Where is the cash?🌋 Credit card’s moment of truth🌋 Open banking’s new use cases🔹 A CBDC design I don’t like!🔹CBDC “5P” design framework

Shanghai's INCLUSION Conference focuses on the little guy.

1. Where is the cash?

2. Credit card’s moment of truth

3. Open banking’s new use cases

4. A CBDC design I don’t like!

5. CBDC “5P” design framework

Today’s art: Vesuvius, Andy Warhol, 1985

One of Warhol's most iconic artworks of the 1980s, the lithograph depicts Vesuvius during an eruption. With the bright colors typical of the artist and Pop Art, this work is charged with energy and shows the volcano in all its destructive power. Warhol explained that “the volcanoes seemed to be painted just one minute after the eruption.”

The “destructive power” of Account to Account (A2A) payments enabled by digital wallets has a Vesuvius-like impact on cash and cards!

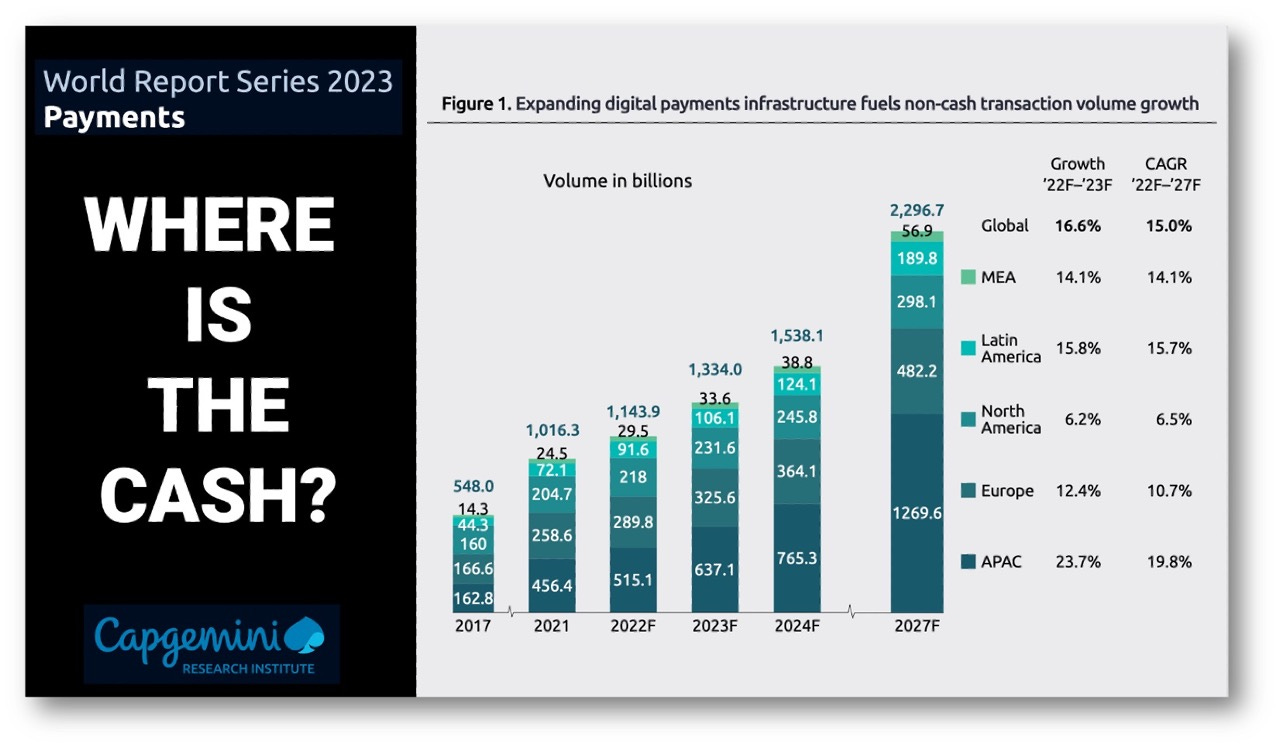

1. Where is the cash?

Where did all the cash go? Non-cash transactions chalk up a stunning 16.6% YOY global growth rate!

