Three big CBDC stories! Is crypto rockstar David Chaum's eCash 2.0 the future of CBDC? Digital euro progress, and shocker the Fed gushes support for wCBDC! Digital banks takeoff in Southeast Asia!

Three big CBDC stories! Is crypto rockstar David Chaum's eCash 2.0 the future of CBDC? Digital euro progress, and shocker the Fed gushes support for wCBDC! Digital banks takeoff in Southeast Asia!

QR Codes Past Present and Future! Video and podcast!

1. Digital Euro progress report

2. Is crypto rockstar David Chaum’s eCash 2.0 the future of CBDC?

3. The Fed gushes support for wholesale CBDC

4. Southeast Asia Digital banks ready for takeoff

5. QR Codes Past, Present and Future (video and podcast)

Green Wheat Fields, Auvers, Vincent van Gogh,1890 In the spirit of my immersing myself in hiking in tea fields, the green of van Gogh seemed to fit even if from a world away.

1. Digital Euro progress report

Digital euro update that has it all the Good, the Bad, and the Ugly!

Download the ECB powerpoint presentation: here

Catchy title aside, the digital euro is making GREAT progress, but there is always room for improvement! Let’s dive in using Red, Yellow, and Red for the “good, bad and ugly!”

🟩 The Good

• Christine Lagarde will “soon” go to the European Commission with a legislative proposal for establishing a digital Euro. This is great news as the EU legislators have an important role to play. The ECB has made progress in exploring and defining the rationale, risks, and rewards for the digital euro and now it’s time to get it built into the law.

• Look at page 8 in the PDF which covers the use cases for the new CBDC and you’ll see something that makes me very happy! One of the use cases that the ECB envisions is “machine-initiated” payments! “A fully automated payment initiated by a device and/or software based on predetermined conditions.” I always say that CBDCs are for a future, “when machines pay!”

🟨 The Bad

• The ECB lays out the case for offline payments on pg 9-10. This is good, but they are still not committing 100% to an offline version.

• Offline use is critical for inclusion and broad adoption. The ECB is on the right track when they say that offline transactions will have, “fully private offline transactions and holdings, no transparency to intermediary or central bank, but only for payments of lower value”

• The ECB clearly gets what the people want and need but hasn’t committed to the functionality just yet. Whether they are having tech issues or are scared of low-value private payments is hard to know!

🟥 The UGLY

• For the ugly we’ve got a quote from Fabio Panetta in a separate speech when discussing how excessive digital euro use would be “avoided by design” (pg 11)

• The concept of limits on maximum holdings and conversion into CBDC is fine that isn’t new. Nor is the idea of “tiered” remuneration, all good!

• The ugly is that in a speech he commented that the maximum amount of digital euro holdings would be €3,000. Sounds good. Then a limit of 1,000 transactions per month, (I don't like that but OK) and a maximum transaction value of €50! WHAT?

• Who is going to use a payment system with a maximum payment of €50!

• The German minister of finance fired back! “I wonder whether people would accept €50 as they can pay in cash hundreds and more,” adding: “We should introduce a digital euro that is really accepted by people and not only by policymakers.”

• Panetta is nuts if he thinks €50 will fly even for offline payments! China's offline payment cap is roughly €300 for comparison.

Takeaways

Overall the progress on the digital euro is quite good!

Offline use of the digital euro is a mandatory feature. It concerns me the ECB can’t quite commit to supporting it.

Panetta's comment is not official policy and I’m glad that the German finance minister pushed back! Still, it's very odd that he would have let this slip!

Overall I give the ECB an A- grade for keeping the digital euro project moving along! Commit to offline use and they’ll get an A+!

2. Is crypto rockstar David Chaum’s eCash 2.0 the future of CBDC?

BIS “Project Tourbillion” explores a PRIVATE CBDC that might strike the right balance but as always there are tradeoffs!

Download the paper: here

This is BIG! The BIS Innovation hub in Switzerland is partnering with crypto rockstar David Chaum and Swiss National Bank gov. board member Thomas Moser on eCash 2.0 which allows for privacy, scalability, and cyber resiliency.

Is it too good to be true? Let's look at privacy!

🔹 Privacy solved?

• eCash 2.0 is not a “privacy” coin like Monero. Instead, it allows complete privacy for the sender but not the recipient, meaning that regulatory checks can still be conducted.

