Stablecoins: The New Digital Dollar with a $3.7 tn Market Potential

This is my daily post. I write daily but send my newsletter to your email only on Sundays. Go HERE to see my past newsletters.

HAND CURATED FOR YOU

In the most important read of your month, Citi examines the new digital dollar, and it isn’t a central bank digital currency (CBDC), but rather stablecoins run on blockchain.

There is only one reason why we are at this “ChatGPT moment” for stablecoins, and that is that the Trump Administration is pushing them as the new digital dollar, and bringing regulatory clarity, through the forthcoming GENIUS Act, which will legitimize some, but not all, dollar-based stablecoins.

This is a profound moment, as the dollar is going digital without a CBDC, as used in Europe, China, and 94% of central banks around the world researching them.

Make no doubt about it, the US chose this path because CBDCs were politicized during the last election, and unfairly portrayed as causing the end of freedom in America.

I will go on record as confirming that I do like stablecoins, but I find them inferior to CBDCs in many ways. But one above all concerns me.

The primary concern is that stablecoins fail to maintain the “singleness” of the US dollar. Singleness means all dollars are interchangeable (fungible) with one another. Meaning my dollar is worth the same as yours.

Stablecoins embed the risk of the issuer just as “wildcat” banks did in the US between 1835 and 1865, when individual banks issued dollars, many of which collapsed.

I don’t mean to imply that stablecoin issuers will collapse like wildcat banks given prudent regulation. However, the risk of depegging, where the stablecoin cannot be exchanged 1 for 1 with dollars, is real and a problem that Citibank doesn’t have an answer for and is uncharacteristically silent on.

These depegs are a real concern and not as rare as advertised. Citibank admits that Stablecoins de-pegged approximately 1,900 times in 2023, with around 600 of these instances involving large-cap stablecoins. So why does “depeg” only appear once in the report?

Depegging is something a CBDC cannot do, as the central bank issues it, and it is considered “risk-free.”

Fortunately, fintechs like Ubyx do have answers to depegging with issuer-funded reserves designed to protect users, but this is new territory, and transfer mechanisms like Ubyx need to be tested and then implemented for stablecoins to go mainstream.

Whether stablecoins are a better means of attaining a digital dollar than CBDC, only time will tell. My feeling is that they introduce complexity through intermediaries that a CBDC will not need. For stablecoins to be suitable for mass adoption, they need to rely on fintechs like Ubyx and others to build the necessary critical infrastructure.

Another potential issue is that we must carefully monitor the risk of new duopolies emerging in the stablecoin world, similar to Visa and Mastercard, and that stablecoins do not create “walled gardens” that restrict the free exchange of stablecoins.

Will this increase the use of the US dollar, as Washington claims?

This is unlikely because stablecoins will be subject to the same sanctions, AML, and KYC as any other bank transaction. While stablecoins may have advantages in cost and speed, that doesn’t mean more trades will be done in dollars so much as stablecoins will cannibalize other payment systems.

Another important factor conspiring against increased dollar use is the global trend toward de-dollarization, which the trade war has significantly amplified. Using a stablecoin dollar does not alleviate sanctions and other restrictions on dollar usage. While stablecoins may attract new dollar users, the dollar already holds the majority of the market, raising the question of how many more dollars the world can absorb.

In the meantime, we should all look forward to and welcome stablecoins in their new role as digital dollars. This is, without question, a positive development for all consumers.

