130 Countries exploring CBDCs; Banks want open access to digital platforms platforms say not so fast; Top 10 emerging technologies

"CBDCs are coming, like it or not."

1. 130 Countries exploring CBDCs

2. Banks want open access to digital platforms; platforms say not so fast.

3. Top 10 emerging technologies

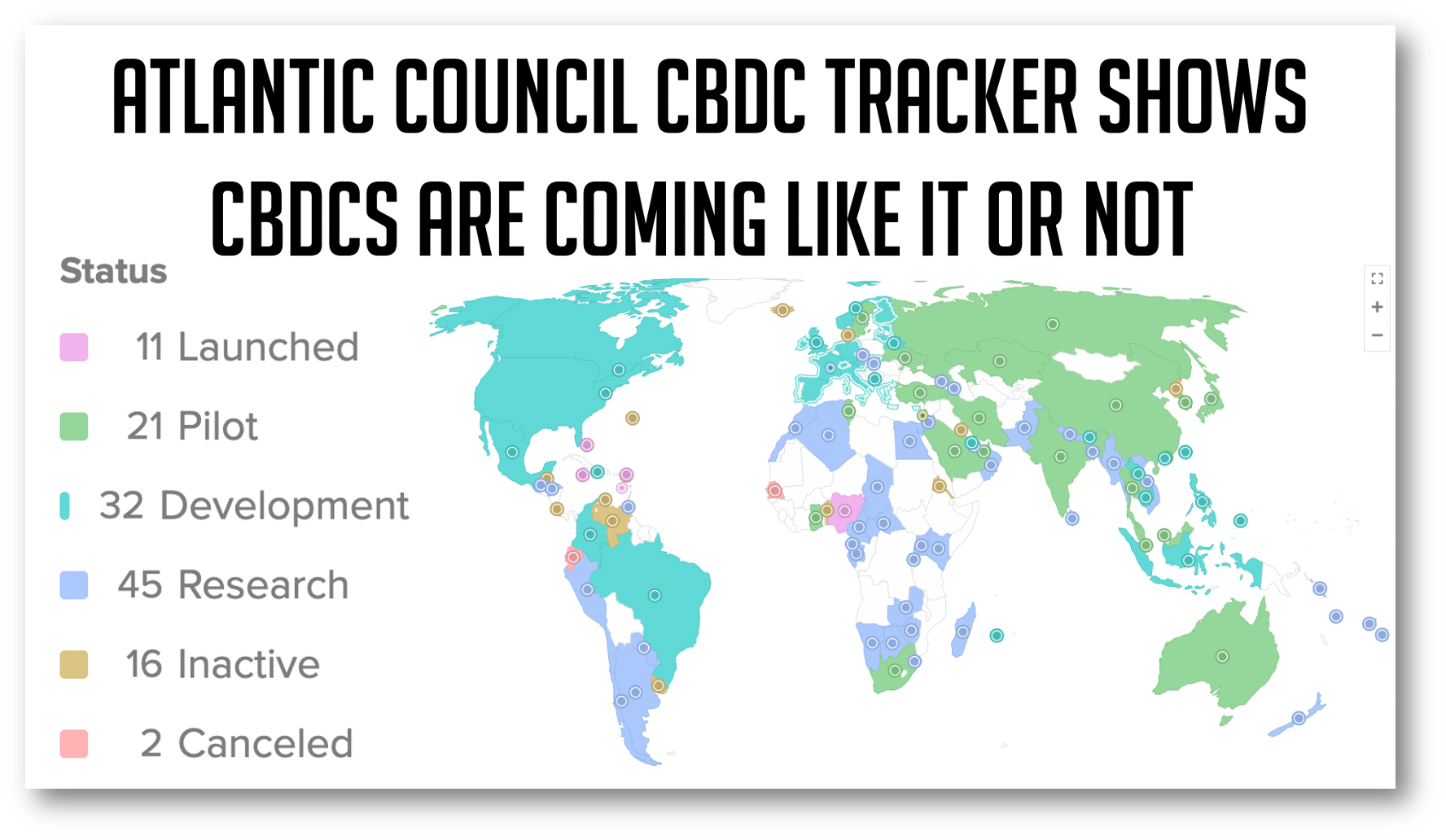

Today’s artwork: The Atlantic Council’s CBDC tracker just got a big update and is the picture of the week! I use the ominous subtitle of “like it or not” because CBDC is being savaged in the media and is now a front-and-center US election issue. Despite the undeserved bad press, I view the trend toward sovereign digital currency as unstoppable.