Another day another payment report showing how clients are running from cash transactions! This CapGemini report predicts a doubling of non-cash transactions in four years!

APAC, the global leader in going cashless, is even more stunning, with a STUNNING 23.7% YoY non-cash growth predicted in 2023!

Add this to the BCG payment report (story below) that shows a migration to alternative payments, and we get a clear picture that the “status quo” in payments is dead!

Here are the key points:

1️⃣ Expanding digital payments infrastructure fuels non-cash transaction volume growth

Non-cash volume will continue to grow at a CAGR of 15% during the 2022-2027 forecast period on the back of expanding instant payment schemes, initiatives to couple cross-country payment infrastructures, growing adoption of ISO20022, and the proliferation of new payment instruments (wallets, QR code payments, A2A payments, and more).

2️⃣ High costs and stressed revenues leave little room for innovation.

Managing the volume and velocity of key regulations and industry innovations comes at a significant cost for banks and payments firms. Moreover, revenues are also under pressure – limiting resources for innovation.

3️⃣ Enterprises with ineffective cash management services are vulnerable to business upsets.

On average, a multi-national corporate has more than 27 banking relationships to meet all of its treasury needs. Enterprise clients face challenges across the cash management value chain despite multiple banking partners.

4️⃣ Employ a layered approach to nurturing strategic relationships with corporate clients.

End-to-end digital transformation in transaction banking requires top-down commitment, cohesive planning, and a unified purpose for structural reforms. Banks and payment firms must overcome legacy barriers.

Thoughts?

👉TAKEAWAYS:

—Cash use is in decline globally, with a sobering 16.6% YOY decline.

—Regional variations are strong, with the EU and US posting smaller 12 and 6% declines, while APAC scored a stunning 24%!

—Incumbents’ innovation funds are shrinking, which all but hands payments to fintechs!

—Partnering with fintech payment firms is the only way for many incumbents to survive.