• eCash allows a user to make payments and remain anonymous to both the merchant paid and the user’s bank. Your bank issues coins and handles KYC as do all two-tier CBDCs.

• When enrolling in the system users are given an irrevocable ability to undo the anonymity of any value withdrawn from their account thwarting theft and aiding criminal investigations.

• The system uses a “blind signature” technique, tokens are “blinded” upon withdrawal and only entered in the central database when deposited. This makes for “one-way privacy” which makes the CBDC unsuitable for criminal activities.

• The system solves a problem that is likely vexing the ECB that we discussed yesterday! It makes it impossible for users to aggregate large amounts of small-value transactions for criminal purposes.

🔺 Trade-offs:

• No offline usage! I have always said that offline use is CRITICAL for CBDCs. Sending and receiving CBDC tokens requires that they pass through central bank systems so no offline usage!

• It can't work with low-cost connected cards reducing inclusion. The solution is viewed as “software only” meaning that it cannot be ported to a connected card-like device like e-CNY uses!

The system is without question a major advance, as it is quantum-resistant, scalable with high speed, and can even be used with an “optional” blockchain network. Note the keyword “optional” when referring to blockchain! Still, all of these capabilities come at a cost. A digital euro without offline transfer is a non-starter for me and likely for many others. That said, privacy is key, and while there are other ways to achieve privacy this methodology is certainly powerful.

Takeaways:

Is this the future of CBDC? Maybe let's see what Project Tourbillion delivers before judging.

No doubt eCash 2.0 is a big advance in privacy for CBDCs, It gives users private spending and the ability to unmask transactions while giving the government the ability to monitor cash receipts.

Will it make governments and citizens happy? I honestly don’t know! Chaum is a rockstar in the crypto world and perhaps his seal of approval will be enough for crypto zealots who are CBDC's most ardent critics.

The ability of the government to observe the receipt of funds should allow for an adequate degree of supervision to ensure that criminal activities are thwarted.

The big tradeoff is that there will be no off-line usage and as I read it an inability to use low-cost hardware devices. Both are BIG!

3. The Fed gushes support for wholesale CBDC!

Project Cedar a potential breakthrough for a US wholesale CBDC or "innovation theater?" We can't say! But the Fed is actually gushing with enthusiasm for wCBDC.

LONG READ on the Fed's CBDC project! So long that I wrote this up as a separate article here on substack. Read it: here The full Project Cedar report is also available for download links in the article.

Michelle Neal, Executive Vice President and Head of Markets for the Federal Reserve Bank of New York, better start looking for a new job! Her recent comments at the Singapore FinTech Festival in Singapore represent the most positive comment yet by a Federal reserve employee about CBDCs!

