US is behind the curve with blockchain and data, The IMF's Money Revolution, Fintech in Africa, 2022 Tech Trends

Singapore lays down the law for crypto!

1. The IMF’s Money Revolution

2. The US is behind the curve with blockchain and data

3. Singapore lays down the law for crypto

4. Fintech in Africa is booming!

5. Technology Trends Outlook 2022

Andy Warhol Dollar Sign Portfolios, 1982 No other series reflect mass identity, luxury, and wealth as prominently as Warhol’s Dollar Sign Portfolios: The Andy Warhol Foundation of Visual Arts

1. The IMF’s Money Revolution

IMF publishes “The Money Revolution” covering Crypto (it hates it), CBDC (it loves it), and the future of finance.

The IMF’s “magazine” covering digital assets is a must read! Kudos to the IMF for assembling such a thoughtful review. That the IMF is no fan of crypto is a given bias, let’s face it this is the IMF. Still in several articles, particularly those focusing on DeFi the IMF extends an olive branch to crypto.

Download: here

The IMF got a dream team of digital currency experts together for this wonderful read on Digital Currency. Unsurprisingly, the IMF is pro-CBDC and anti-crypto so don’t be alarmed or offended by articles like “The Superficial Allure of Crypto.”

There are too many SUPERB articles in the publication to write about so I'll likely cover more in-depth this coming week.

For now, lets look at 3 articles :

1️⃣ Bullet Train, pg 20

This is the IMF’s signature article where it states that it wants nothing short of “a radical transformation” of cross-border payments. To achieve this the IMF is going “all in” on CBDC and tokenized assets.

The IMF sees our existing cross-border transfer system as deeply flawed: “Only a handful of very large institutions...controlling the correspondent banking market. It’s no surprise our payments are costly, slow, and opaque.”

Unsurprisingly, the tool for the transformation will be CBDCs which it calls the least risky digital asset while leaving the door open for stablecoins and tokenized bank deposits.

It’s a fine vision for the future and the IMF lending its significant weight to a CBDC-based future means change is coming. The IMF teased the launch of two papers with more details of its vision coming soon.

2️⃣ ‘DeFi’ and ‘TradFi’ Must Work Together pg 24

Kudos to Michael Casey for bringing “détente” to the relationship between crypto and traditional finance worlds!

“The reality is, both sides need each other. If they are to attain mainstream adoption, DeFi and crypto must integrate some of the regulatory and self-regulatory practices that have brought functional stability to TradFi.”

He lays out a great case for crypto and traditional finance to work with one another in reasonable partnerships. Casey even covers contentious areas like Bitcoin's voracious energy appetite!

3️⃣Taking Digital Currencies Offline, pg 64

My friend John Kiff, a frequent contributor on Twitter and Linkedin, wrote the most significant article about CBDCs!

John hits us with the truth bomb that if CBDCs are going to bring the benefits of financial inclusion to developing economies they must have offline functionality. “75% of the world’s adult low-income population that doesn’t even have internet access.” How exactly will an online CBDC help them?

This is precisely why China's PBOC specified offline e-CNY usage at the very start of the project. For the EU and US offline use seems an afterthought.

Takeaways:

The digital currency revolution is happening faster than you think

That the IMF is going “all-in” on promoting digital is unto itself newsworthy

Look at the writing in this publication, it’s not for policy wonks but aimed at normal people to help them understand the transition we’re facing.

Kudos to the IMF, and authors for such a thoughtful read!

2. The US is behind the curve with blockchain and data

“The US is behind the curve on blockchain” as the tech is raised to the level of a national security concern worthy of the Defense Dept.

Read “War on the Rocks” article “The US is Behind The Curve on Blockchain” by Mike Knapp”: here

Read this excellent overview of China’s view on data as a fifth factor of production by Lillian Li here on Substack: here Reading this will help you understand WHY China cracked down on tech companies. Treating data as a factor of production will be key to changing how the US treats data, the EU is already making this transition.

“Lacking a firm understanding of blockchain, the United States risks competing in an information environment dominated by China.” Says Mike Knapp in this FABULOUS article in “War on the Rocks,” a defense journal afield from my normal fintech reading, that shows how blockchain is far bigger than the latest altcoin.

I’ve written about China’s national “Blockchain Service Network” (BSN) for years and in 2020 called it:

"the biggest event in computing since the cloud." Here

Now come defense analysts who view blockchain as a strategic technology. “Blockchain is not a weapon system by itself — it is a critical enabling technology of the information environment.”

Now if this article isn’t enough look here to see how China’s emphasis on blockchain plays into its development of Web3. “China’s focus on the “chain” rather than the “coin” helps ensure that cryptocurrency hype does not affect the development and utilization of blockchain technology.” Read Technode: Web3 in China: Will it happen, and what form will it take?