Please forgive any editing errors in this “Taiwan Edition” newsletter.

A special note of thanks to readers who have been sending me great PDFs throughout my long trip.

I am proud to be the No. 4 global fintech influencer on the prestigious Onalytica influencer list. I got there by writing solid articles that people like you want to read. This is the place if you want crystal clear, hype-free discussion on all CBDCs, fintech, crypto, and China’s tech scene. All my writing is backed up by my curation of the very best educational PDFs in the business. Subscribe, and you’ll be glad you did!

1. 130 Countries exploring CBDCs

CBDCs are coming whether you like it or not.

The Atlantic Council CBDC tracker recently got an update and 130 nations are now exploring CBDCs, with 64 moving to advanced phases.

These great video clips show how CBDC development is simply on fire. CBDCs are now a “hot-button” issue and have become a part of the US’s coming presidential election cycle, with some states going as far as banning CBDC usage. Someday it may be amusing to watch how they would legally enforce these bans if the US government ever decides to issue a retail CBDC.

The US is but one country, and while an important one, CBDC development on the global stage marches on with or without the US.

The Atlantic Council CBDC tracker can be found: here The above video shows the CBDCs according to phase of development and whether they are retail or wholesale versions. Note that this video is from Atlantic Council’s Twitter page. Tweets cannot be shown on Substack and vice-versa.

This videos from the Atlantic Council’s CBDC tracker page shows how in just 3 years the number of CBDCs under development went from 35 to 130.

Takeaways:

-CBDCs are coming “like it or not.”

-The need for a digital form of sovereign currency is clear; how best to deliver it is a worthy debate.

-Kudos to Atlantic Council for a great job on its CBDC tracker

Hey you, yeah you! Subscibe!

I know you want to…..

2. Banks want open access to platforms; platforms say not so fast.

Banks want better access to platforms with “three-sided marketplaces,” but platforms may have other ideas!

Download: here

Citi plunges banking into a “Brave New World” where instead of single banks supporting platforms, banks are given open API access to platforms as equal market participants.

This is a HUGE shift in how banks view their role on platforms!

Banks are currently forced to go out and strike proprietary deals with platforms. A good example is Amazon which partners with Chase for cards and Marcus for lending (among many others). A single partner for each banking function.

Citi proposes that “rather than viewing financial services as a ‘bolt on’, three-sided marketplaces will incorporate identity, payments, foreign exchange, lending, hedging, insurance, and the full gamut of trust-based financial services that will further accelerate the platform flywheel.”

Spinning banks’ flywheel

Such a system would also spin banks' flywheels as they would have access to the platform on set terms and tech standards. Make no doubt that Citi has its own self-interest in mind when suggesting that platforms open to banks.

Platforms will likely not be in a rush to make the conversion. Why would they when they can extract more value from banks and consumers by limiting their offerings!?

Benefits of a three-sided market:

🔹 Leverage customer due diligence

Utilize the trusted relationships financial firms have with their customers for identity verification, streamlining onboarding processes and bringing new levels of trust to transactions conducted on the platform.

🔹 Employ loyalty incentives

Platforms can collaborate with financial firms to offer exclusive discounts, rewards, or other value-added services that drive usage of the marketplace, customer loyalty and engagement.

🔹 Alleviate customer journey frictions

Leverage financial firms’ capabilities to enhance user experiences by facilitating rapid onboarding, instant payments, accessible lending, and providing peace of mind.

🔹 Encourage financial services firms to participate as buyers

Financial firms, as significant consumers of goods and services, can contribute to the platform’s growth by becoming active buyers.

Citi is asking platforms to help banks, a tough sell:

“Platforms can switch mindset and begin to consider financial firms as a new class of marketplace participant, equal in importance to producers and consumers."

🔥"Equal to consumers?" Citi didn’t just say that did they? 🔥

Yes, they did…and do you believe it❓

Thoughts?

Takeaways:

—Three-sided markets are coming but are still years off.

—Platform owners will not rush to open their platforms to banks when they can charge more for limiting access.

—More variety in bank providers is good for consumers.

—Citi has a tough job convincing platforms.

I’m using reverse psychology:

Don’t subscribe and miss out!

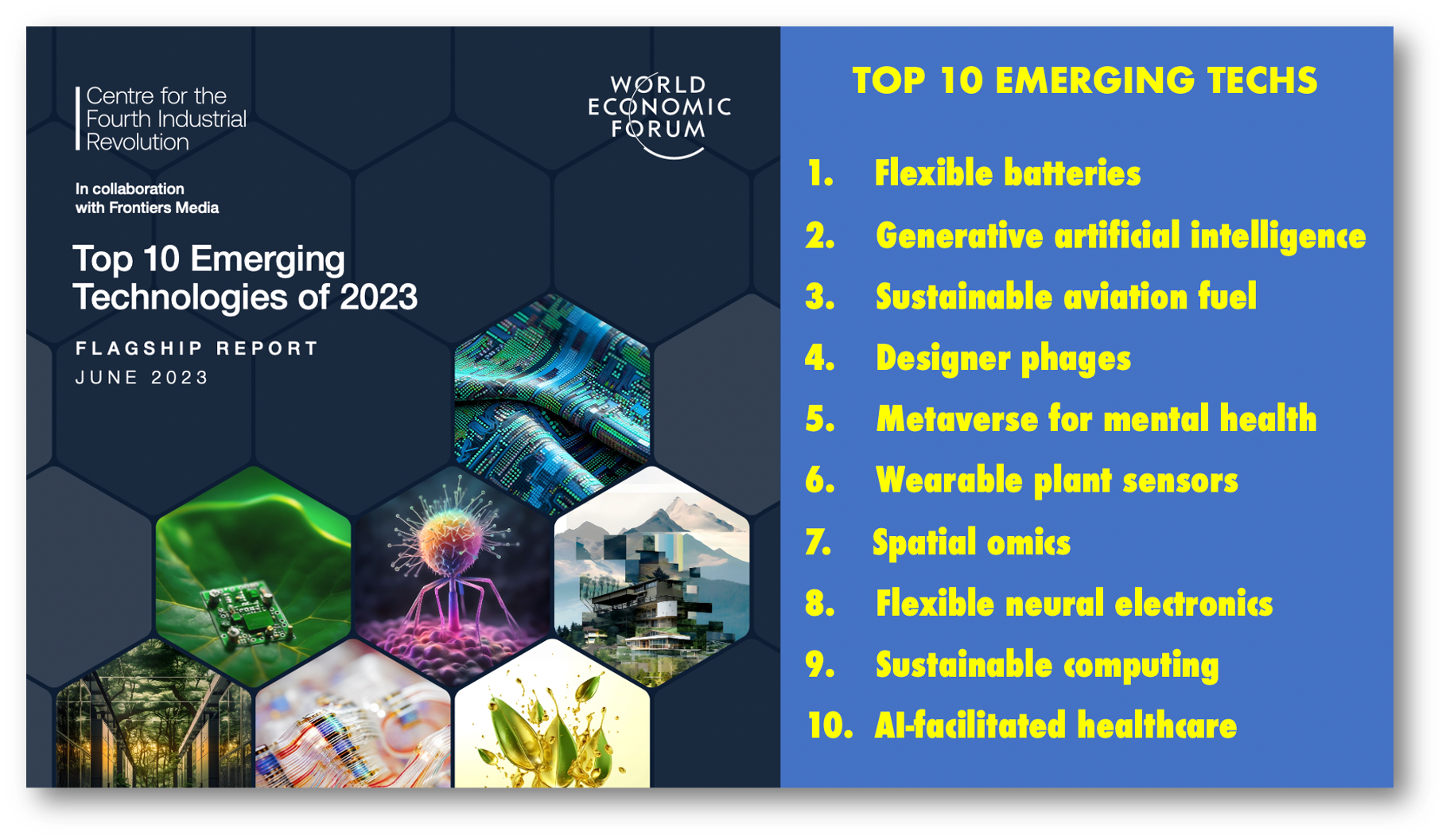

3. Top 10 emerging technologies

The TOP 10 emerging technologies YOU NEED TO KNOW and fintech isn’t on the list!