….click through to read the full article: here

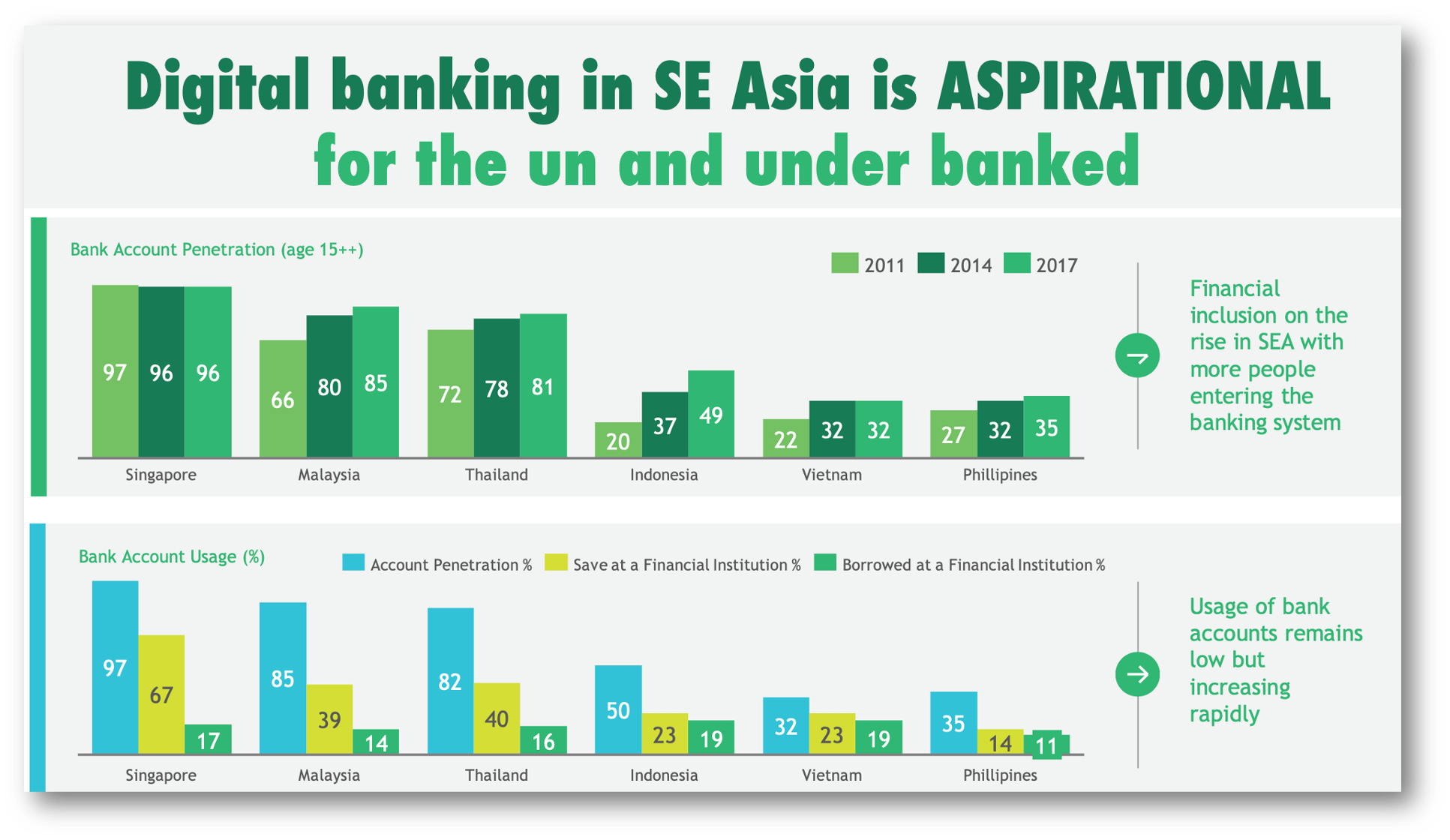

4. Southeast Asia Digital banks ready for take-off!

Southeast Asia’s digital banking is at full-throttle at the end of the runway and ready for take-off!

Just to prove that my writing is “timeless” I have to admit an error! After writing this about SEA digital banks I realized that the report from the Singapore Fintech festival that compelled me to write was from 2020 instead of 2022! So while the report is old my comments are up-to-date and "timeless!" The SEA digital bank report is available: here

The 2022 version from the Fintech Festival is not quite the same but is a great read and available here

SEA offers digital banks a combustible mixture of GDP growth combined with pent-up demand for service.

Digital banks will boom not because of technological wizardry but because the region is desperately in need of them!

Let’s not sugarcoat Southeast Asia’s banking reality, it's bad.

Let’s not sugarcoat SEA's banking reality, it's bad. More than 50% of 270m Indonesians do not have a bank account, while 68% of Vietnamese and 65% of Philippinos are unbanked. Digital banking is desperately needed and incumbents left the door open!

At the same time, ASEAN GDP will make it the 6th largest economic block in the world with 540m people. How can digital banks fail with regulators' support? Easy!

The easiest way to fail is to hold on to the myth that you can use Singapore as a springboard to SEA, something I hear all the time. This is misguided for all but the largest companies. What works in Singapore, a wealthy city-state simply won't appeal to SEA's poorer nations. If you want to succeed in SEA you must be on the ground and fully immersed in the marketplace.

Here are my thoughts on the keys to success for SEA digital challenger banks:

🔺 The report's speed to market advice is perfect!

There is an expectation in SEA that the product cycle is short. This is not the place for Apple-like product perfection, but for fast and dirty coding that goes directly to the marketplace to see what people want. Fail fast and keep pumping out products!

🔺 Leveraging fintech is key!

Challengers simply aren’t going to have all market niches filled. Without local partners, a challenger bank will find that its offerings are simply boring. Clients love you not because of your banking app, but what they can do with it!

🔺 Multi-country rollout is a lot harder than the report makes it sound!

SEA nations are very different! Any thought that a cookie-cutter approach will work here should be abandoned quickly. The authors make a grievous error in suggesting multi-country rollouts are to be expected!

🔺 Go beyond banking.

