Tokenization Coming to Alternative Assets as Moody's Gives its Blessing

The high priest of finance likes tokenization!

You know, tokenization is going mainstream when Moody’s, the high priest of finance, comes out with an article boasting that tokenization is just what alternative assets need.

Note that Moody’s didn’t go as far as to say -all- assets, but at least alternative assets are a start.

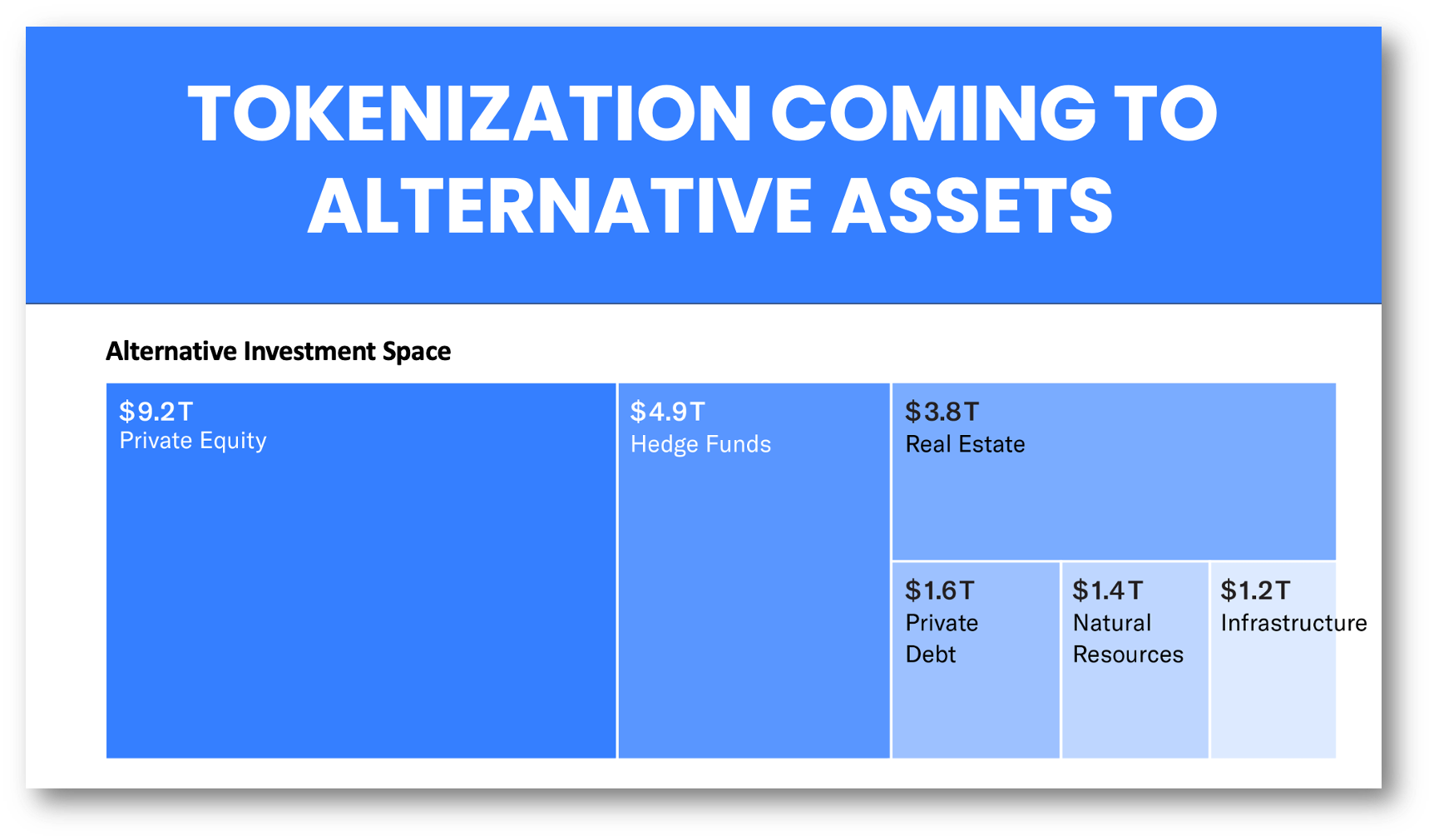

Why alternative assets? Easy, alternative assets are illiquid and include anything from private equity, hedge funds, real estate, art, or even Ferarris.

These illiquid markets need a way to fractionalize their holdings and trade them in open markets.

Where there is smoke, there is fire, and with so many major players in finance writing about tokenization it won’t be long before it is the norm.

👉TAKEAWAYS

🔹 Secondary markets powered by blockchain could improve alternative assets' liquidity.

Blockchain networks could offer a clearer view into the relatively opaque world of alternative assets thanks to token holders' real-time information on their tokenized assets.

🔹 Tokenization of alternative assets could lower costs for investors and distributors.

For investors, efficiencies gained through tokenization, such as lower issuance costs, could translate into higher returns, as asset managers pass on some of their savings.

🔹 Small-scale transactions are already underway in the tokenized alternative assets space.

Traditional financial institutions have already made some of their private equity and private credit investment opportunities available on private and public blockchains3 through feeder funds.

🔹 Tokenization of alternative assets faces several hurdles.

Regulatory and legal uncertainty stands as a principal barrier, with many aspects of tokenization still in a legal gray area. There are technical hurdles, particularly the critical need for seamless integration between on-chain and off-chain operations.

👊STRAIGHT TALK👊

What is -absolutely- indisputable is that tokenization is a game changer in illiquid markets for alternative assets.

Blockchain is perfect for fractionalizing assets while embedding the conditionalities that govern their value through smart contracts.

This is new territory.

Traditionalists may argue that the impact of tokenization on existing -liquid- securities markets will be minimal as these markets are already efficient.

I disagree, but tokenization’s impact on the alternative market has few naysayers, which is why Moody’s gave it its blessing.

If there were ever a mainstream proponent of financial orthodoxy, it would be Moody’s, which is why this report is astounding to me.

Watch carefully; banks, regulators, and Moody’s, among many other mainstream financial services players, are all focusing on tokenization.

Where there’s smoke,illiq there’s fire!

Thoughts?

Thank you to all my subscribers who have been sharing Cashless! You are now the No. 1 driver of subscriptions!

Use this “Share” button to share on social media, copy the article link, or email friends. It’s easy and only takes 2 seconds!

Join the community by subscribing! You’ll be glad you did! All it takes is your email!

Sponsor Cashless and reach a targeted audience of over 50,000 fintech and CBDC aficionados who would love to know more about your company.