The Circus! Fast payments💨 EU fintech🥇 Embedded Finance💰MBridge is a CB⚡️DC Rockstar🤘🏼

Biden's AI EO is a big step forward

1. Fast payments are no longer optional

2. European fintech market beats US?

3. Embedded finance: who does what and transparency

4. MBridge is a CB⚡️DC Rockstar🤘🏼

5. Bidens AI new EO is a big step forward

Today’s artwork: Henri Matisse, Circus (Le Cirque) from Jazz, 1947

In the final decades of his life, Matisse invented a new form of art, the cut-out. Working with scissors and sheets of gouache-painted paper, he cut various shapes—from the organic to the geometric—and arranged them into lively compositions. Cut-outs formed the prototypes for the printed images in the illustrated book Jazz.

Despite its musical title—likely named for the experimental, improvisational nature of its compositions—the book’s dominant themes are the circus and theater. The “experimental and improvisational” and the idea of a circus perfectly fit our current fintech world and today’s stories!

1. Fast payments are no longer optional

Faster Payment Systems and no longer an option but a necessity. See why!

The World Bank looks at Faster Payment Systems (FPS) and shows how they improve convenience, speed, and cost of payments.

That's good, but what makes them a necessity is that they allow financial services to innovate and add new services!

FPSs are in banks' best interest!

Think CBDC will kill FPSs? Read 👊STRAIGHT TALK👊 in the comments below to see why that won’t happen.

👉TAKEAWAYS:

• The global real-time payment market is expected to grow at a compound annual growth rate of 35.5% from 2023 to 2030.

• The Asia-Pacific Region has dominated the FPS market, with a share of 38% in 2020.

• Initially, most FPSs were launched to support real-time and around-the-clock domestic P2P fund transfers.

• Use cases have expanded drastically in recent years due to technological progress, changing expectations, and increased adoption of fast payments by end-users.

• Increased standardization in payment messaging across global markets enables interoperability and allows users to transfer funds across borders in close to real-time.

• Interoperability between payment providers, both domestically and across different jurisdictions, is expected to grow multifold.

• Retail payment trends such as digital lending and deferred payments (BNPL) allow payment schemes, financial institutions, and overlay services to monetize FPS through new services.

• FPS is also behind banks’ heavy investment in open banking to provide more efficient and transparent services in banking.

• CBDCs may impact FPS systems, though integration is a more likely scenario. (Note India’s CBDC integration with UPI.)

👊STRAIGHT TALK👊

I don’t know if you’ve noticed, but it seems like every week, there is a report on Fast Payment Systems and how they are now mandatory!

I think that’s great for consumers and merchants who deserve the convenience and low fees FPS systems bring.

The big question is how will FPS and CBDC interact? Some claim that CBDC renders FPS systems redundant.

A more likely scenario is that FPS systems can be used as the payment rails for CBDC.

India and China both provide examples of how this works. In India’s CBDC trials, the e-rupee can also use the existing UPI network.

China followed a similar path, building the digital yuan into both WeChat and Alipay superapps.

Rather than one system “killing off” the other, they will all coexist in a symbiotic relationship where they help each other.

CBDC gets to ride on the back of established digital payment rails, while in return, the FPS systems get a higher volume of payments over their network.

Remember that people paid in CBDC will spend more digitally than ever before. FPS networks want to capture this increase!

So it’s not a question of FPS or CBDC but both!

2. European fintech market beats US?

Despite getting hammered by the tech and start-up sector downturns, the EU’s fintech isn’t going anywhere and has made some impressive gains.

In fact, it is holding its own, even beating the US!

Still, the gap between the EU’s advanced fintech nations, such as Sweden and the UK, and laggards is shocking.

👉TAKEAWAYS:

🔷 In each of the seven largest European economies, at least one fintech ranks among the five top banking institutions.

🔷 By the end of 2021, Sweden and the United Kingdom were the leading fintech ecosystems for funding per capita.

🔷 There is growing fintech activity in every EU country, including unexpected pockets of strength in a few small economies such as Estonia, Luxembourg, and Malta.

🔷 There is a wide divergence of maturity and performance among fintech ecosystems by country, with substantial gaps between the top one-third and the rest.

🔷 The bottom third contains: Italy, Hungary, Slovenia, Czech, Croation, Poland, Greece, Bulugaria, Romania Slovakia.

🔷 For comparison, in 2021, the US would ranked in the top one-third of Europe,

🔷🔥The US was beaten on overall score by the UK! 🔥 (Let’s not mention that the UK is no longer Europe.)

🔷 To scale up, fintechs in Europe need to be able to expand beyond their home market.

🔷 McKinsey pushes a regulatory-heavy set of solutions to foster fintech in the EU. They are believable but their best recommendation is to increase more “homegrown” capital.

👊STRAIGHT TALK👊

EU fintech is doing a great job and by the numbers, is helping to modernize the financial system. This is good for all citizens.

