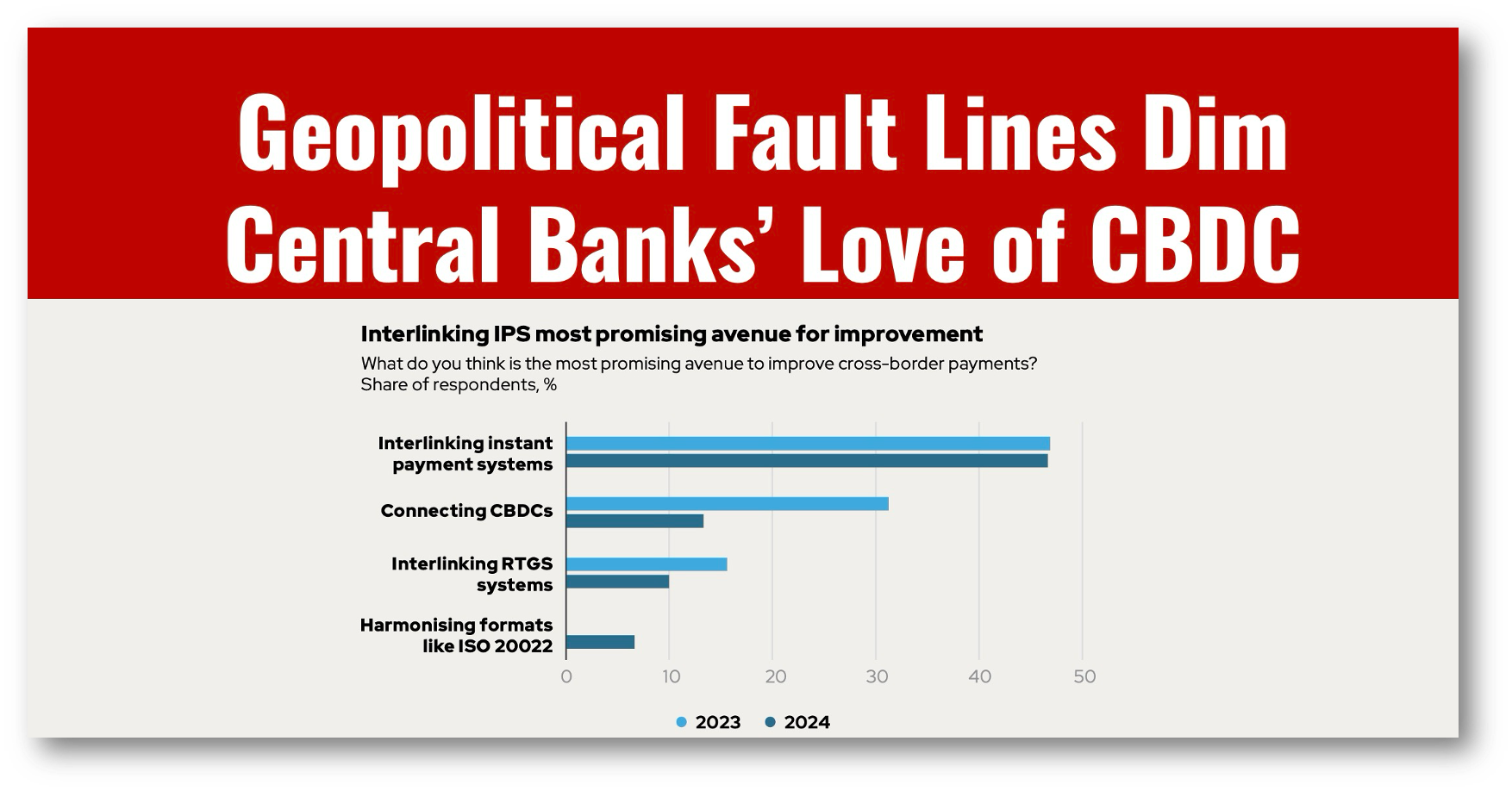

The OMFIF’s Future of Payments report shows a big difference for central bankers’ support for CBDCs this year with the realization that they will fragment the payment system along geopolitical fault lines.

This year, only 13% of central bankers say CBDC is the best way to improve cross-border payments compared to 31% last year.

That’s a bit of a shocker, and the primary reason is that bankers finally realized that there would be no “unified” global payment system for CBDCs.

It finally hit that CBDCs would hasten the transition to a fragmented payment system between the US and BRICS nations, and central bankers didn’t like that one bit.

👉TAKEAWAYS

68% of central banks say transaction costs are a challenge for cross-border payments.

33% of central banks say that more than 10% of the institutions they supervise will miss the ISO 20022 deadline.

13% say connecting CBDCs is best for improving cross-border payments, down from 31% in 2023.

47% say interlinking IPS is the best way to improve cross-border payments.

44% say harmonising legal and regulatory frameworks is the biggest barrier to interlinking IPS.

85% of central banks give or plan to give non-bank payment services providers access to real-time gross settlement systems.

76% of central banks see wholesale CBDC and tokenised deposits operating in a tokenised ecosystem.

15% of central banks are working on tokenising cash, but 33% say they expect to be within three to five years.

👊STRAIGHT TALK👊

So what’s behind central bankers and their cadre’s change of heart?

This year, the shift of support was toward “Instant Payment Systems” (IPSs), which had five successful trials in Southeast Asia. Note also that IPS may also be referred to as Faster Payment Systems (FPS).

See my article on how SE Asia is connecting QR code payment systems

Instant Cross-Border Mobile Payments are Becoming a Reality in SE Asia

Simple is always best, and one way to get immediate cross-border payments is to connect Asia’s wildly successful QR-based instant payment systems (IPS).

There’s nothing wrong with IPS systems, and I quite like them as long as you realize they carry only small amounts of money across borders. And that is a problem!

The central banks’ support for IPSs is the equivalent of supporting the application of a band-aid to a cross-border payment system that is gushing arterial blood. It’s an issue of scale.

Central banks like IPS systems because, unlike CBDCs, they don’t upset the status quo, no nation can de-dollarize or fragment a payment system using IPSs!

Another advantage is that they do not disturb commercial banks who maintain their lock on payment charges. Even if IPSs charge lower fees, banks make up for that in large number of payments.

Always remember that commercial banks loathe CBDC because it fundamentally changes their centrality in payments and, with it, their ability to charge fees.

IPS systems are far less disruptive and do not require a “replumbing” of the financial system as CBDCs do. This undoubtedly makes IPS easier for central banks, whose role becomes supervisor rather than builder, as with CBDCs.

Central bankers can appear to be doing something by pursuing linked IPS systems, while nothing changes for most payments. It’s the easy way out!

Yet still there is hope! It turns out that central bankers still support CBDCs as part of their tokenization programs. A stunning 75% support wholesale CBDC tokenization while 58% support retail CBDC!

So don’t count CBDC out just yet!

Please share on Substack with a restack!

Readers like you make my work possible! Please buy me a coffee or consider a paid subscription to support my work. Thank you!

Sponsor Cashless and reach a targeted audience of over 55,000 fintech and CBDC aficionados who would love to know more about what you do!