2. Credit card’s moment of truth

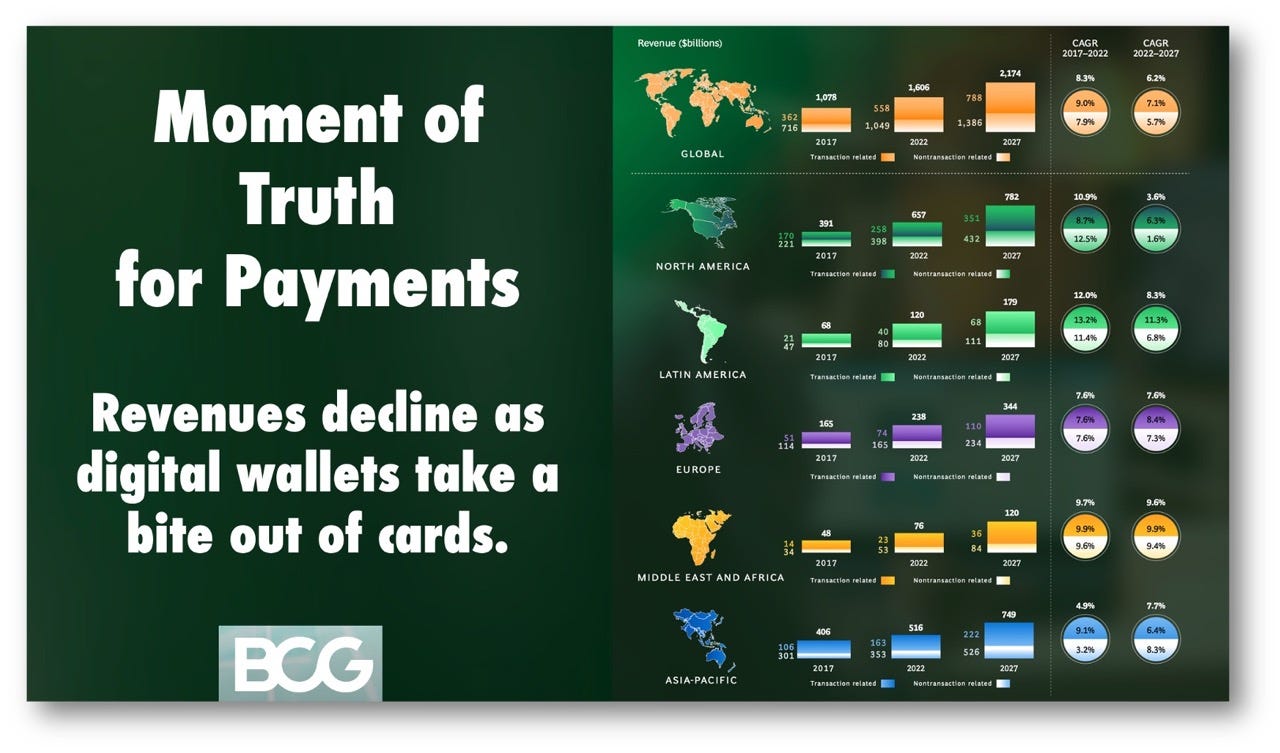

Global Payments 2023: A2A transactions take a bite out of cards’ fat margins and are growing 2x as fast!

The halcyon days of credit cards are behind us, as 5,000 global payment fintechs account for about $100 bn of total industry revenues, cut into incumbents’ card margins and revenue.

To make matters worse, by 2030, these fintechs could quintuple growth to command a revenue pool worth $520 bn! Then there are CBDCs launching in the next 5 years. What, then, of cards’ high margins?

I will shed no tears, how about you?

Here are a few shocking key points that show the level of disruption:

🔷 Total payments revenues grew at an annual rate of 8.3% from 2017 to 2022, taking the revenue pool to $1.6 tn at the end of 2022.

🔷 Revenue growth is likely to slow to 6.2% annually through 2027, with the revenue pool reaching $2.2 tn by then. Of this amount, transaction revenue from card and account-to-account (A2A) payments rails is on track to grow by 7.1%. But nontransaction revenue from interest- and fee-based sources is likely to expand by just 5.7%.

🔷 🔥Slowing revenue growth comes from an expected shift in the retail payments mix from cards to A2A transactions, along with compressed card margins in some markets. Contributing macroeconomic factors include cooling inflation and normalization in interest rates.🔥

🔷 🔥Total shareholder returns have plummeted. The top 20 largest payments companies saw their TSR drop by an average of 20% over the past two years. Acquiring and payments processing witnessed the sharpest declines, with TSR falling by roughly 40%.🔥

🔷 Digital currencies are moving from concept to reality, as more than 90% of central banks actively experiment with them as a complement to cash. At current rates of development, retail and wholesale CBDCs could be operational in some countries in every region in five to ten years.

Thoughts?

👉TAKEAWAYS:

—As predicted, payment fintechs are taking a bite out of card revenue and incumbents' profits.

—We all deserve a better deal in payments, so I won’t cry, how about you?

—Cards and incumbents won’t disappear but competition from fintechs will be expensive.

— A2A and CBDCs are bringing the cost of payments to near zero, and that’s what it should cost!

3. Open banking’s new use cases

Open banking is slow going as banks balk at sharing data and consumers don't understand the benefits.

"Open banking" took the banking world by storm even before “embedded banking” won the "Bank Buzz Word of the Year Award." It's still slow going!

Open banking is simple, offer consumers the chance to simplify financial activities and increase competition by allowing them to share data with others through their bank's APIs.

Banks, however, remain slow in opening and standardizing APIs for data sharing, even in the UK, where it is mandated by law. Data sharing doesn’t come naturally to banks, who prefer keeping a lock on data.

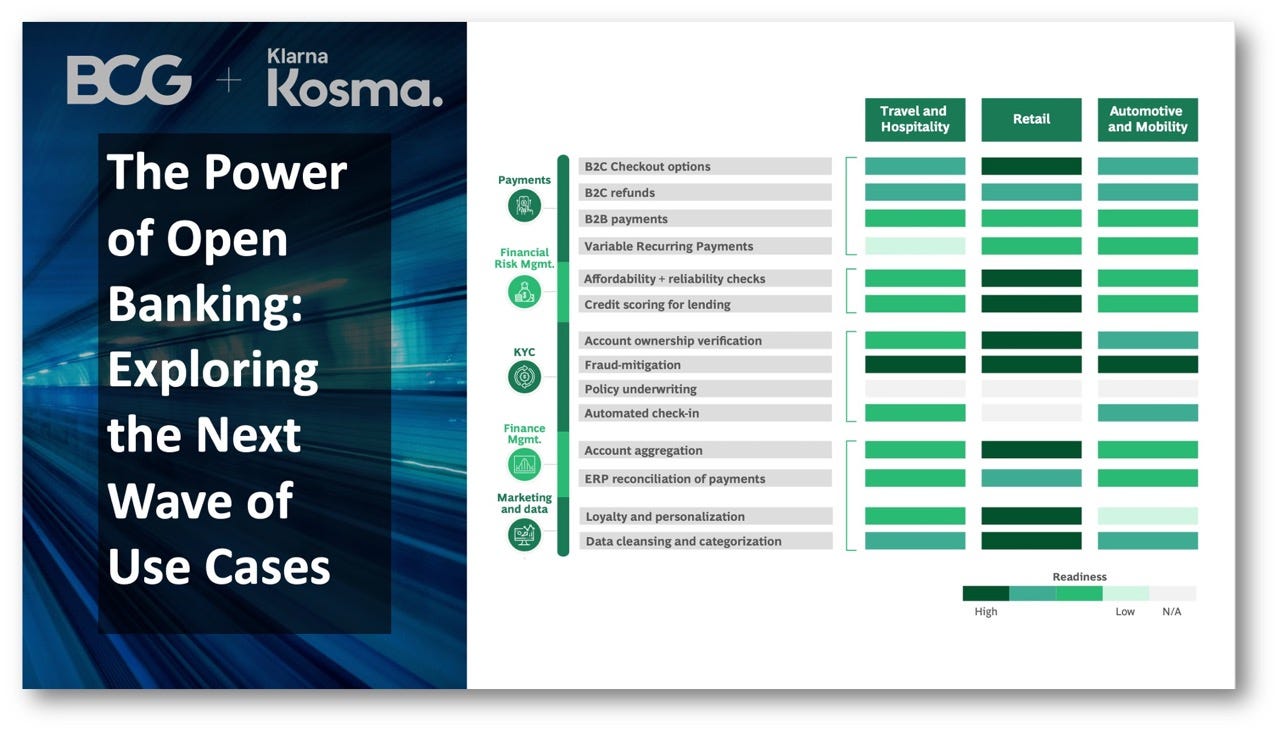

Most open banking use cases fall into one of two buckets: Basic or mandatory APIs, enabling access to payment accounts for distinct services, or premium APIs to unlock financial products beyond payment accounts such as investments or savings. (Great chart, Exhibit 2).

Now we should look to a “third wave” of open banking use cases which would expand the utility of the service to include far broader use cases.

Examples include:

🔷Financial Risk Management:

Companies in travel & hospitality, retail, and automotive can use transaction and account data to support more accurate credit risk assessment than is sometimes available through credit bureaus at specific points in time. Retail is the most advanced industry in terms of readiness.

🔷Account ownership verification:

Open banking can help companies verify client account ownership, complementing existing ID/KYC verification process. One potential use case is digital IDs, already used in some countries to enable access to a range of government services.

🔷Loyalty and personalization:

Open banking can provide unique information based on consumer buying behaviors. This can help merchants across industries create tailored marketing campaigns and personalized offers.

Open banking's data sharing is far more important to clients than embedding. Banks need to follow through and not get distracted by embedding.

Thoughts?

