Tokenization is the evolution of banking, can they evolve fast enough?

Banks face four potential futures three of which are very bad for banks.

Tokenization is coming for bank high-value wholesale transfers, and Oliver Wyman predicts four potential futures, all of which involve lower margins.

The biggest question is: Can banks or traditional finance (TradFi) evolve fast enough? I think they can! This time they don’t have a choice; they see the digital writing (QR Code) on the wall!

The best way to predict the future is to build it.

Oliver Wyman nails it!

👉TAKEAWAYS

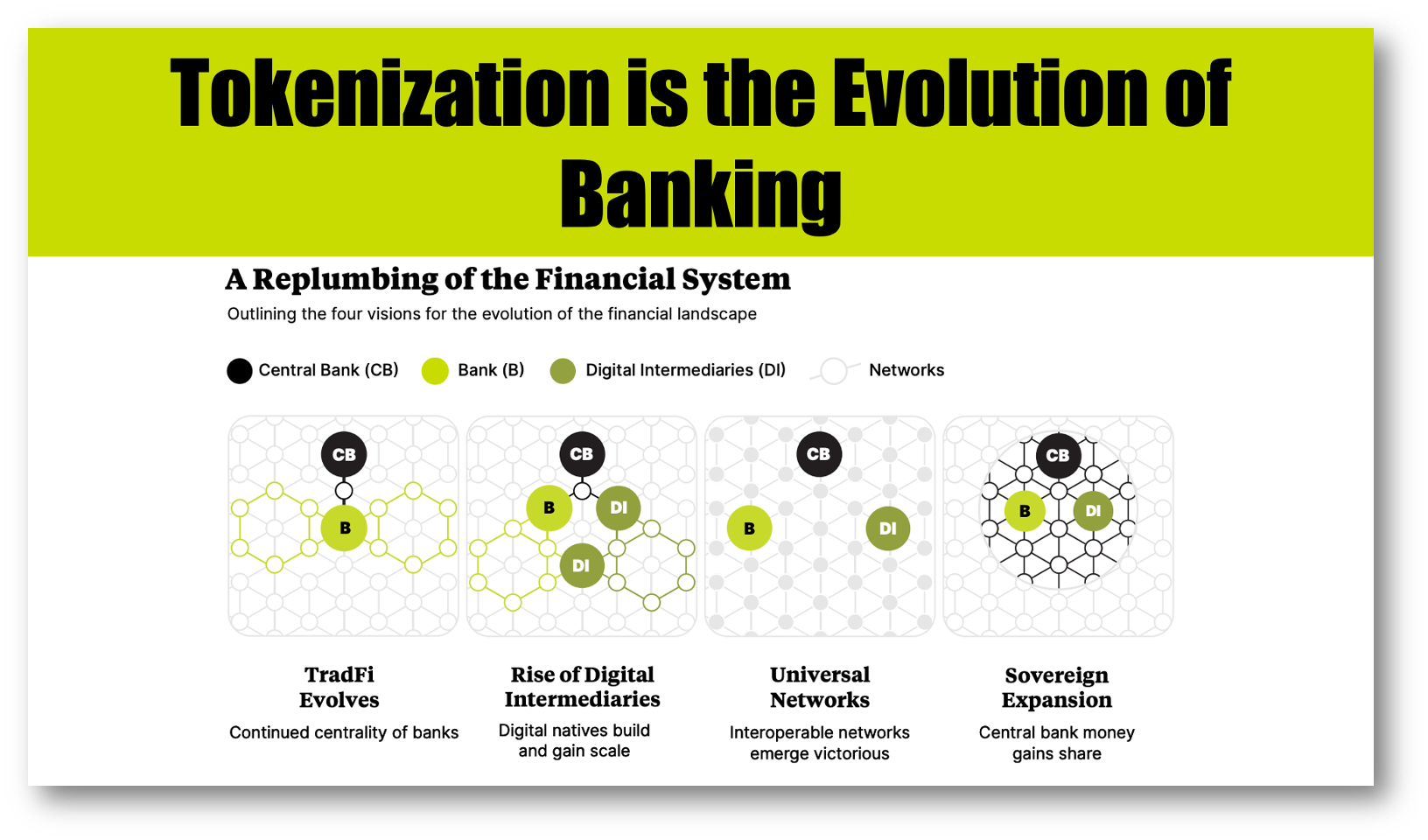

Tokenization will give rise to four potential futures for bank high-value transfers all of them will reduce costs and some of them will reduce banks’ pivotal role.

