Moody's: Tokenization is Here, Intermediaries Aren't Going Anywhere

Moody's picks fintech and asset managers as tokenization's biggest winners

I post daily, but deliver to your inbox every Sunday. Browse past newsletters HERE. Book Rich. Bring the speed of Asia to your next event HERE

Read me first

Tokenization will bring winners and losers, but the crypto dream of cutting out intermediaries is still just that: a dream.

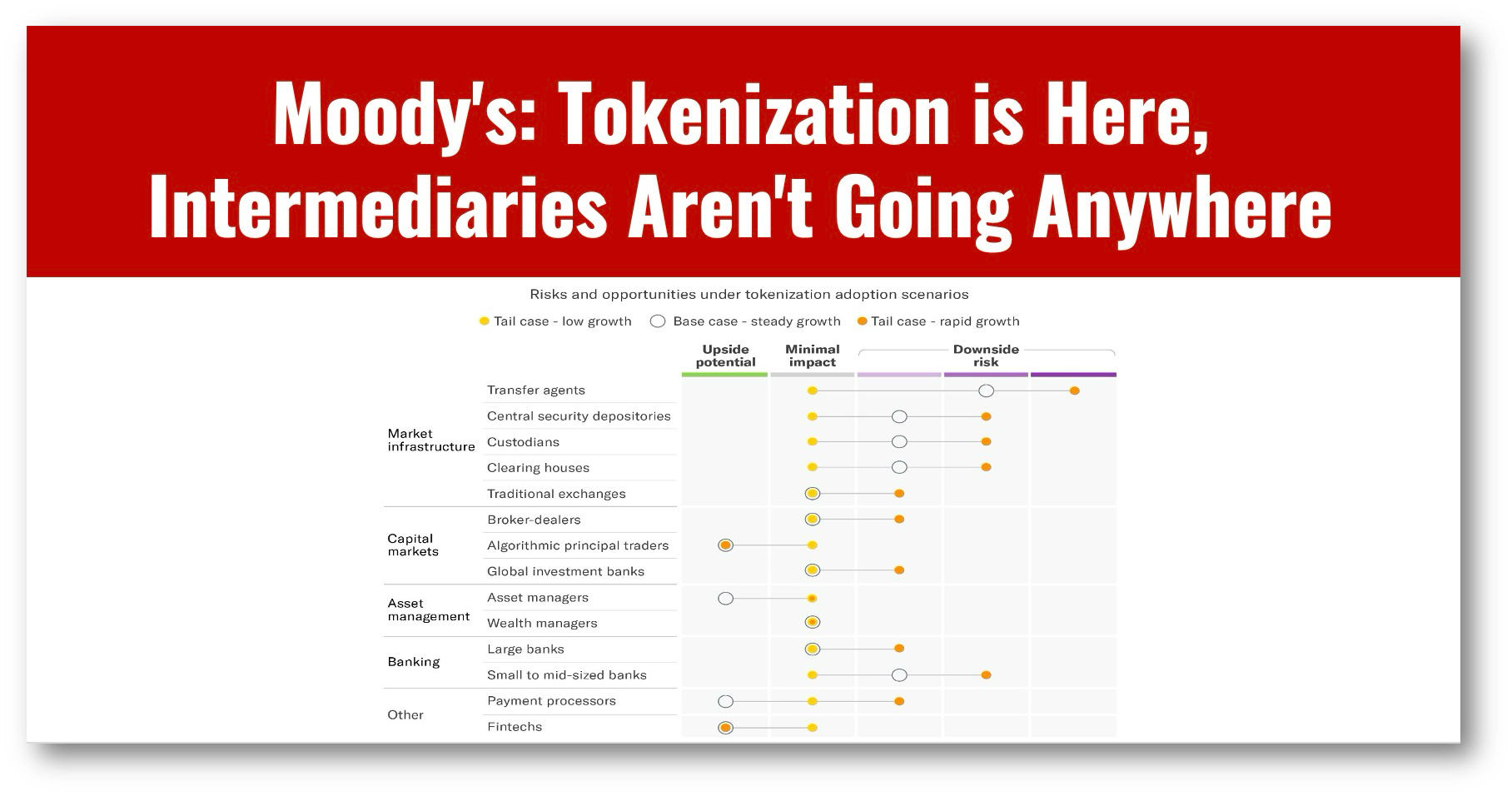

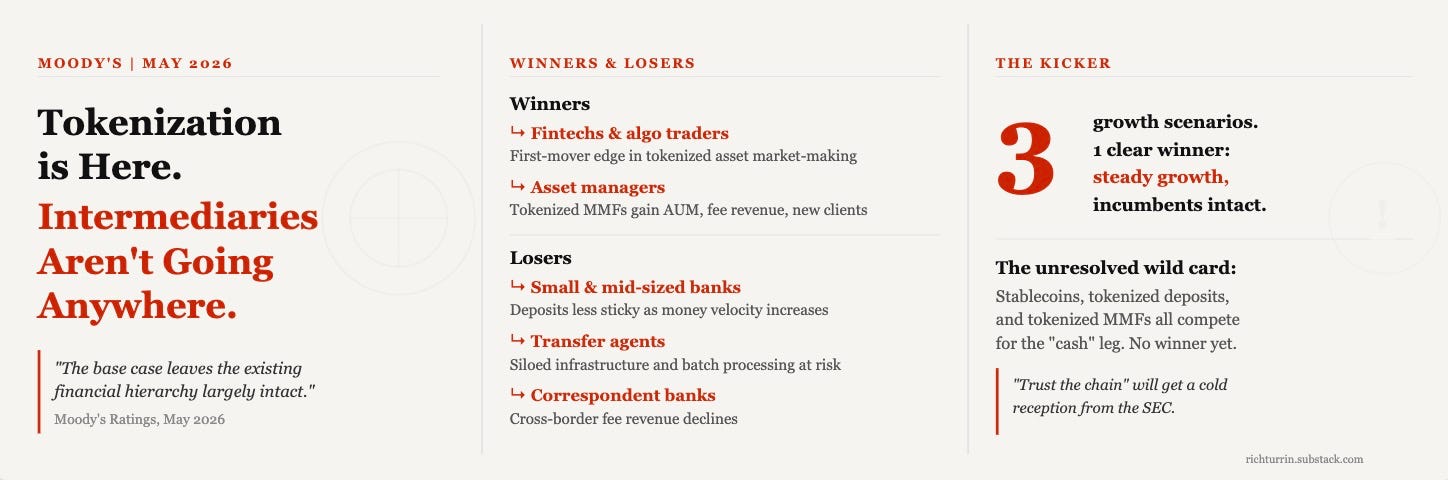

Moody’s sector report maps three growth scenarios for real-world asset tokenization. The base case, considered by far the most likely, leaves the existing financial hierarchy largely intact.

The irony is hard to miss: the DTCC, NYSE, and Nasdaq are moving to tokenization precisely to protect their intermediary roles, not disrupt them. (see below)

The SEC’s decision this week to delay a dedicated sandbox for tokenized stocks, citing industry concerns over investor protection and market integrity, shows how intermediaries still know how to fight back.

The reason this matters is that, as I wrote last week, tokenization is adopting crypto’s technology but not its libertarian sentiment.

The biggest winners Moody’s identifies:

↳ Algorithmic principal traders and Fintechs, with first-mover advantages in tokenized asset market-making

↳ Asset managers, particularly tokenized money market funds and short-duration liquidity products, gaining AUM and new client bases

The biggest losers? Predictably, the ones who never move fast enough.

↳ Small- to mid-sized banks, whose deposits could become less sticky as money velocity increases

↳ Legacy transfer, reconciliation, and post-trade functions — the ones still running on siloed infrastructure and batch processing, such as transfer agents

That small and mid-sized banks get squeezed while global giants don’t shouldn’t be a surprise. Smaller institutions lack the resources to build digital asset services, and deposits will migrate elsewhere.

The wild card in Moody’s analysis that is still unresolved is what the settlement asset will be.

Stablecoins, tokenized deposits, and tokenized MMFs are all competing for the “cash” leg of tokenized trades. So far, even Moody’s won’t pick a winner as all lack the universal acceptance of plain old cash.

This is exactly why CBDCs are so convenient, before Washington decided to make them illegal.

So is the “disintermediation” narrative oversold?

The potential for cost savings through disintermediation is real, but so are the reasons the intermediaries exist.

Moody’s states that going on-chain doesn’t eliminate the need for governance, compliant ownership records, identity controls, interoperability, and legal finality.

So far, these remain in the control of market intermediaries, regardless of how much goes on-chain.

The securities industry won’t go down without a fight, and anyone proclaiming to simply “trust the chain” will get a cold reception from the SEC and the intermediaries they regulate.

Suggested Reading

HAND CURATED FOR YOU

🚀 Asia moves fast. So does this newsletter. I curate only the best fintech, CBDC, and AI insights from 50+ sources weekly so you stay ahead of what’s coming West. Subscribe and never fall behind.

If you know someone who would like this newsletter, please share it with them and help grow our Asia, CBDC, and AI aficionados community!