👉TAKEAWAYS:

—Open banking's data sharing is critical for clients, and banks must be pushed to do more.

—Banks loathe sharing data and far prefer the profits from embedding than the competition of sharing.

—Open banking's use in KYC is in EVERYONE's interest.

—Banks have delayed long enough.

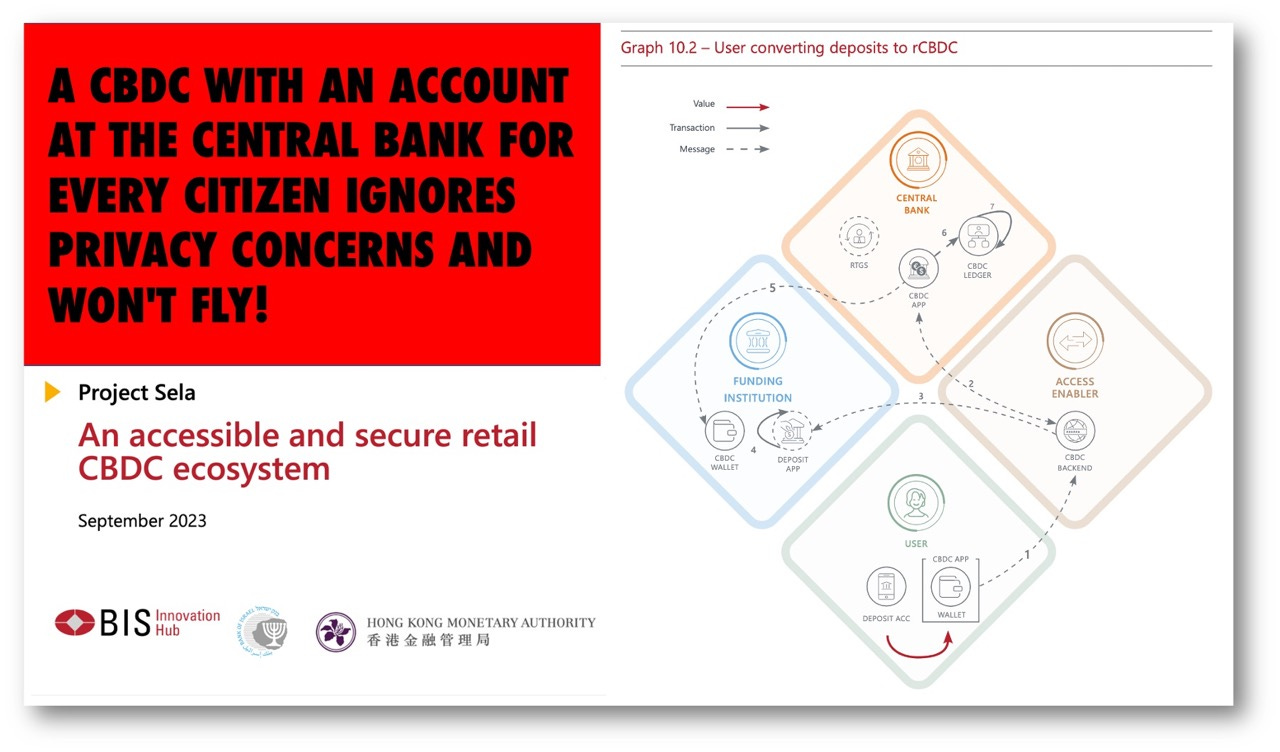

4. A CBDC design I don’t like!

Sorry, BIS, but a CBDC with an account at the central bank for every citizen ignores people’s privacy concerns and won't fly!

So finally, I’ve found a CBDC design that I really don’t like!

The BIS’s latest CBDC project is “Project Sela,” a collaboration between the BIS Hong Kong Monetary Authority (HKMA) and בנק ישראל Bank of Israel.

While I appreciate Sela trying to show a new rCBDC design, it comes with one HUGE drawback, it requires that the central bank have an account for every user!

