Payment Risks Drive Growth, Tell That to PayTM!

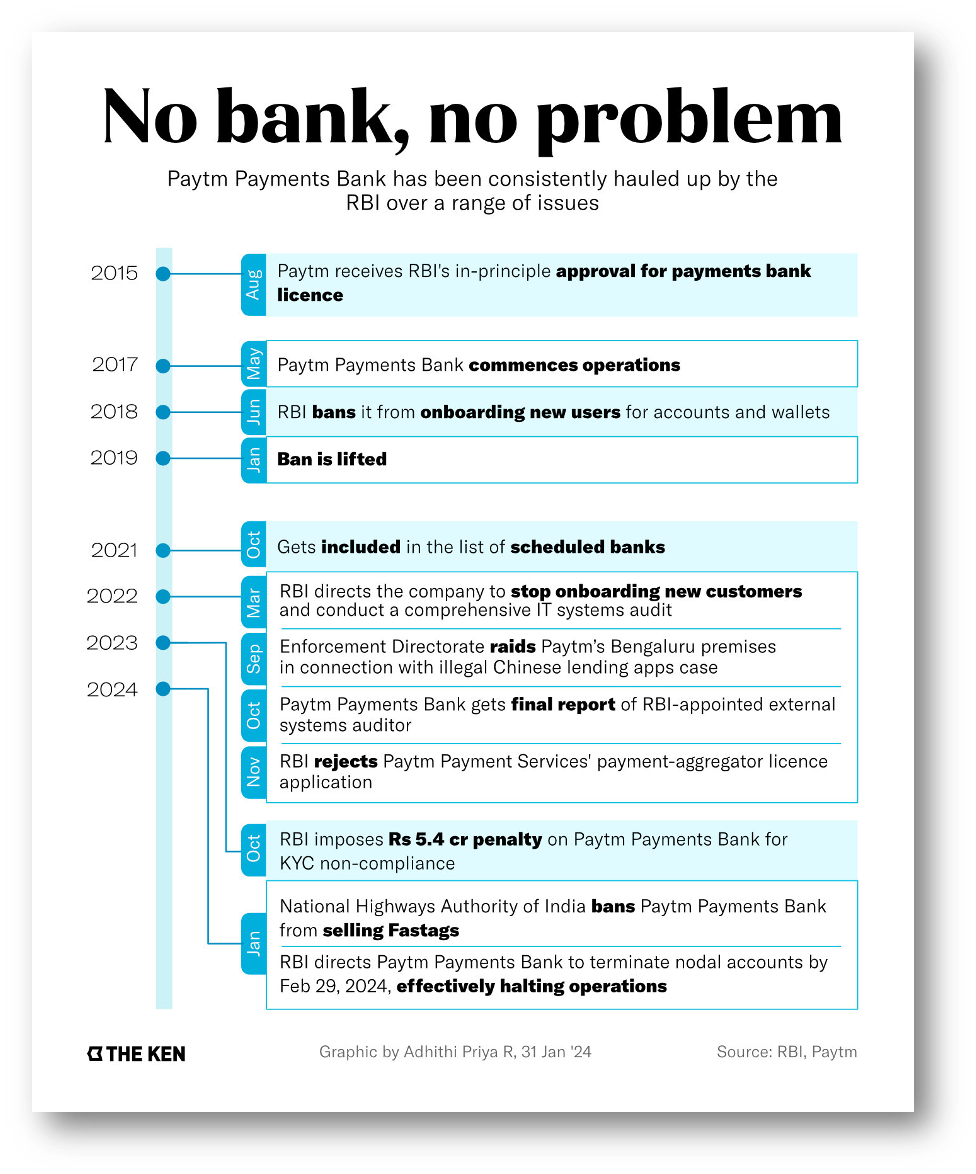

PayTM regularly flaunted regulator's concerns and died by its own sword.

Never have the stars aligned more perfectly for a McKinsey report on managing payment risks because PayTM is a perfect example of how NOT to do this!

For those who may not know, India’s famous payment fintech PayTM has been banned from accepting new credit card transactions, and digital wallets are in runoff mode, effectively shutting down the company’s payments.

India shutting down one of its most famous fintechs is a real shocker! However, Paytm’s pervasive history of regulatory non-compliance shows that McKinsey is right in telling payment companies to manage risk!

👉TAKEAWAYS: Risk as a mechanism for protection

1. Strengthening risk processes to maintain regulatory compliance

In addition to increasing the focus on fraud mitigation, payments service providers (PSPs) could be looking to modify their risk management programs to protect their revenue and improve regulatory compliance.

PayTM FAILURE: PayTM failed to apply adequate KYC on client accounts despite multiple regulatory interventions. Instead of strengthening risk procedures they appeared to flaunt them to speed growth!

2. Fighting fraud while enhancing the customer experience

The incidence of fraud and scams, such as account takeover (ATO) and authorized push payment, or APP (when someone is tricked into sending money to a fraudster), are growing at alarming rates.

PayTM FAILURE: By ignoring regulators’ concerns, PayTM was complicit in scams by allowing single personal IDs to control multiple accounts, which opened the door for tax evasion and fraud.

3. Building operational resilience to prevent failures

In 2024, new rules and regulations could accelerate PSP action on operational resilience.

PayTM FAILURE: This is the part that PayTM seemed to willingly ignore. PayTM seemed to be betting regulators would have infinite patience with their transgressions and didn’t count on STRICTER enforcement that is hitting payments globally.

4. Improving credit and collections processes to address a new normality

During COVID-19, issuers and wallets reported low delinquencies, partly because of excess cash in cardholders’ accounts that was associated with delayed spending, relief funds, and low interest rates.

PayTM FAILURE: PayTM was not a lender but had lending partners. Partner lending could be compromised if multiple accounts are tied to a single ID.

PayTM ran up a long record of regulatory non-compliance that taxed regulators to the limit. Source: The Ken @TheKenWeb on X.

👊STRAIGHT TALK👊

Payment companies manage your risk if you want to survive and PayTM shows what NOT to do!

McKinsey’s report on Payments and Risk shows how a risk program is the foundation for growth. It is a sound report and would seem unsurprising were it not for Paytm’s failure to point out how important risk management in payment is.

All payment companies are under increasing observation by regulators, and any form of “payment-made-easy,” regardless of its technological underpinnings, should expect to be under the microscope.

This shouldn’t come as a surprise. With billions of VC money dumped into payments in recent years, India’s regulatory action is likely only the first of many to come and is likely the “new normal,” not a statistical outlier.

Think that this is just India or Asia? If PayTM is the best example, Revolut in the UK will come in second for showing how NOT to manage risk and impress regulators.

Thoughts?

If you’ve read this far, there had to be something that made you stick around to the end! So do yourself a favor and subscribe, it’s free!

What do you have to lose? If you don’t like my newsletter, just unsubscribe.

The button says pledge, but there’s no need. Substack adds that it's not me.

Share