This is no joke, while Web3 development in the West seems to focus on its ability to shill crypto, China's national blockchain tech establishes a strong foundation for Web3. There is no doubt that China’s Web3 will be “fit for purpose” and compliant with regulations. Whose Web3 would you bet on?

While the US views data primarily as a playground for big tech to enrich itself, as a tool for ICE to track migrants, or for covert NSA operations (thank you Ed Snowden) China thinks about it very differently.

Data, the fifth factor of production

While mostly lost on tech policy wonks like me, in April 2020, the State Council formally designated data as a factor of production, right up there with land, labor, capital, and technology. Let the enormity of this sink in.

Then to back it up the 14th China's 5-year plan calls for “the sharing of public data related to demographics, transportation, and telecom through a unified national open data platform.” China’s new data exchanges in Beijing and Shanghai are not accidents.

So while the US views blockchain as a “technology of tomorrow,” it is readily being rolled out nationwide in China. As I state in “Cashless” it won't stay in China, and BSN will go international through Belt and Road countries.

This doesn’t mean the US is doomed or that China is going to take over the planet because of its blockchain savvy.

It means that the US & EU need to examine the role of blockchain and data in society. To their credit, the EU has already taken steps in this direction with GDPR and AI laws while the US does nothing.

Takeaways

We deserve more than a blockchain policy based on crypto adverts.

The US is woefully behind in recognizing blockchain’s potential and far behind the EU in recognizing society’s relationship with data.

Data’s role in society requires a rethink as does how we use blockchain technology and once again China provides a window into our shared digital future.

China considering data as a 5th factor of production fundamentally changes society’s relationship with data and calls into question big tech’s monopoly.

3. Singapore lays down the law for crypto

The Monetary Authority of Singapore lays down the law for crypto in a truth-bomb speech that calls out retail crypto investors for being “irrationally oblivious about the risks.” Menon’s candor is refreshing!

Ravi Menon’s speech on crypto shows why Singapore is not going to be the free-wheeling crypto capital as many had hoped. While villainized by many in the crypto world this speech nicely captures what most regulators fear about crypto. My marked-up version of the speech: here

Let’s make it clear from the start that Singapore is still smarting from three black eyes due to the collapses of crypto firms: Three Arrows Capital, Terra, and Holdnaut.

While Singapore gracefully absolved itself of any responsibility for all 3 failures, they tarnished Singapore’s fastidiously guarded reputation. With FinServ making up 13% of GDP this is no joke.

MAS MD Ravi Menon who delivered this speech is being savaged by the crypto press who decry that Singapore’s pursuit of fintech innovation does not include crypto.

In response, I’m publishing his speech in its entirety to let you decide!

🔹Slamming crypto:

• MAS regards cryptocurrencies as unsuitable for use as money and as highly hazardous for retail investors.

• Speculation in cryptocurrencies is what MAS strongly discourages and seeks to restrict.

• Cryptocurrencies lack the three fundamental qualities of money: medium of exchange, store of value, and unit of account.

• Outside a blockchain network, cryptocurrencies serve no useful function except as a vehicle for speculation.

• Consumers are increasingly trading in cryptocurrencies. They seem to be irrationally oblivious about the risks of cryptocurrency trading.

🔹Supporting DLT, tokenization, and stablecoins:

• The most promising use cases of digital assets in financial services are in cross-border payment and settlement, trade finance, and pre-and post-trade capital market activities.

• The concept of asset tokenisation has transformative potential, not unlike securitisation 50 years ago.

• MAS sees good potential in stablecoins provided they are securely backed by high-quality reserves and well regulated.

🔹No retail CBDC for Singapore:

• MAS sees good potential for wholesale CBDCs, especially for cross-border payments and settlements.

• MAS does not see a compelling case for retail CBDCs in Singapore.

• I agree, with 6 mn well-banked inhabitants who already have real-time payment what will a retail CBDC achieve?

🔹And makes clear MAS's regulatory priorities:

• AML and terrorist financing

• Cyber risks

• Safeguard retail investors

• Ensure stablecoins are stable

• Mitigate financial stability risks

Menan says that innovation and regulation go “hand in hand.” But craftily adds: “We do not split the difference by being less stringent in our regulation or being less facilitative of innovation.”

Takeaways

Singpaore’s black eyes are very real. Terra’s founder Do Kwon lives freely in Singapore while awaiting likely extradition to Korea, and the 3AC founders fled the country!

You decide whether the MAS is an enemy of crypto or simply doing its job as a regulator to ensure Singapore does not become a home to illicit money flows.

In my view, Menon’s speech was simply perfect as it clearly laid out the fears of regulators everywhere with a degree of candor that is rarely seen.

4. Fintech in Africa is booming!

Fintech in Africa is set for explosive eightfold growth by 2025 according to McKinsey.