So the design abandons tokens for accounts? Why? This is nothing more than a glorified central bank-sponsored WeChat Pay!

I honestly don’t think this CBDC will fly as it is tone-deaf to most people's privacy concerns.

A key feature in the system is creating a new player called an “Access Enabler” (AE). Its job is to be the customer-facing entity for your rCBDC accounts. AEs don’t “hold” users’ rCBDC on balance sheet; think of them as a form of CBDC agent.

How does it work? You select an AE, which provides an interface that accesses your rCBDC account at the central bank. In turn, the central bank accesses your bank account to move money into or out of your CBDC account as needed.

This system removes your bank from its guaranteed role as rCBDC intermediary, as in most two-tier systems. This is good for innovation but bad for banks!

This system achieves three things that aren’t all bad:

1. AE’s don’t hold money, so it removes complexity, costs, and risks from rCBDC service providers; they don’t have to be banks.

2. AE’s aren’t just banks but credit card companies, fintech firms, tech cos, financial firms, or even telecoms.

3. But the biggest simplification is that your bank interacts only with the central bank through EXISTING ACCOUNT RTGS systems. The internal plumbing of CBDCs is GREATLY simplified. That is HUGE and why I suspect the Bank of Israel went with this system.

The INSURMOUNTABLE problems:

1. Convincing the public that they want an account at the central bank!

2. Convincing banks that they should sit idly by while AEs encroach on their territory!

3. Convincing central banks like China’s or India’s with 1.4 bn people that they should have peoples’ accounts! Good luck with that!

4. Proving that Sela's AE provides greater privacy than a bank would in a two-tier CBDC.

Thoughts?

👉TAKEAWAYS:

—Project Sela is tone-deaf! Citizens do not want a bank account with their central bank.

—Two-tier CBDCs, as in China, India, Europe, and the UK, all are token-based and strive not to have central bank accounts!

—Abandoning tokens for accounts rules out programmability. Think of this as a gov’t version of WeChat Pay or Alipay!

—Is this more private? No, and that is the biggest problem!