Still, while the top fintech nations are models for innovation, the bottom third of Mckinsey’s three-part classification aren’t just laggards but woefully behind.

McKinsey, ever the optimist, sees this as an opportunity. When fintech works its magic in these countries, it will bring large gains. McKinsey has grounds for optimism because these untapped markets still have room for growth.

Still, I’m unsure if McKinsey’s metrics accurately capture the situation in the EU.

I was surprised to see Italy in the bottom third in terms of “fintech per capita” and “funding per capital”!

While I agree that Italy does not belong among the leaders, seeing it in the bottom five doesn’t quite square with the digital banks and payment systems I saw this summer.

So, while I celebrate the EU’s impressive fintech gains, the I have to ask if this report is measuring the right thing?

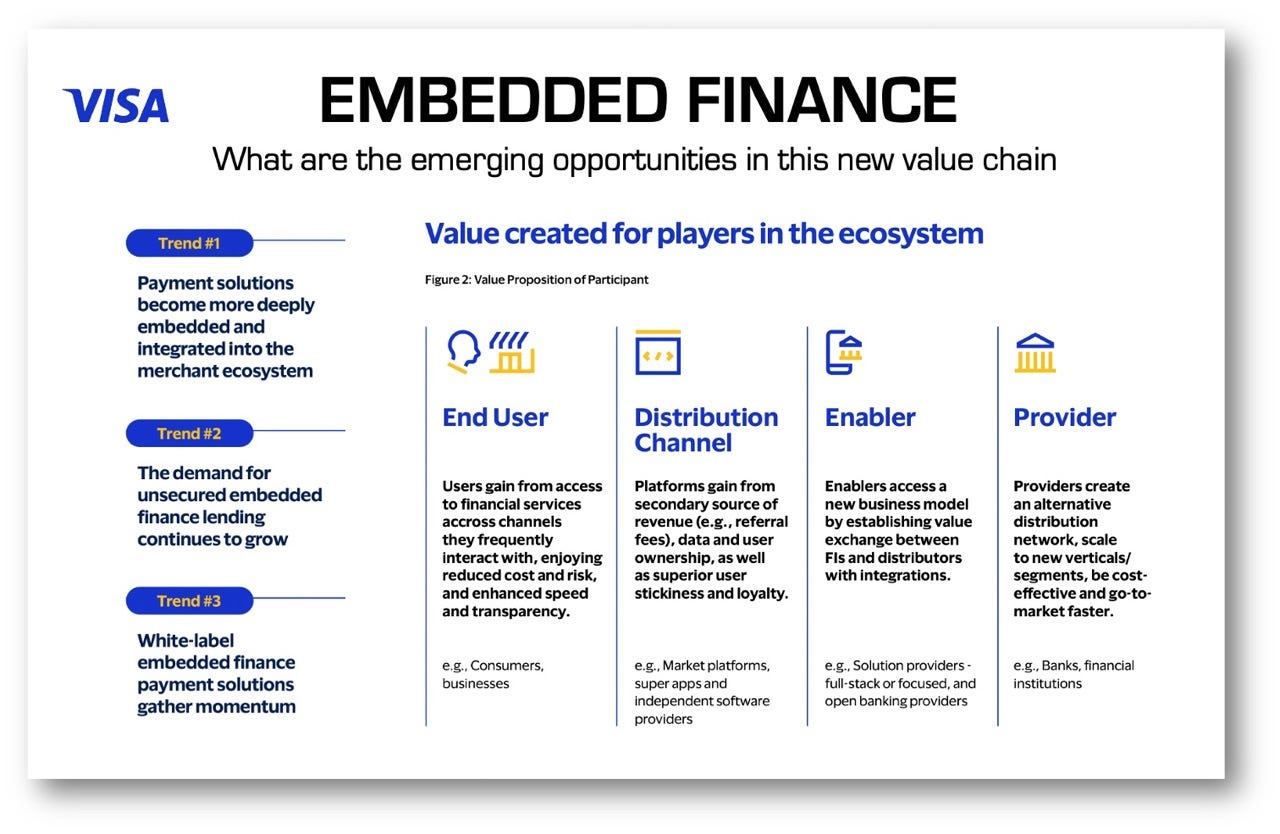

3. Embedded finance: who does what and transparency

Visa loves embedded finance and sees growth for financial services and digital players, but how transparent is it for consumers?

Visa produced this solid report on embedded finance that does a great job of clarifying the players and exactly who does what!

If you didn’t “get” embedded finance before, you will now.

But how transparent is it? See 👊STRAIGHT TALK👊 for the answer.

👉TAKEAWAYS:

🔷 Player 1: THE PROVIDER

The provider is a regulated financial institution that holds a license to provide financial services. It provides financial products.

🔷 Player 2: THE DISTRIBUTOR

The distributor is a non-financial distribution channel and provides the interface from which the financial products are offered to end users.

• Platform examples: Super apps that offer wealth management and personal financial management solutions – by partnering with specialist players.

