The US-China-Ru divide, programmable money and survival bunkers, The US falls behind in digital banking, and SE Asia is going digital

My interview with CFO magazine on China's economic slowdown

1. Our Divided World

2. Singapore’s Programmable Purpose Bound Money

3. Digital Banking and why the US is Behind

4. Southeast Asia’s digital decade!

5. China’s Economic Slowdown

Vibrazione Universale, Hsiao Chin, 1965, Song Art Museum Beijing. I think we could use some “universal vibrations” right now to slow the divide! According to the Chinese cosmology, circle symbolizes the sky, while square (similar to the rhombus) symbolizes the earth.

1. Our Divided World

We live in a divided world and the shocking results of this survey show just how differently the world sees the US, Russia, and China.

This is report is absolutely stunning and shows not just how people view our divided world but why it’s splitting in two, once again. Unlike the cold war, however, the divisions are less clear.

Download: here

Living in China I see how dramatically our world is being cleaved in two. It’s not theoretical to me but part of my daily life. This apolitical report lays out exactly how and why. You need to read this.

The shocking results of this report come from an analysis of 30 global surveys spanning 137 countries. To head off the inevitable comments about surveys in repressive countries, the authors counter this on pg 7.

The survey results are astounding:

🔹 Liberal and illiberal world spheres:

Among the 1.2bn people who inhabit the world’s liberal democracies, 75% now hold a negative view of China, and 87% a negative view of Russia. However, for the 6.3bn people who live in the rest of the world, the picture is reversed. In these societies, 70% feel positively toward China, and 66% positively toward Russia.

🔹 China leads the developing world:

For the first time ever, slightly more people in developing countries 62% are favorable towards China than towards the United States 61%. This is especially so among the 4.6bn people living in countries supported by the Belt and Road Initiative. But China is losing the developed world where 5 years ago, 42% held a positive view of China, compared to 23% today.

🔹 Russia’s international influence lies outside of the West:

75% of respondents in South Asia, 68% in Francophone Africa, 62% in Southeast Asia continue to view the country positively in spite of the events of this year. In the west, positive views fell from 39% 10 yrs ago to 12% following the Ukraine war.