McKinsey reports not just “fintech disruption” but “fintech eruption" in Africa! It's true, even if McKinsey’s 8X figure is a stretch! What McKinsey doesn’t show in the chart is that Kenya’s population has 98% mobile penetration. Download: here

There is no question that Fintech is booming in Africa:

“Between 2020 and 2021, the number of tech startups in Africa tripled to around 5,200 companies.” “Estimated revenues of around $4 billion to 6 billion in 2020 and average penetration levels of between 3 and 5 percent.” Fintech also garners 54% of known startup funding in Africa.

McKinsey’s leap of faith is a bit too long

Now for McKinsey’s leap of faith: “If the sector overall can reach similar levels of penetration to those seen in Kenya, a country with one of the highest levels of fintech penetration in the world, we estimate that African fintech revenues could reach 8X their current value by 2025.”

"The big if" is whether the rest of Africa can match Kenya? McKinsey is being very optimistic! The problem isn’t fintech, but mobile penetration. Kenya has 98% mobile phone penetration!

Sub-Saharan Africa which currently has a mobile penetration of 46% will struggle to attain such a high number in 3 yrs, even with Huawei's help! Huawei makes up 70% of Africa’s mobile networks.

Still, whether growth is 2X or 8X it's clear Africa's fintech is growing fast. It has to! 65% of Africans are underbanked or unbanked, and 90% of payment transactions are in cash! Inclusion is necessary!

11 key countries with 70% of Africa's GDP and 1/2 the population will be at the center of the fintech revolution: Cameroon, Côte d’Ivoire, Egypt, Ghana, Kenya, Morocco, Nigeria, Senegal, South Africa, Tanzania, and Uganda.

So what is the secret for fintech success?

1. Match value proposition to the market:

Understand the market, including customer needs and where the specific market stands on its infrastructure development journey.

2. Acquire a large base of active users quickly:

Scaling requires either pricing or a physical distribution networks.

3. Have clear monetization strategies that are rolled out effectively:

Strong and effective monetization strategies must notput growth at scale ahead of profits.

4. Manage lower expected revenue per customer:

Africa has the lowest-income population on the planet, expenditures are 10x lower than that of N. America and 5X lower than in Europe.

5. Understand and address Africa’s offline market:

Same with CBDCs! Offline physical presence is essential!

6. Actively engage, align with, and work with regulators:

Align regulatory policies, and work with governments.

Takeaways

Africa’s fintech development is amazing!

Expect big things, not miracles McKinsey’s 8x figure is not credible!

Watch as Africa becomes a focal point for CBDC development with Nigeria’s eNaira already launched and Ghana’s eCedi coming soon.