FOUR POSSIBLE FUTURES With my vote as to likelihood 👍 or 👎

1. TradFi Evolves 👍 Most likely!

TradFi evolves successfully by embracing DLT, such as blockchain. The problem is that this requires a radical change in how banks, exchanges, and other financial institutions operate their middle and back offices, but it wouldn't involve a significant change in market structure.

2. Rise of Digital Intermediaries 👍 Will happen whether banks like it or not.

A new class of intermediaries evolves unencumbered by legacy technology, which can provide investors and borrowers connectivity across emerging networks. Candidates include stablecoins, tokenized money market funds, and tokenized government securities.

3. Universal Networks 👎 Complicated is anything universal anymore?

New open networks that use interoperable standards and protocols allow the deployment of institutional-grade decentralized finance (DeFi) to permit competition among various money issuers and digital solutions. Such models are already being tested.

4. Sovereign Expansion 👎 Regulators are in banks pockets, no way no how.

While most governments and central banks that are studying or experimenting with central bank digital currencies (CBDCs) aren’t looking to fundamentally change their roles, crisis or politics may demand that change.

Tokenization will bring a new world where transfers are immediate. With it will come new products, new competitors, and a system that will better serve the needs of society. Banks will no longer have “primacy” in cash transfers even if they maintain a commanding role.

👊STRAIGHT TALK👊

Let’s dive in and see why I think that banks will evolve, though they will no longer own the market completely!

Banks are evolving; fear works

Tradfi is already evolving. They see the digital handwriting on the wall (a QR code?) and are already working on building tokenized deposit transfer systems.

The most famous example is from JP Morgan, which is handling $1 billion a day. This is tiny compared to JP’s $6 trillion in daily transfers, but it it shows that they are aware of the need to change. Citibank also recently launched a similar network for wholesale clients.

Let’s be clear about these banks’ motivations. No bank has any great love for tokenization. They are doing it because of the massive disruption they wish to stave off from CBDCs and non-bank intermediaries. Fear works!

So, I give banks credit they are evolving because they wish to maintain their role, even if it is at a slightly diminished capacity due to competition.

Intermediaries on the rise

Understand that large banks like JP Morgan will have a decided advantage over smaller rivals by using token-based transfers. The only way smaller rivals can compete is to use an intermediary, and there will be many. Whether stablecoin, CBDC, or other token, there is a clear need.

These intermediaries will perform two critical roles. First, they will show banks that they aren’t the only game in town ending bank primacy. Second, and more insidious, they will put a cap on bank margins for transfer!

Universal?

First, let me clarify that this is not crypto DeFi, but institutional DeFi. I love it and think it will be a game-changer in the future.

That said, it won’t be ready for rollout for another 5 years, and the solutions above are ready to go now. I also think that “universal” is a tough sell. Banks will run these blockchain networks on a consortia basis, and it’s likely you’ll see competing networks out there.

CBDC

Every central bank designing a CBDC is bending over backward to avoid infringing on banks’ role in society. Given how banks work in concert with regulators, I find it inconceivable that they would suddenly change direction. Nothing short of a revolution could make this possible.

That doesn’t mean CBDC won’t have a role to play in transfers! It most definitely will, but it won’t disrupt banks so much as complement their existing tokenization efforts, by adding another new payment channel.

The best example of this is the European Central Bank’s trials of wholesale CBDC scheduled for early 2024!

Margins can’t be saved.

One thing that must be acknowledged is that bank margins for cash transfers will decline. There is no way that banks can continue to depend on rich transfer margins for much longer. This is fundamentally good for all society even if bankers complain about it!

It takes two seconds to forward this newsletter and subscribe!