•Independent Software Vendors (ISVs): ISVs offer niche solutions to meet the unique needs of a given industry, such as invoicing, expense tracking, managing cash flows, and customizing invoices.

🔷 Player #3: THE ENABLER

The enabler is the middle layer that integrates across providers and offers a one-stop shop to distributors.

•Full-stack enablers offer banking as a service (BaaS), which enables businesses to build their financial products on the enabler’s banking platform.

•Focused enablers service SMBs and corporations by offering a focused banking offer like payments.

•Open banking enablers offer data integration solutions.

👊STRAIGHT TALK👊

Visa sees a bright future in embedding.

It couldn’t be any more clear what’s in it for Visa: the more embedding, the more money gets carried on Visa’s network.

There’s nothing wrong with that except for Visa’s high charges. Let’s leave them aside for now.

Embedding is, in theory, good for the consumer because it will give you better access to financial services across channels.

In an ideal world, this will mean reduced cost, risk, enhanced speed, and transparency.

The problem is that we all know the world is far from ideal.

We still don’t know whether banks and platforms will provide transparency and choice for consumers with embedding.

So far with BNPL, the hero of early ventures into embedding, the results are not convincing.

In most cases, embedded BNPL fails to offer:

•Options to use other BNPL providers

•Cost comparisons with other financing options

•An analysis of what BNPL will cost if you miss a payment

So, while everyone from Apple to Klarna is pushing embedding, where exactly is the “transparency?”

Most users don’t know if they are getting a good deal, but that big button that promises instant gratification is irresistible!

And that’s the problem!

4. MBridge is a CB⚡️DC Rockstar🤘🏼

MBridge is a “CB⚡️DC Rockstar🤘🏼” and will go on a world tour with 23 central banks, IMF and World Bank!

MBridge’s cross-border CBDC transfers will change the world; don’t say I didn’t warn you!

👉TAKEAWAYS:

🔷 Project mBridge in Hong Kong is a multi-CBDC common platform for wholesale cross-border payments focusing on international trade.

🔷 MBridge connects central banks and commercial banks around the world as a "public good."

🔷 mBridge will go live with a minimum viable project in mid-2024!

🔷 There are now 23 central banks observing the project, plus the IMF and the World Bank

🔷 11 of the 23 central banks have transacted in a sandbox environment

🔷 This system will put an end to correspondent banking and is an alternative to SWIFT

🔷 Instant peer-to-peer and atomic cross-border payments and FX transactions using wholesale CBDCs will become a reality. ….and wait for it…..

🔷 ….even those without a domestic CBDC system may join the mBridge platform!

🔷 mBridge has an Asia and Mid-East focus and is an example of how fintech and geopolitics are linked. mBridge will support currency multipolarity.

Kudos to all of my friends at the BIS Innovation Hub in Hong Kong for your INCREDIBLE work!

👊STRAIGHT TALK👊

mBridge will go live with a minimum viable product in mid-2024, fundamentally changing how we transfer money across borders.

What makes mBridge special is that it allows for interoperability between CBDCs over a secure, private blockchain network.

Because CBDCs are all “custom builds,” they are not interoperable. mBridge allows them to communicate and transfer across borders using its blockchain.

Two features make this platform particularly interesting.

First is that technically, a nation doesn’t need a CBDC to interact on the platform; any real-time gross settlement platform will do.

Second, is that sanctions are imposed by the user not the platform. If country X has sanctions or restrictions on Y and Z, it is X’s responsibility to program its node on the platform accordingly. This is not like SWIFT, where SWIFT applies sanctions.

Also of interest is that the blockchain protocol used on mBridge is “Made in China.” The Dashing blockchain is considered a blockchain breakthrough in solving the blockchain trilemma. It should be no surprise that mBridge is using it!

Six of mBridges supporting central banks are from Asia and five from the Middle East.

Where do you think this is headed?

5. Regulating AI—“the most consequential technology of our time.”

Biden's Executive Order on AI is a big step forward!

Two downloads: The “FACT SHEET” The full Executive Order:

Subscribing is 100% free, you’ll be glad you did!

I’m reading your mind. In the unlikely event you don’t like my newsletter, click unsubscribe at any time! It’s only logical.

My work is entirely supported by reader gratitude, so if you enjoyed this newsletter, please do both of us a favor and subscribe or share it with someone. You can also follow me on Twitter or Linkedin for more. For more about what I do and my media appearances, check out richturrin.com

Rich Turrin is the international best-selling author of "Cashless - China's Digital Currency Revolution" and "Innovation Lab Excellence." He is number 4 on Onalytica's prestigious Top 50 Fintech Influencer list and an award-winning executive previously heading fintech teams at IBM following a twenty-year career in investment banking. Living in Shanghai for the last decade, Rich experienced China going cashless first-hand. Rich is an independent consultant whose views on China's astounding fintech developments are widely sought by international media and private clients.

Please check out my books on Amazon:

Cashless: HERE

Innovation Lab Excellence: HERE