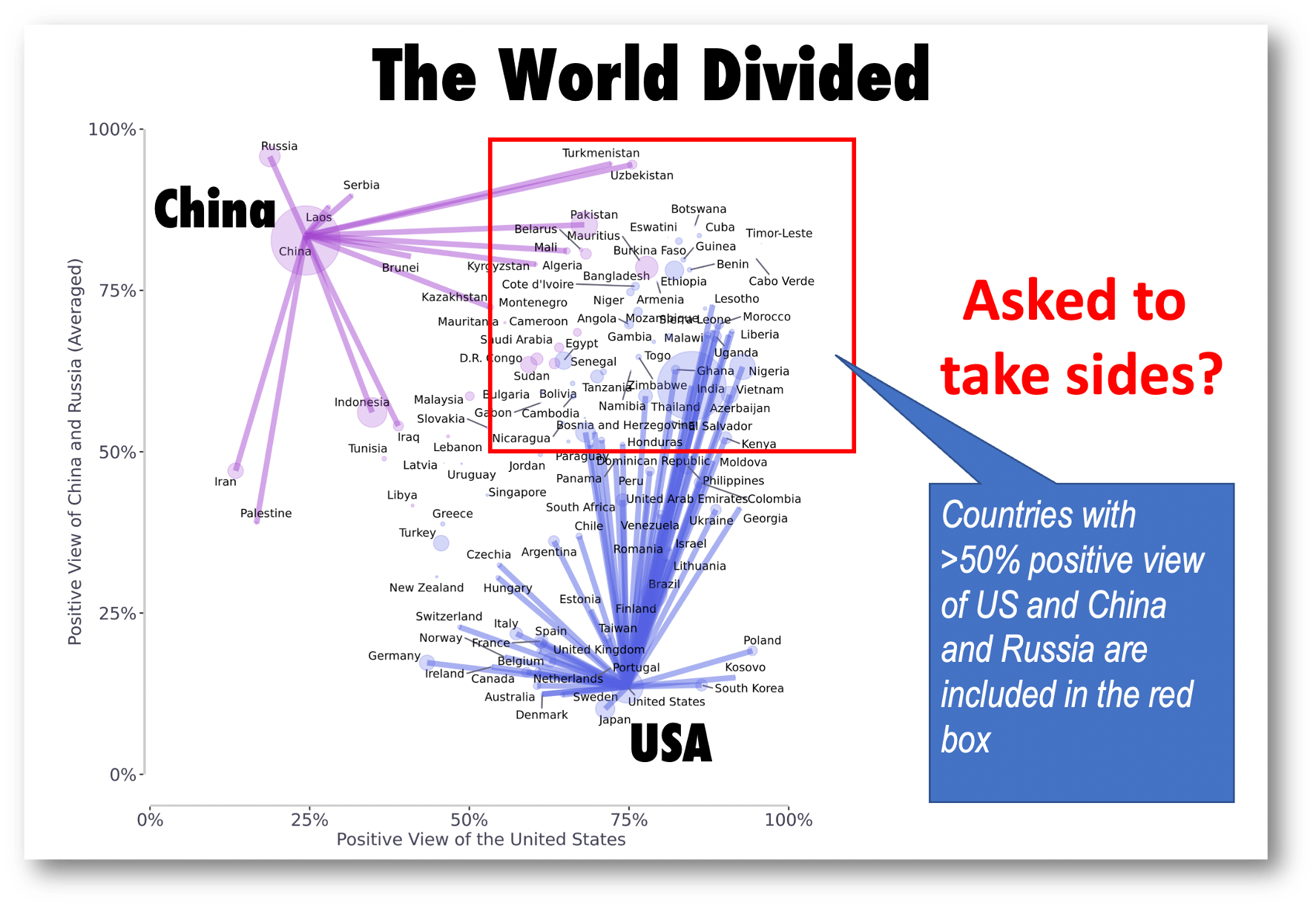

🔹 Positive views of the US: (fig 11)

Attitudes have polarised – with western nations more than ever behind the US, yet a much longer tail of countries where public opinion is ambivalent or even hostile to the US, led by Iran, China and Russia. The average perception of the US in the world as a whole has become more positive over time.

Make no doubt about it more countries have populations that like the US best. Still what happens to all the nations that like everyone? Will they be asked to take sides as our world splits into two camps? There are roughly 55 nations in the red box above that have greater than 50% of their populations that like all of the countries!

🔹 Cold war vs. today:

American attitudes towards Russia have not been this bad since the mid-1950s. Meanwhile, though China has not launched any similar war, opinions of the country fare little better.

🔹 China’s rise:

China’s rise is leading to a bifurcation in the global economy. Countries in Latin America, Eastern Europe and southern Africa continue to rely upon western investment, aid, and exports. Yet a large and growing bloc of countries now count China as their primary trading partner.

Takeaways:

The cold war division was easy, the divisions were clear capitalists and communists, black and white.

Today’s division is based on whether regimes are democratic or authoritarian and liberal or illiberal. Areas with shades of grey!

The division will deepen and will require more nuance than simply "friend or foe" to navigate.

2. Singapore’s Programmable Purpose Bound Money

STOP THE INSANITY OVER PROGRAMMABLE MONEY! Singapore shows why we need it with “Purpose Bound Money.”

Programmable money is here and will be a key tool used in providing government social benefits in the future. It’s not new we already have programmable money through paper vouchers or debit cards with spending limits. Download: here

Want to buy a survival bunker?

Not a day goes by without someone ranting about programmable money being the end of freedom or civilization. Usually, they are selling crypto, gold, or survival bunkers! Look closely next time, you’ll find I’m right!

As a prelude to a CBDC and for “experimental and exploratory purposes” Singapore is launching an experiment with digital Singaporean Dollars (SGD) that shows just why programmable money is needed.

Singapore is trialing digital SGD to replace small parts of its extensive social payment paper voucher system with a new programmable digital -paper- voucher that it calls “Purpose Bound Money” (PBM).

PBM enables senders to specify conditions, such as validity period and types of shops, when making transfers in digital SGD. The experiment will test gov’t vouchers, commercial vouchers (Grab), Gov’t payouts, and gov’t learning accounts.

This is practical because the existing social payment vouchers are already dedicated to specific uses, Digital vouchers decrease program overhead, fraud, loss in transit, risk to accepting businesses, and payment waiting time.