👉Key Takeaways

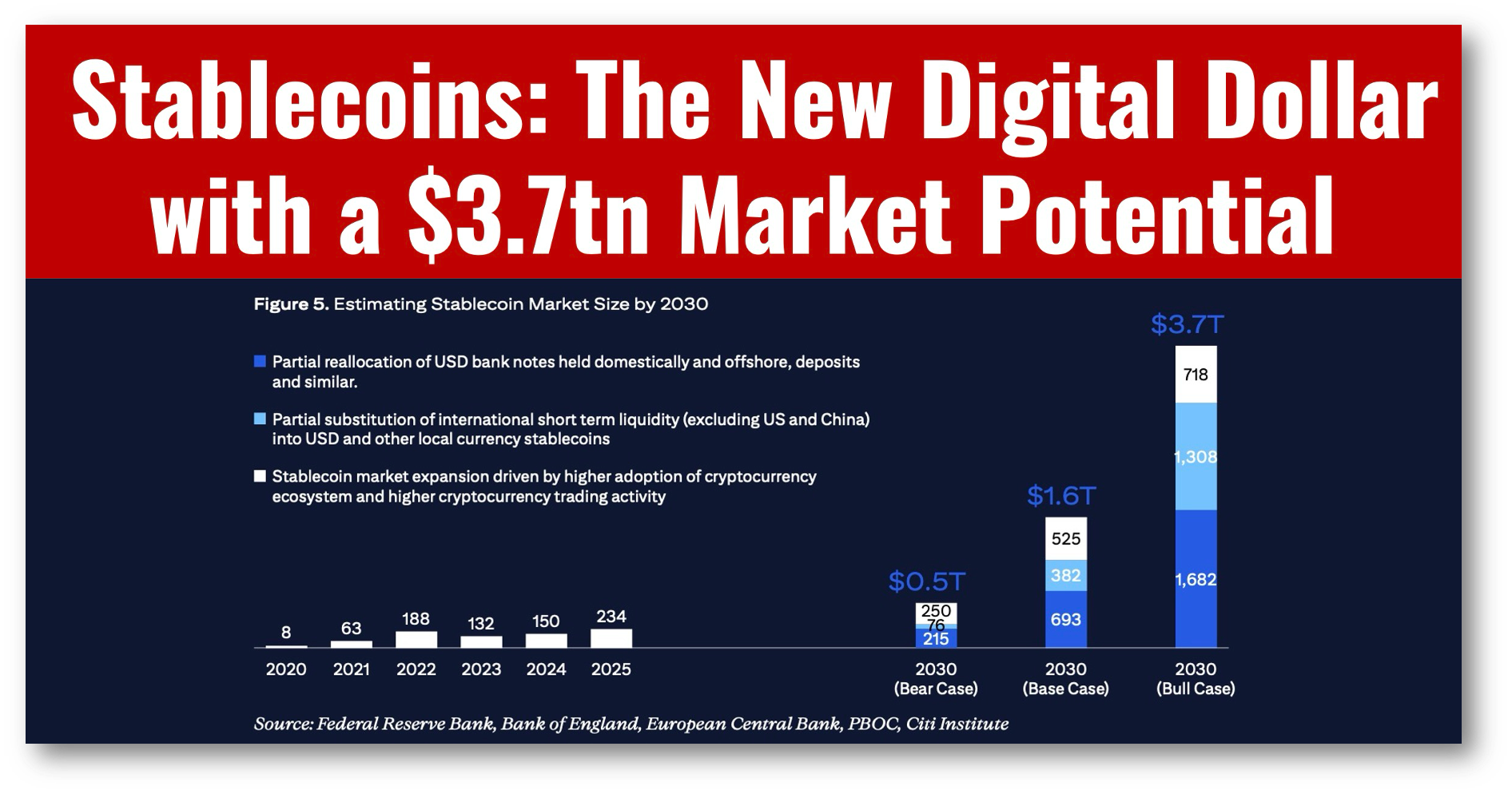

🔹 The total outstanding supply of stablecoins could grow to $1.6 trillion by 2030 in our base case and to $3.7 trillion in our bull case. That said, the number could be closer to half a trillion dollars if adoption and integration challenges persist.

🔹 We expect the stablecoin supply will remain US dollar-denominated (approx. 90%, with non-US countries promoting national currency CBDCs.

🔹 A US regulatory framework for stablecoin could drive net new demand for US Treasuries, making stablecoin issuers among the biggest holders of US Treasuries by 2030.

🔹 Stablecoins pose some threat to traditional banking ecosystems via deposit substitution. But they are likely to offer banks/financial institutions opportunities for new services.

🔹 Key public sector use-cases of blockchain include: tracking spending, disbursement of subsidies, public records management, humanitarian aid campaigns, tokenization of assets, and digital identity.

(Note that the tracking feature is touted as a benefit! Amusingly, it bears a resemblance to the most severe accusations of government surveillance associated with CBDCs. )

If you know someone who would like this newsletter, please share it with them and help grow our Asia, CBDC, and AI aficionados community!