Visa: the Victim of the Money Movement Revolution, Not the Revolutionary

Visa is correct a revolution is underway and Visa is dodging the bullets.

Visa with a fun read about the money movement revolution, a revolution where digital wallets fired the first shots, and Visa is dodging the bullets.

Visa is correct to point out that payments are rapidly changing, but many of the 12 key issues they highlight show how Visa is being disrupted!

If you enjoy this article, subscribe!

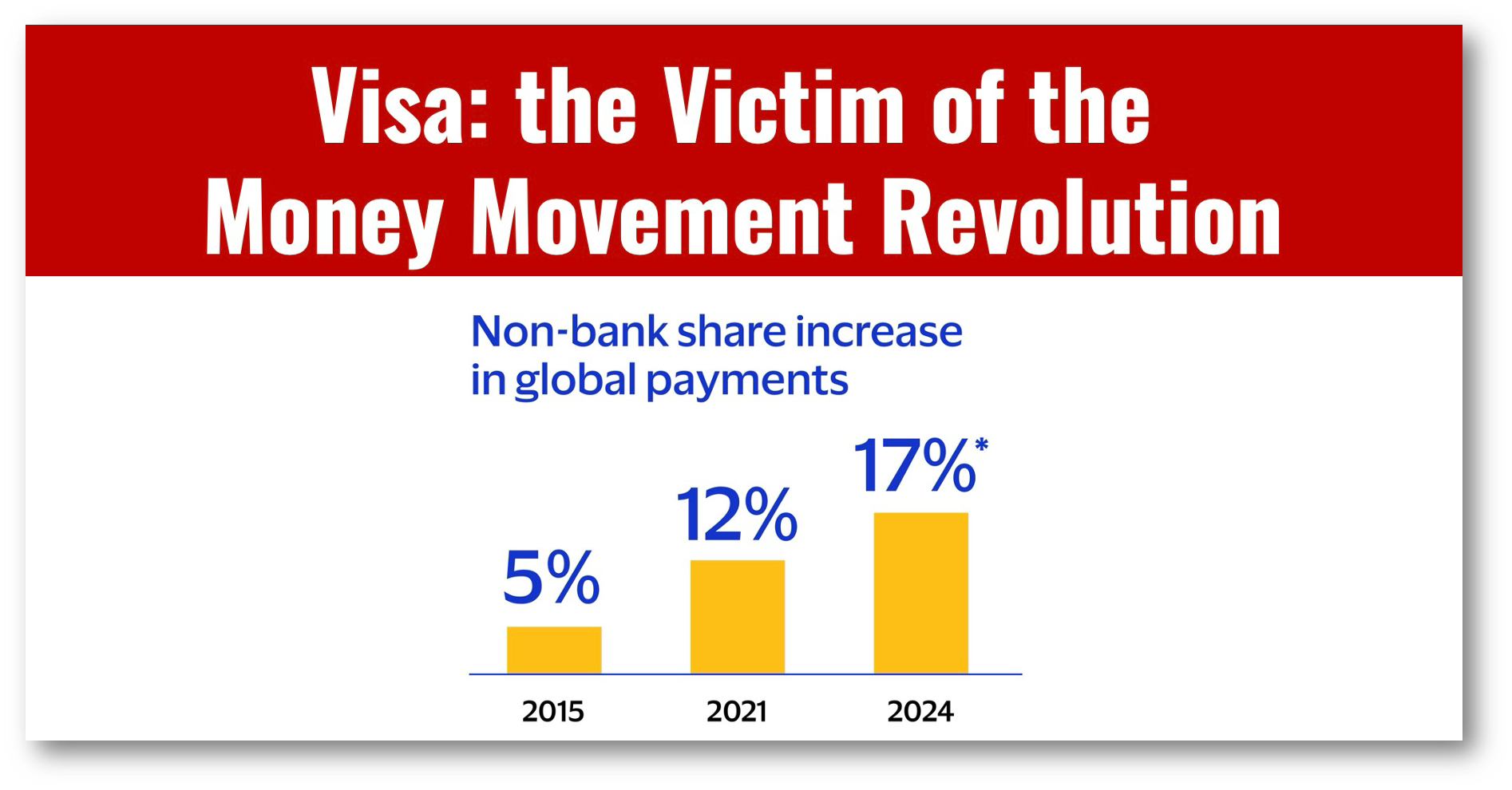

What Visa should be losing sleep over is that for much of the world, Visa never was the dominant payment system and never will be. They have failed to evolve and are being beaten by local payment systems that better suit local needs and are, for the most part, far cheaper to use.

Let’s take a look at my favorite six of Visa’s twelve key points as I show how Visa long-term is in a lot of trouble.

👉Visa’s key Points on Money Movement: My comments following showing how they are in trouble

The movement of money has expanded. “Money movement is going through a period of incredible momentum.”

My take: Yes, but digital wallets move the money! Digital wallets like WeChat and Alipay in China alone now handle roughly twice the payment volume of the global Visa and MC network. Who is doing the moving? Add on India’s UPI and other Asian digital wallets, and Visa is losing not winning, market share.

Domestic and cross-border payments are developing at very different rates. Across Asia there are countless examples of low cost and frictionless instant payment services domestically. ….“It will take many years before

the industry delivers cross-border money movement that is global, secure

and frictionless.”

My take: Really? Ask India, Thailand, Singapore, the Philippines, and Malaysia, all of whom have now linked instant payment systems through mobile wallets. It didn’t take more than three years, and Visa isn’t part of the solution.

The distinction between payment, money movement and remittance has become blurred. “Payment has become money transfer, has become remittance, all together.

My take: This is true, but cross-border mobile money transfers have blurred the distinction between remittances and payments. Without the need to go to a special remittance agent, paying offshore is no different from any other payment. I give credit to Visa because this is one area they can help in.

Differentiators in any money movement proposition are trust, speed of remittance, pricing and user experience. Consumers vary in their priorities, but any successful provider will have to balance these four criteria.

My take: This is not true. Digital wallet transfers provide all four; there shouldn’t be a trade-off as Visa suggests. Most domestic mobile money solutions, by definition, tackle all of these factors.

The rise of digital wallets is unstoppable and a key engine of financial inclusion, particularly in Latin America, Asia and EMEA.

My take: Yes, I agree with Visa on this! The problem is that most of these new digital wallets don’t use Visa because of the high cost associated with the network. They simply built their own networks to cut costs to the bone.

Consumers don’t much care about underlying technology, nor do they need to see it. What they do care about is service, which they want to be seamless, reliable and cheap.

My take: Visa is correct. Consumers don’t care if their payments are handled on the Visa network or by any of the dozens of competitors that are popping up. As Visa is never the cheapest option, it will have difficulty keeping up with new entrants outside markets like the US, where it maintains a duopoly with MasterCard.

If you know someone who would like this newsletter, please share it with them and help grow our Asia, CBDC, and AI aficionados community!

Readers like you make my work possible! Please buy me a coffee or consider a paid subscription to support my work.

Sponsor Cashless and reach a targeted audience of over 55,000 fintech and CBDC aficionados who would love to know more about what you do!