The new vouchers can even allow interoperability across voucher programs to get more money to the vulnerable! Crypto fanatics, please tell me why this is the end of freedom and do better than the gov't will block your money.

The cost of social payments in the US

Whatever country you live in you have social payments and could use a better way to ensure that the money goes to the needy and isn't lost in fees, or stymied by the process.

Need an example? Look to the USA where Fed governors still can’t see why the US needs a CBDC. Here’s the real cost of government-issued debit cards:

In 2019 the US issued $136bn in prepaid debit cards which issuers collected $490 million in fees! Half a billion dollars that should have gone to the poor wasted!

Technical details are scant but digital SGD can be either CBDC, stablecoins, or tokenized deposits and for now, can be implemented on ERC-20 smart contracts on a ledger-based system. MAS is promoting the concept and use case, not the tech stack.

So how does it work?

Traditional fiat currency is transferred from the government agency to the digital SGD issuer.

The digital SGD issuer mints the digital SGD for the government agency’s purpose.

A paper PBM voucher is created for the government agency’s distribution to eligible citizens or businesses for spending at approved institutions.

Takeaways:

Singapore still doesn’t see the need for a CBDC but does see the need for programable money!

Digital cash's crowning achievement is programmability and PBM is the best use case yet! Far better than apes!

Why programmable Ether is considered godlike and programmable CBDC the spawn of Satan is beyond me.

3. Digital Banking and why the US is Behind

The future of digital banking in the US depends on better regulation, without it the US will continue falling behind!

Interesting to read how open banking in the EU and many other countries leads the USA. Like it or not this is largely due to regulatory pressure and banks won’t change until regulators impose it upon them.

Download report: here

This Money, 20/20 USA edition of The Future of Digital Banking, makes it clear that even bankers want better regulations! Having delayed them for years, the US finds itself behind the curve in digital banking.

I can't cover every chapter in this report, so I'll focus on the authors' comments on regulations! The authors’ quotes are followed by my own comments.

🔹Chapt 1: Open banking: the next frontier:

Open banking currently lacks regulation in the United States and is strictly market-led. However, the CFPB's Dodd Frank 1033 will eventually change that.

Right now, the US lags behind Europe in terms of establishing a regulatory framework that governs the way banks and fintechs collect consumer data.

Note that the EU is in the lead, and that like them or not regulations are required for the industry to change. Being market-led has not produced open-banking innovation.

🔹Chapt 2: Vulnerability and Protection:

The US has taken more of an industry-led approach to open banking, unlike that of the UK and Europe which took a regulatory approach.

The CFPB director is on it: "CFPB will be looking to harness technology in ways that give American families the power to more easily fire poor-performing banks. We can only accrue the benefits of competition if customers can vote with their feet."

The US is even behind its neighbor Mexico which published its rules for open banking as part of an update to their 2018 'Fintech law.'

Note that an “industry-led approach” is the authors way of saying that the US does little! And its clear why if EU style regulations assist customers “voting with their feet” banks want no part of it. That Mexico is ahead of the US, should tell you something!

🔹Chapter 3: Consumer trends:

Personalization, embedded finance, and digital ubiquity require a reimagining of the standard banking business models.

While embedded finance revolutionizes the way we buy goods and services, it could also reset how we bank — and even redefine what we think of as a bank.

Banks wanted to delay "redefinition" as long as possible and were largely successful. Now they have to pay the price, actually their customers pay, as they come from behind.

🔹Chapt 4: Offence and Defense:

Financial regulation on divisive topics such as DeFi and stablecoin is expected to be determined by the results of midterm elections.

Central America has seen an emergence of digital wallets, crypto usage, and QR-based transactions. Mexico specifically is a large market for growth for neobanks, with large European players such as Revolut expanding to the nation.

Once again we see EU and Mexico in the lead!

Takeaways:

Incumbent banks dominated the market and regulators for so long that they were instrumental in delaying digital regulations that would lead to change.

As a direct result of trying to maintain the status quo, they were leapfrogged by the EU and its southern neighbors.

US banks are now playing catch up and new regulations are required!

4. Southeast Asia’s digital decade!

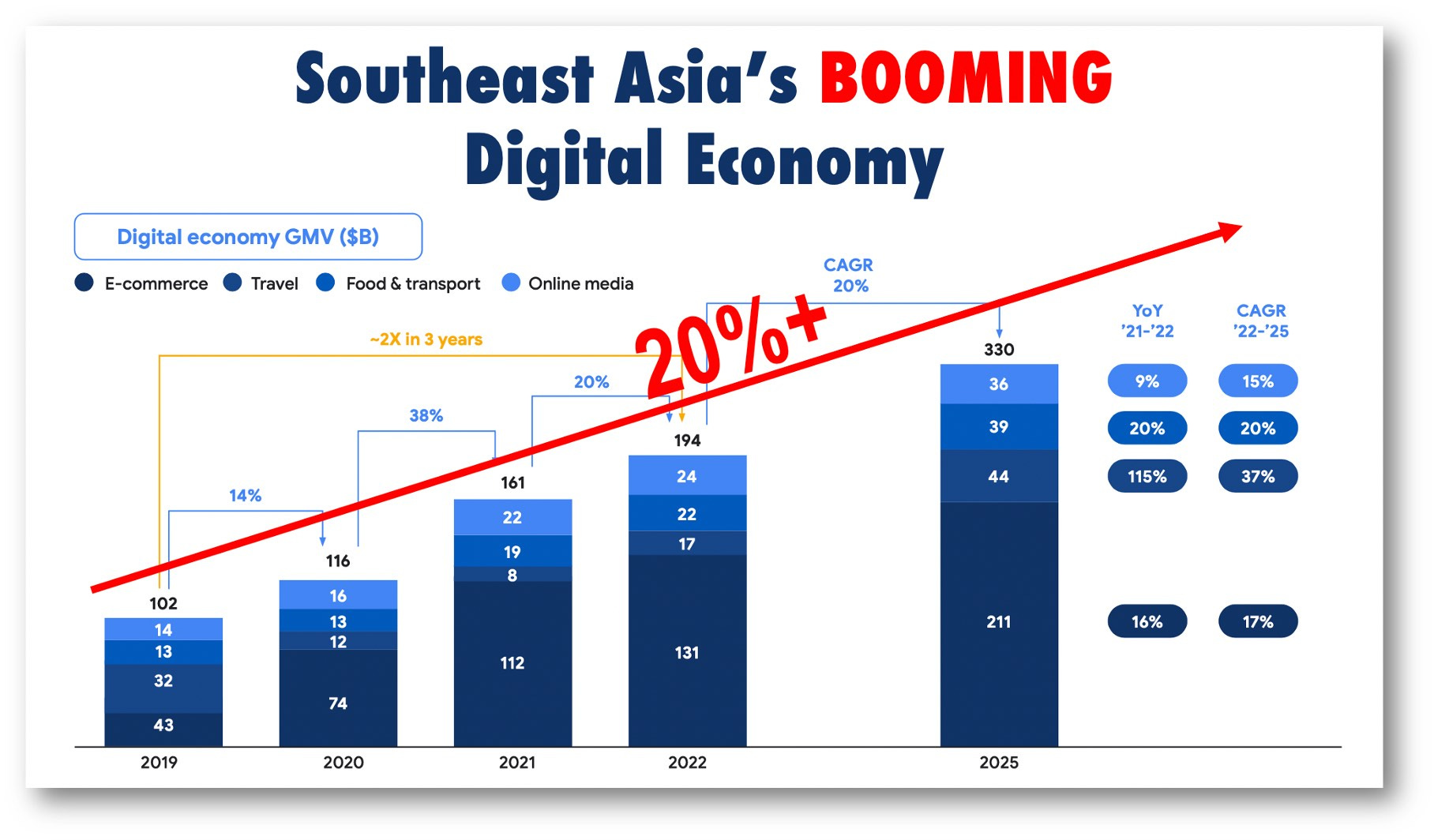

South East Asia’s “digital decade” is upon us with digital payments hitting $2tn by 2030 and the digital economy growing by 2x GDP!

Watch as Southeast Asia’s digital economy heads for the moon. Never forget that digital in SEA is seen as aspirational!

Download: here

For years now I’ve been telling you all that SEA’s digital economy is on fire! It’s not just on fire but growing faster than predicted. It is on course to reach $200b in gross merchandise volume this year a full three years earlier than predicted by this same report in 2016!

This report by Google, TEMASEK, and Bain does a great job of laying out which countries and products are taking SEA by storm. The leading products are e-commerce, groceries, food delivery, transport, travel, online media, and gaming!