Download: here

The WEF looks at the Top 10 emerging technologies and comes up with a list with entries that go far above and beyond AI.

Fintech fans should take note that fintech doesn’t make the list, nor should it. The WEF is looking for emerging tech that may go exponential, and fintech is no longer “emerging;” it “emerged” long ago.

You should read this for the chapters with tech that you hadn’t imagined. For me, it was “designer phages” and “spatial omics” “ which lie far out of my area of expertise. Perhaps for you, the eye-opening tech will be different.

My last post on the WEF received more than a few comments that I was supporting “Davos Man,” and I even lost a few connections over the post. Not the first or last time this will happen. Several comments even went as far as to ask me to explain my support for the WEF, so I will.

For the record, I like -some- of the WEF’s research, and this report is a good example. If you want to unfollow me for liking high-quality WEF research like this, feel free. I also don't buy into conspiracy theories that the WEF is hell-bent on world domination.

The WEF’s Top 10:

Flexible batteries

Generative artificial intelligence

Sustainable aviation fuel

Designer phages

Metaverse for mental health

Wearable plant sensors

Spatial omics

Flexible neural electronics

Sustainable computing

AI-facilitated healthcare

So the real question is how does the WEF rank these techs:

A. People: Participants rated their expectations regarding each technology’s potential to enhance security and dignity.

B. Planet: Participants gauged the extent to which they envisage the technologies could help protect and restore our planet.

C. Prosperity: Survey respondents were asked to evaluate the potential of each technology to improve the quality of life for individuals worldwide.

D. Industry: Participants assessed the potential of these technologies to disrupt existing industries and generate new markets over the next decade.

E. Equity: Finally, the survey asked participants to rate the potential for these technologies to promote global societal equity.

Thoughts?

🔺Hit like and comment now! One comment equals 10 likes!

Takeaways:

—The WEF’s list of “emerging tech” is a great read and shows AI isn’t the only game-changer

—Is this list an example of “Davos Man” taking over? Perhaps the “Designer Phages” are programmed?

—Fintech is tech that has already emerged.

—GenAI and sustainable computing will be game-changers for fintech.

Subscribing is the only logical course of action.

And share with your colleagues because:

"The needs of the many outweigh the needs of the few or the one."

My work is entirely supported by reader gratitude, so if you enjoyed this newsletter, please do both of us a favor and subscribe or share it with someone. You can also follow me on Twitter or Linkedin for more. The best way to ensure you see the stuff I publish is to subscribe to the mailing list here on Substack, which will get you an email notification for everything I post.

Everyone, including platforms that disagree with me, has my permission to republish, use or translate any part of this work or anything else I’ve written (except my books) with credit given to me and this site (richturrin.substack.com) free of charge. For more info on who I am, what I do, and where I’m going, check out richturrin.com

Rich Turrin is the international best-selling author of "Cashless - China's Digital Currency Revolution" and "Innovation Lab Excellence." He is number 4 on Onalytica's prestigious Top 50 Fintech Influencer list and an award-winning executive previously heading fintech teams at IBM following a twenty-year career in investment banking. Living in Shanghai for the last decade, Rich experienced China going cashless first-hand. Rich is an independent consultant whose views on China's astounding fintech developments are widely sought by international media and private clients.

Please check out my books on Amazon:

Cashless: HERE

Innovation Lab Excellence: HERE

You mentioned that you see the inevitability of a national digital currency. One of my biggest concerns is how the currency will be utilized in the trading of stocks. I am not referring to crypto stocks but rather our trading being conducted with digital currency.

The government could very well (and most likely will ) put a micro second delay on the transaction and control the market. Another that could be as dangerous, if not more dangerous, is their ability to determine trading patterns. The one assumption I am making (and it’s valid) is that the government will never lose control/contact of digital currencies... meaning they will have complete and total control over digital assets.

It would be foolish if the government had the ability to do this and not do it... control that is.

If we do a 100% conversion we will lose our privacy right along with it. Our Constitution protects from unwarranted surveillance; how can the laws be manipulated to accommodate the need for 100% touching the currency?