Stablecoin Yield: Crypto Exchange Disclosures Are Nearly Criminal

Exchanges have quietly redefined "earn" and "principal protection"

I post daily, but deliver to your inbox every Sunday. Browse past newsletters HERE. Book Rich. Bring the speed of Asia to your next event HERE

Read me first

Banks hate stablecoin yields, and exchanges love them. The Clarity Act will decide who wins, but what Coinbase calls "earn" and "principal protection" is nearly criminal.

BIS research lays bare what exchanges call “earn,” and what I uncovered about “principal protection” is equally damning. Neither will make you love crypto exchanges.

A new BIS Bulletin shows that stablecoin yields on centralized exchanges come from two entirely different places, carrying two entirely different risk profiles, hiding under the same “earn” label:

Coinbase/USDC: a passthrough of reserve asset income, Treasury bills and repo instruments, tracking the federal funds rate. Stable, predictable, resembling a money market fund without the regulatory wrapper.

Binance/USDT and USDC: yield drawn from the exchange’s own lending, margin finance, and trading activity. Binance’s own Simple Earn terms state that customer assets are commingled and may be used for loans to other clients at Binance’s “sole discretion.” Coinbase runs a similar product.

The Binance yield, or similar Coinbase product, is not a savings product. It is a revenue share from a trading floor, with your principal on the table marketed as “earn.”

Same word, but an apples-and-oranges comparison with your bank.

Consumers should have the right to pick what they are comfortable with, but that requires knowing what they are actually picking. Right now, the labels make that nearly impossible.

“Principal Protected”

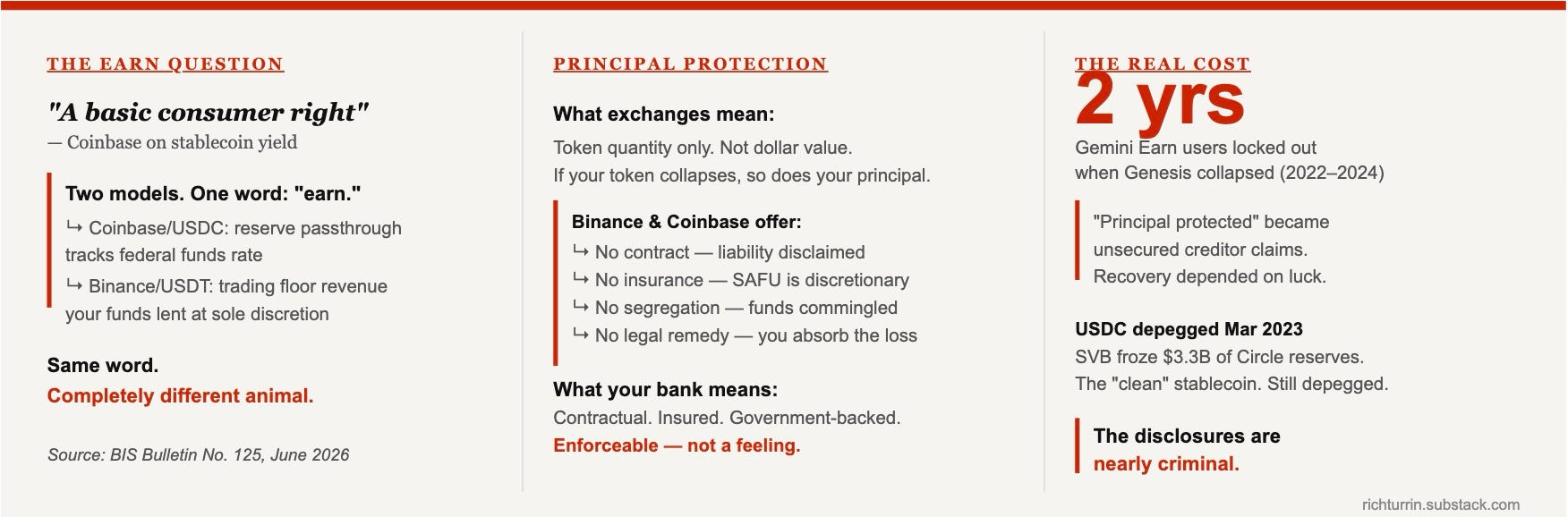

So, adding to the confusion we saw with earn, Coinbase and Binance compound the problem with another borrowed term: “principal protected.” A term that any bank customer reads as a guarantee.

Both Coinbase and Binance call their Simple Earn products “principal protected,” but have a new definition for protection.

For these exchanges, principal protection means the token quantity is protected, not the dollar value. So if your token value collapses, so does your principal. That redefinition is nearly criminal.

This notion of protected says nothing about exchange solvency, nothing about the peg, and nothing about what happens if the trading book generating your yield blows up.

Compare that to what principal protection means in traditional finance: a contractual obligation, deposit insurance, and a legal remedy if delivery fails. An enforceable guarantee backed by government balance sheets.

Binance and Coinbase’s version:

↳ No contract: terms explicitly disclaim liability for platform failure

↳ No insurance: Binance’s Secure Asset Fund for Users (SAFU) is a discretionary reserve with no defined per-user coverage. Coinbase has no equivalent reserve at all.

↳ No segregation: the BIS flags that customer stablecoins may be used for the exchange’s own activities, unlike traditional intermediaries which fully segregate client funds

↳ No legal remedy: if the peg breaks or the platform fails, you absorb the loss

This isn’t a theoretical discussion. Gemini Earn users discovered this the hard way. When Genesis collapsed, their “principal protected” holdings became unsecured creditor claims in a bankruptcy proceeding.

Withdrawals were frozen for nearly two years with no insurance, no legal remedy, and no queue jump. Users did get their crypto back, but only because Bitcoin tripled during the bankruptcy period. If prices had moved the other way, the story would have ended very differently.

Counterparty risk, as with Gemini, is only part of the problem. The stablecoin peg itself holds only if reserves hold, regulators don’t intervene, and market confidence doesn’t crack overnight. USDC briefly depegged in March 2023 when Silicon Valley Bank froze $3.3 billion of Circle’s reserves. That was the clean, GENIUS Act-compatible stablecoin, and it still depegged.

Two things the consumer rights debate is not telling you.

First, when Brian Armstrong calls yield a consumer right, he is also describing a revenue model that pays Coinbase handsomely for stablecoin adoption. Coinbase earns roughly 40% of reserve income generated by USDC held on other platforms, with Circle taking the other 40%. The more USDC in use the more Coinbase makes.

Second, activity-based yields like Binance’s, which depend on crypto lending, surge when crypto markets run hot and collapse when they cool. Consumers get caught when the market goes bust, not just with no yield but potential loss of capital. The BIS warns that busts are accompanied by rapid shifts back to fiat, putting redemption pressure on the assets backing the stablecoin.

When treasury markets sell off, the chain runs from stablecoin redemptions straight to the Fed, banks, and unrelated investors. A stablecoin run does not stay in crypto.

The debate over deposit interest between banks and exchanges is comparing apples and oranges. Consumers have the right to yield. They also have the right to know what they are actually buying.

Crypto exchanges are failing them on both counts, and their disclosures are nearly criminal.

HAND CURATED FOR YOU

🚀 Asia moves fast. So does this newsletter. I curate only the best fintech, CBDC, and AI insights from 50+ sources weekly so you stay ahead of what’s coming West. Subscribe and never fall behind.

If you know someone who would like this newsletter, please share it with them and help grow our Asia, CBDC, and AI aficionados community!