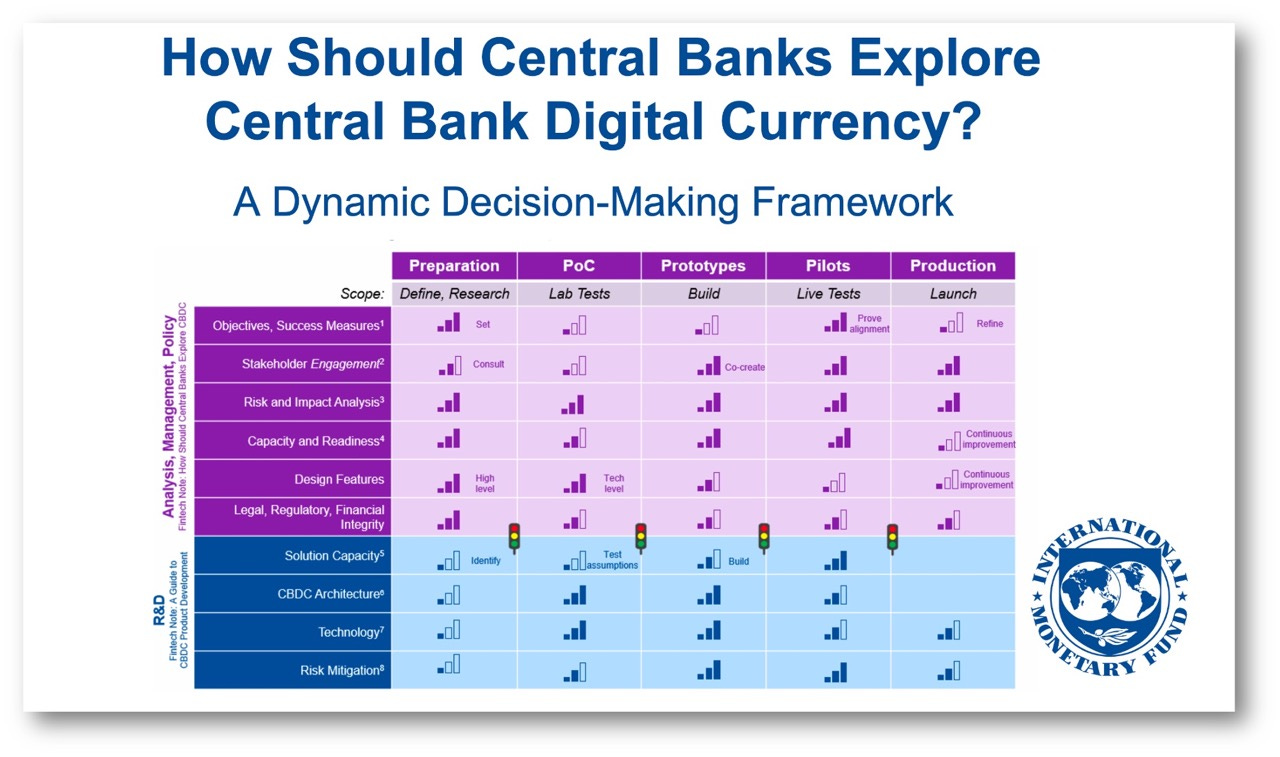

5. CBDC “5P” design framework

The IMF recognizes with CBDC “one-size does not fit all” and proposes the “5P” design framework.

"CBDC exploration and an eventual launch need to be jurisdiction-specific, depending on the degree of digitalization of the economy, the legal and regulatory frameworks, and the central bank’s internal capacity."

This fabulous paper was partly written by CBDC legend and friend John Kiff, who proposes a dynamic CBDC decision-making framework with the IMF team that helps central banks make successful decisions.

The paper proposes an original five-step approach called the “5P Methodology,” with each P being a “go/no go” point:

1. Preparation:

The preparation phase establishes the rationale and focus of the CBDC project and ensures sufficient resources to execute it. Key tasks are to define the policy objectives of CBDC, begin exploring the technology, and analyze the potential risks, design features, and success criteria

2. Proof-of-concept:

PoC is an empirical investigation to answer a question about how a potential aspect of CBDC could work in a simulated environment. The PoC phase resembles an empirical research process in which assumptions or hypotheses are subjected to testing to “find proof,” without committing yet to a specific approach that will later be used in a potential CBDC.

3. Prototypes:

The prototype phase marks the initial stage of developing the CBDC solution intended for eventual launch, contingent upon the decision to do so. A CBDC prototype can be defined as the first functional model of the CBDC, incorporating a technology solution and design features that closely align with the specified desiderata from earlier phases.

4. Pilots:

The pilot phase is the real-life testing of the CBDC prototype. It provides information on how well the prototype fulfills its requirements, how it can be improved, and ultimately whether the CBDC should move into the production phase through an official launch.

5. Production:

The production phase starts with the formal launch of the CBDC and covers its ongoing management and improvement.

Thoughts?

👉TAKEAWAYS:

—CBDCs are not “cookie cutter”. There is no standard design.

—5P presents a framework that helps central banks better understand if CBDC is the right choice.

—Kudos to John and the IMF!

Hey did you enjoy this? You know what to do!

My work is entirely supported by reader gratitude, so if you enjoyed this newsletter, please do both of us a favor and subscribe or share it with someone. You can also follow me on Twitter or Linkedin for more. For more about what I do and my media appearances, check out richturrin.com

Rich Turrin is the international best-selling author of "Cashless - China's Digital Currency Revolution" and "Innovation Lab Excellence." He is number 4 on Onalytica's prestigious Top 50 Fintech Influencer list and an award-winning executive previously heading fintech teams at IBM following a twenty-year career in investment banking. Living in Shanghai for the last decade, Rich experienced China going cashless first-hand. Rich is an independent consultant whose views on China's astounding fintech developments are widely sought by international media and private clients.

Please check out my books on Amazon:

Cashless: HERE

Innovation Lab Excellence: HERE