Tokenization: A $30tn Market Waiting to Happen (Part 1)

Part 1: Standard Charter sees tremendous opportunity in trade finance

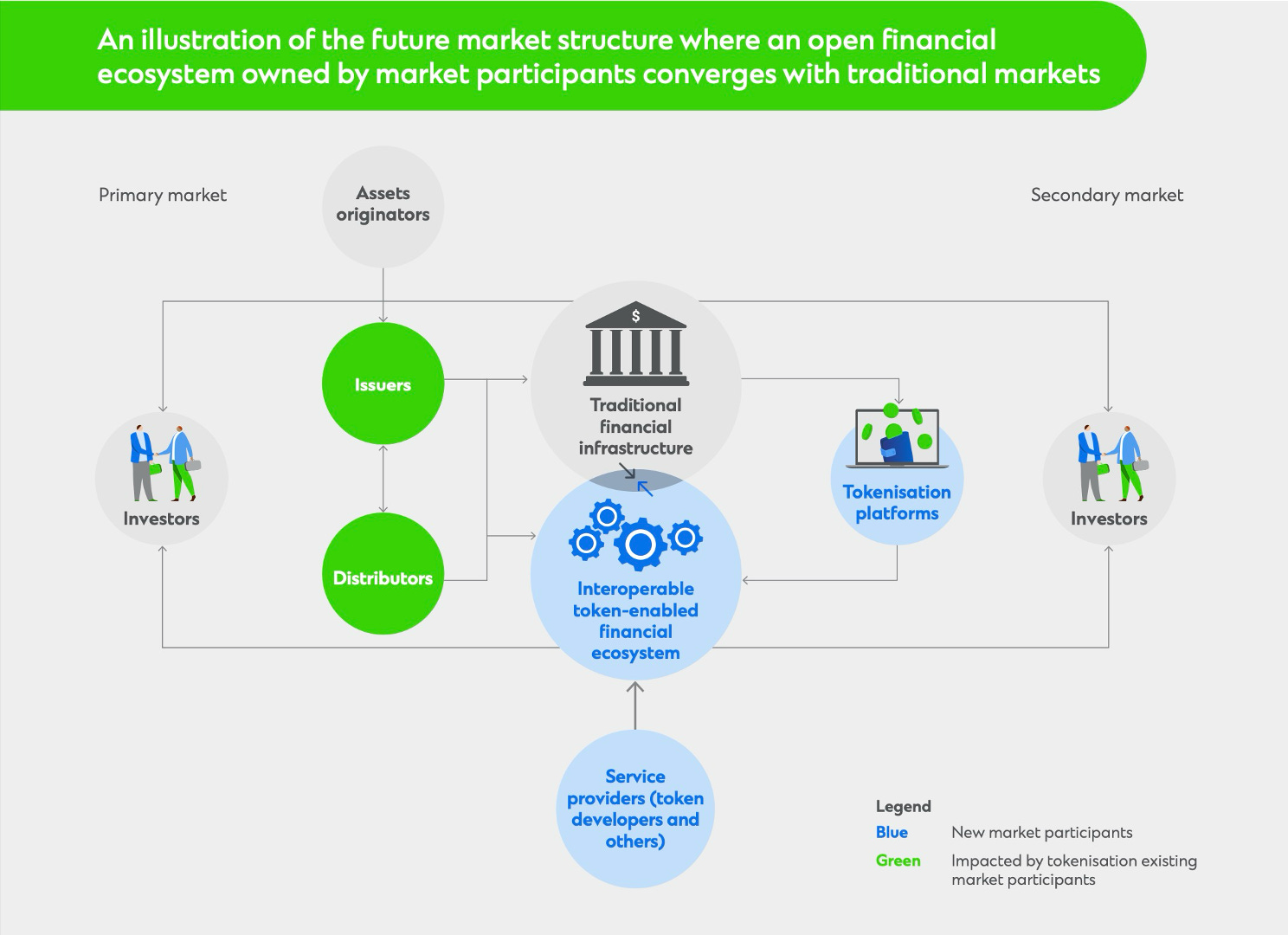

Standard Chartered claims that the market for tokenized assets will reach $30.1 tn in ten years, of which 16%, or $4.8tn, will be in trade finance!

👉Part 1: How real and big is tokenization: HERE

👉Part 2: Singapore’s GL1 shows Asia is leading tokenization: HERE

👉Part 3: Real example of why programmability is so important: HERE

While I believe StanChart’s $30 tn market estimate is high, I think they’ve got the right number of zeros when compared to McKinsey’s paltry $2 tn estimate from a few weeks ago.

My rationale is simple tokenization technology’s gains in efficiency will mean that anything that can be tokenized will be.

StanChart is betting on two major factors driving the market for tokenized trade finance assets: market need and investor demand.

👉TAKEAWAYS

Trade Finance Market Need

🔹 Global trade is projected to grow by 55% over the decade, reaching $32.6 tn by 2030

🔹 There is a critical gap between trade financing demand and supply, particularly for SMEs in developing nations.

🔹 The gap has increased dramatically from USD 1.7 tn in 2020 to $2.5 tn in 2023. Adding to this is another potential $2.5tn in unreported trade demand.

🔹 65 mn firms, or 40% of formal micro, small and medium enterprises (MSMEs) in developing countries, have unmet financing needs.

Investor Demand

🔹 Tokenisation is not a fleeting trend; it’s a fundamental shift in investor preferences.

🔹 Demand is expected to soar, with 69% of buy-side firms planning to invest in tokenised assets by 2024, up from 10% in 2023.

🔹 By 2024, investors aim to allocate up to 6% of their portfolios to tokenised assets, rising to 9% by 2027.

🔹 The current total value of tokenized real-world assets is a mere $5 bn! (excluding stablecoins)

👊STRAIGHT TALK👊

StanChart is likely overestimating the potential market size of tokenization and it is essential to note that their market estimates include real estate, which is an easy way to make estimates like this explode!

Still, I agree that the market will be trillions with two digits, and StanChart’s explanation of the benefits of tokenization is the reasons why:

Improving market access;

Simplifying trade complexity;

Digitizing securitization;

Reducing information asymmetry.

Regarding market needs, StanChart, an Asia specialist bank, is correct that Asia’s SMEs have an unfilled need for trade finance.

Here again, the bank is on target, and its two pilots outlined in the paper undertaken during Singapore’s Project Guardian show that they mean business!

StanChart’s plan falters in its assumption that investors will want to buy ABS securities based on SME trade finance deals.

While there is a market for everything, these high-risk securities would seem an unlikely buy for an asset manager’s first or early venture into tokenized securities!

Tokenization is great tech, and investors understand and welcome its role in securitization, but it won’t make them jump into new asset classes overnight!

I have no doubt securitization markets will gain significantly from tokenization, but tokenization cannot spin flax into gold!

What do you think?

Part 2

Part 3

Join our community by subscribing. You’ll be joining an exciting journey down the rabbit hole to our shared digital future—and you’ll be glad you did!

Sponsor Cashless and reach a targeted audience of over 50,000 fintech and CBDC aficionados who would love to know more about what you do!