While the report goes into depth into all of these sectors lets focus on the sectors in digital financial services that are making it big:

🔹 Pure-play fintechs:

Largely focused on expansion to improve profitability and drive customer stickiness. Their biggest challenge however remains profitability with limited offerings despite their digital prowess.

🔹 Established financial services players:

Rapid digitalisation to unlock seamless omnichannel customer journeys and to compete with insurgents. Digitally challenged incumbents have products unlike their fintech competitors but lack the digital skills to bring them to market.

🔹 Consumer tech platforms:

Leading e-commerce or transport platforms expanding into DFS with an initial focus on existing customers. These could be the superapps of tomorrow but their limited product offerings hold them back.

🔹 Established consumer players:

Solo attempts at expansion were mostly unsuccessful and now pivoting from individual ventures to partnerships. They have great client relations but lack digital capabilities.

🔹 Digital banks:

New entrants leveraging existing merchant and consumer networks to reach unbanked and underbanked populations. This is the sector that everyone is focusing on! Their cost base is some 60-70% less than incumbents, yet without credit, they are struggling for profitability.

Sticking with digital banks, the report brings in something new with the concept of digital banks' “right to win” business being directly proportional to the unbanked population (pg 43).

Using the “right to win” Bain picks Indonesia, the Philippines, and Vietnam as the leading nations for digital banks. Thailand and Malaysia are in the middle and mature Singapore with a low unbanked population as a non-starter.

This is the market that CBDCs will eventually enter, with all of the SEA nations in the report building them. My take is that CBDCs will be broadly welcomed because as we are seeing in this report digital services are on fire.

Takeaways

SEA’s digital economy is growing in leaps and bounds! But ask yourself why? Yes digital services fill critical gaps, but there is more to it……

Digital services in SEA are seen as “aspirational” for many. They bring products and services that were unavailable and are seen as a way to a better life.

Fintechs are having a field day in SEA due to the large unbanked population.

Watch as SEA mobile payment companies build out their cross-border transfer systems to create a new payment paradigm that excludes Visa and Mastercard. Not if, but when!

5. China’s Economic Slowdown

Let’s talk China, even with a slowdown, chip-wars, and covid “the sky is not falling” and long-term growth should not be ignored.

Hey if you want to help me out, and read a great article on China click HERE!

There is no paywall on CFO.com and every view ensures that I get invited back!

Thank you to Adam Zaki for interviewing me for this CFO.com article! We talked about what's going on in China and the article serves as a great update across multiple sectors. I encourage you to read it.

I pull no punches

I don’t pull punches on Evergrande and some of the gross mismanagement in China but it’s also important to see that the predictions of imminent doom in China are misplaced.

As if on cue, we have UBS chair Colm Kelleher backing me up on this point this week saying that “Global Bankers are very pro-China.” This gem says it all: “We’re not reading the American press, we actually buy the [China] story.”

Adam did a fabulous job with this interview please check it out! HERE

Subscribing is the logical thing to do!

My work is entirely supported by reader gratitude, so if you enjoyed this newsletter, please consider subscribing or sharing it, and follow me on Twitter, or Linkedin. If you want to learn more about Innovation Labs or China’s CBDC, check out my website richturrin.com which is full of videos, interviews, and articles. The best way to make sure you see the stuff I publish is to subscribe to the mailing list here on Substack, which will get you an email notification for everything I post.

Everyone, including platforms that disagree with me, has my permission to republish, use or translate any part of this work (or anything else I’ve written outside of my books) with credit given to me and this site (richturrin.substack.com) free of charge. For more info on who I am, what I do, and where I’m going, check out richturrin.com

Rich Turrin is the international best-selling author of "Cashless - China's Digital Currency Revolution" and "Innovation Lab Excellence." He is number 4 on Onalytica's prestigious Top 50 Fintech Influencer list and an award-winning executive previously heading fintech teams at IBM following a twenty-year career in investment banking. Living in Shanghai for the last decade, Rich experienced China going cashless first-hand. Rich is an independent consultant whose views on China's astounding fintech developments are widely sought by international media and private clients.

Please check out my books on Amazon:

Cashless: (https://amzn.to/3RcC6PB)

Innovation Lab Excellence: (https://amzn.to/3C35Mcr)