The concept that you can just be a great bank in this region is deeply flawed. That may work in developed nations but in SEA the WeChat and Alipay model dominates.

The regions unbanked are not looking to simply put their money in the bank and watch and wait. They want functionality. Maybe not super app levels, but something more!

Takeaways:

Digital banking is an aspirational product in SEA in that it's not just about a bank, but the better life it can bring.

Providing lifestyle services beyond banking isn’t optional. Always answer the question how does this help clients aspire to a better life?

SEA is going to spawn the next generation of digital banks but it won't be easy!

5. QR Codes Past, Present and Future: Podcast interview and video!

My thoughts on QR Codes: Past Present and Future with the incomparable Theodora Lau!

This was so much fun because I got to work with my friend Theo, author of “Beyond Good.” (see comments) She gets that there is far more to QR codes than meets the eye! This podcast was brought to you by the true masters of QR codes Alipay and the AntKast podcast!

Timestamp: (from video)

🔹 1:44 Tell me about yourself.

“I watched China go Cashless firsthand!" It inspired me to write "Cashless."

🔹 4:10 What is so special about QR codes?

QR is old technology that was actually considered dead! It is useful because it creates a bridge from the physical to the digital world.

🔹 7:00 The transition to QR codes how did it go?

2014 was the year Apple Pay, WeChat, and Alipay all launched! By 2017 all of China had gone “cashless” because it was so convenient. QR codes also eliminated the need for a POS device!

🔹 09:38 Theo:

“I have to laugh because I wrote a check this morning!” 🤣

🔹 10:06 Global adoption of QR.

All of Asia is QR friendly and now QR has migrated to PIX in Brazil and Mercado Libre in Latin America. It’s gone global! Even Metapay is using QR codes.

🔹 12:57 Why now for EU QR payment standardization?

Because we have a digital euro coming in about 5 years and a standardized QR code system will make for a unified EU digital payment system. One QR code and you can pick how you want to pay! This is where Alipay+ is taking the world now!

READ: “Standardizing QR Payments in Europe” Copenhagen Economics (https://bit.ly/3DS6fPp)

🔹 16:54 How can QR code be an enabler of financial inclusion?

QR codes are a perfect way to bring more vulnerable people into a digital payment world that they would be excluded from in the West! Apple Pay was “pay to play” and did not foster inclusion! Yes, that's true.

🔹 20:45 NFC vs QR codes?

The west lives in a proximity payment world, meaning you need to be close. QR codes can be used from much further away and without electricity. They are elegant!

🔹 24:40 What role will QR play in embedded finance?

The real question is what can’t you do with a QR? They are ubiquitous in China. So embedded finance? Well, where do you want to put your QR code? There is no limit! Alipay invented embedded finance, but the West will have to wait.

🔹 28:20 Theo’s example of airlines accepting QR payments on planes.

🔹 28:50 The future of payments?

The future of QR payments is unified QR code payment systems as the gov’t of Singapore has done. There is also Alipay+ which is bringing cross-border QR payment to all of Asia and even Europe! It sounds like science fiction but it's happening now. It's a beautiful future!

It sounds like science fiction but it's happening now. It's a beautiful future!

My work is entirely supported by reader gratitude, so if you enjoyed this newsletter, please consider subscribing or sharing it, and follow me on Twitter, or Linkedin. If you want to learn more about Innovation Labs or China’s CBDC, check out my website richturrin.com which is full of videos, interviews, and articles. The best way to make sure you see the stuff I publish is to subscribe to the mailing list here on Substack, which will get you an email notification for everything I post.

Everyone, including platforms that disagree with me, has my permission to republish, use or translate any part of this work (or anything else I’ve written outside of my books) with credit given to me and this site (richturrin.substack.com) free of charge. For more info on who I am, what I do, and where I’m going, check out richturrin.com

Rich Turrin is the international best-selling author of "Cashless - China's Digital Currency Revolution" and "Innovation Lab Excellence." He is number 4 on Onalytica's prestigious Top 50 Fintech Influencer list and an award-winning executive previously heading fintech teams at IBM following a twenty-year career in investment banking. Living in Shanghai for the last decade, Rich experienced China going cashless first-hand. Rich is an independent consultant whose views on China's astounding fintech developments are widely sought by international media and private clients.

Please check out my books on Amazon:

Cashless: (https://amzn.to/3RcC6PB)

Innovation Lab Excellence: (https://amzn.to/3C35Mcr)