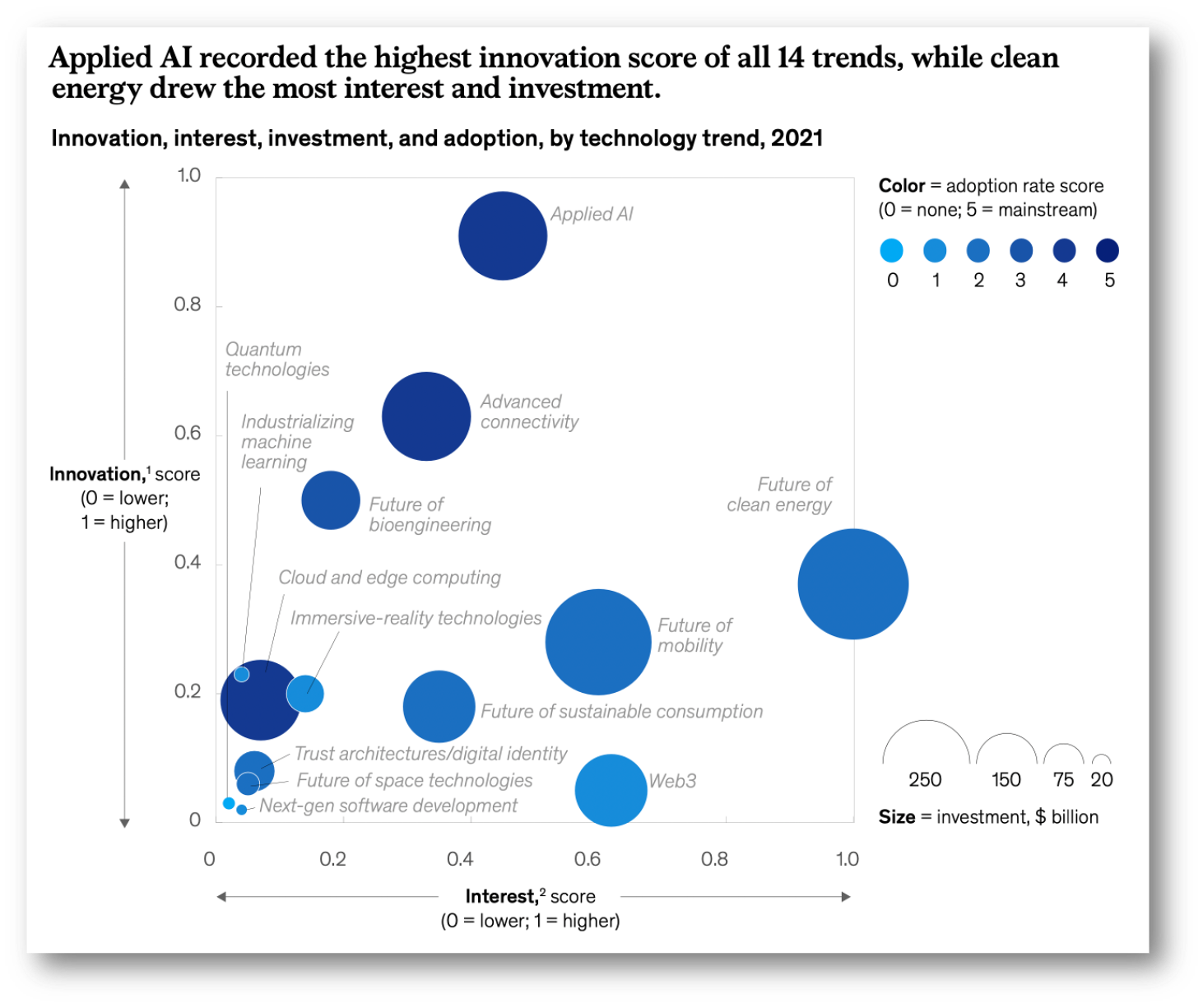

5. Technology Trends Outlook 2022

Mckinsey lists the top 14 tech trends that you need to follow so that you don’t fall into premature obsolescence!

“McKinsey Technology Trends Outlook 2022” is a great read that shows just where the money is going. Download: here

This article is a departure from CBDC and fintech I normally write about to bring some important perspective on other tech trends that are changing our world.

In this concise report, McKinsey ranks the top 14 tech trends by three critical factors: 1) Innovation; 2) Interest; and 3) Investment.

As a firm believer in “money talks, BS walks” I’m going to look at the top 3 by funding just to filter out what should take the top 3 spots on your radar.

Surprisingly, some of the tech we know and love like space tech and VR do not attract the money that you might assume. (Pg 5 Exhibit 1)

1️⃣ Future of clean energy, $257 billion

Here the focus is on “energy solutions that drive toward net-zero emissions span the entire value chain, from generation or production to storage and distribution.”

It probably will come as no surprise that clean energy captures the largest investment amount of any of the technologies covered as it is central to our planet's existence. The problem is not just technical, but one of supply chains and critical components that are sourced internationally. This is an area where no single nation can “go it alone”.

2️⃣ Future of Mobility, $236 billion

“More than a century after mass production of automobiles began, mobility has arrived at a second great inflection point: a shift toward autonomous, connected, electric, and smart (ACES) technologies.”

Still waiting for autonomous driving electric vehicles? You’ll have to wait a bit longer, but autonomous trucks and loading vehicles in ports are here now. While the tech challenges are enormous, removing or reducing the human element in transport is critical for smart cities and logistics. Batteries and their reliance on rare earth elements inject geopolitics into this solution more than most.

3️⃣ Applied AI, $165 billion

"In a 2021 McKinsey Global Survey on the state of AI, 56 percent of respondents said their organizations had adopted AI, up from 50 percent in the 2020 survey.”

No surprise that AI continues to be a “best seller” with increasing uptake across all industries. Security and regulating AI’s behavior remains an ongoing concern, and we are at a point where regulations would help.

While I’ve done my best to avoid talking about CBDCs, check out page 29 on “trust architectures and digital ID. While still small in terms of investment it's a critical technology for CBDCs and digital payments.

Takeaway

There is so much going on in tech, other than fintech, that will have a profound impact on society it's staggering.

While fintech is great, it is important to keep it in perspective with what I would venture to call even more important technologies.

Thank you for reading!

Hey did I mention that subscribing is a great way to say thanks? Every new subscriber helps me get my message out to more people!

More of my writing, podcasts, and media appearances here on RichTurrin.com

Rich Turrin is the international best-selling author of "Cashless - China's Digital Currency Revolution" and "Innovation Lab Excellence." He is an Onalytica Top 100 Fintech Influencer and an award-winning executive previously heading fintech teams at IBM following a twenty-year career in investment banking. Living in Shanghai for the last decade, Rich experienced China going cashless first-hand. Rich is an independent consultant whose views on China's astounding fintech developments are widely sought by international media and private clients.

Please check out my books on Amazon: