Tokenized Securities Settlement: Speed Kills

Corporate AI governance is a sham, and 89% of your bank customers are one tap away from leaving

Thanks for reading the “Cashless” newsletter, an insider’s view on Asia’s fintech, CBDC, and AI for anyone serious about “the Asia Century.” I’m Rich Turrin, and these are my hard-hitting insights designed to help you — whether you’re in finance, tech, or consulting — stay ahead of the pack. Free is great. Premium is your unfair advantage.

Topics:

Tokenized Securities Settlement: How Fast is Too Fast? (part 1 of 2)

It’s natural to think that the instant settlement made possible by tokenization is best, as though faster is always better. This article makes the case that T+0 settlement isn’t always optimal and that slower T+1 or T+2 can reduce liquidity spikes. This article by OMFIF introduces the concept and is Part 1; now go to Part 2 below for the IMF’s perspective.

Tokenization: Speed Kills, Without Global Interoperability (part 2 of 2)

The IMF looks at tokenization and warns that without global interoperability, faster just means less time for regulators to pump the brakes. The IMF looks at settlement speed but goes further to discuss whether stablecoins, wCBDC, or deposit tokens should be the settlement currency.

Bank Customer Loyalty is Dead: 89% of Your US Customers Are Ready to Walk, 76% Global

89% of US bank customers are ready to walk, and the only thing keeping them is friction. Asia already proved what happens when you remove it: instant payments, frictionless account opening, and loyalty that evaporates overnight. That world is coming to the West. Once the friction is gone, retention lasts exactly as long as it takes to hit send on a cash transfer app.

AI Governance is a Sham: 87% Don’t Even Bother (part 1 of 2)

This article has only one purpose, and that is to call out the sham that is corporate AI governance, where 87% of companies don’t even bother. Organizations are deploying the most powerful technology in a generation with zero guardrails and calling it strategy. The lawsuits are coming, and so is the reckoning for every board that tries not to accept responsibility for AI.

AI Governance Is Broken: 60% Use Shadow AI (part 2 of 2)

As an accompaniment to the article above, we have a report that shows just how broken AI governance really is. 60% of workers are now using an AI that they bring from home with work data, a liability bomb waiting to go off.

Dive into the Knowledge Vaults — Start with a Free Read

Chart of the day: Economies Most Dependent on Remittances

Happy Sunday!

In all my years of writing, I’ve never had two two-part articles in a single newsletter, so enjoy the extra coverage on tokenization and AI governance. Two topics I never tire of, and this week we got double helpings of both.

Thanks for reading — whether free or paid, I’m grateful you’re here. 🚀

Rich

Tokenized Securities Settlement: How Fast is Too Fast? (Part 1 of 2)

Why T+1 or T+2 with on-chain DvP beats instant settlement

Faster isn’t always better when it comes to settling securities.

A 2024 survey of bond market participants found only 16% preferred instant T+0 settlement, while 84% favored a longer cycle.

Instant settlement eliminates the netting mechanisms that keep today’s system capital-efficient, strains liquidity, and creates FX hedging nightmares for offshore investors.

See why on-chain T+1 or T+2 is the smarter path forward for tokenized markets.

Tokenization: Speed Kills, Without Global Interoperability (Part 2 of 2)

The IMF’s concerns about tokenization go beyond the hype

Tokenization promises to make finance faster, but not necessarily safer.

The IMF warns that without global interoperability, speed creates new dangers: automated margin calls can trigger cascading liquidations before any human can intervene, settlement lags that currently act as liquidity buffers disappear, and smart contract errors can propagate instantly.

Fragmented platforms could trap liquidity in digital silos, and emerging economies face currency substitution risk.

Take a look at the IMF’s sobering reality check on tokenized finance.

Bank Customer Loyalty is Dead: 89% of Your US Customers Are Ready to Walk, 76% Global

Good news: your customers want to share their data. Bad news: not with you.

Bank customer loyalty is eroding fast. A Mastercard survey of 8,000 consumers across 11 markets found that 76% are ready to switch financial providers for better digital features, and 44% already have.

In the US, that number jumps to 89%. Customers want to share their data for better rates and personalization, just not necessarily with their current bank.

We examine just how bad the problem is and why it will only get worse when AI-driven neobanks like Revolut and Nubank move in.

AI Governance is a Sham: 87% Don’t Even Bother (Part 1 of 2)

The wake-up call will cost billions. And it’s coming.

Corporate AI governance is largely theater, and the numbers prove it.

A Thomson Reuters / UNESCO survey of nearly 3,000 companies found that 87% haven’t committed to any AI governance framework, 97% have no record of what AI they’ve even deployed, and 84% have nobody accountable when their AI causes harm.

I argue that only one thing will force companies to take governance seriously: a catastrophic failure with a billion-dollar price tag.

AI Governance Is Broken: 60% Use Shadow AI (Part 2 of 2)

Using your home AI on private work data is the new normal

Shadow AI is now the workplace norm, and it’s a liability crisis hiding in plain sight. A LexisNexis survey of 1,400 professionals found that 60% are using personal AI tools at work, 53% without formal approval, and 28% work somewhere with no AI policy at all.

Crucially, the blame lies with leadership, not employees. We explain why restrictive policies and a lack of approved tools are driving the problem, not reckless workers.

Dive into the Knowledge Vaults — Start with a Free Read

Knowledge Vaults are your curated edge across five high-impact themes: AI, banking, CBDC/tokenization/payments, stablecoins, macrotrends, and Asia.

Every resource inside is hand-picked with only the highest-quality, most valuable material I uncover, no filler.

These vaults are living documents, updated weekly and growing fast.

This week, the 2026 Macro Forecasts & Trends Vault in focus:

ARK Invest, Visa, Stanford, Plaid, and BDO all dropped major research this cycle, and there’s a clear through-line: the structural shifts in AI, payments, and financial infrastructure aren’t on the horizon anymore. They’re underway.

Stablecoins on Visa’s strategic priority list. AI agents executing payments without human approval. Fraud overtaking delinquency as lenders’ top risk. Tokenized assets are opening up private markets. Stanford mapping ten converging technology fields with geopolitical implications. These reports give you the data and the framing to make sense of what’s moving and why.

Premium members get all five in the Knowledge Vault — plus everything we add going forward.

🔓 Free Vault Read

To show you what’s inside the vaults, here’s an example that’s yours to read, free.

Consider this your preview. Inside The Knowledge Vault, every vault is stacked with reports like this one, curated, current, and built to give you an edge. One subscription. Every vault. Unlimited reads and downloads.

Read it free. Download it and everything else with a premium subscription. Then decide if you can afford not to have access.

Chart of the Day!

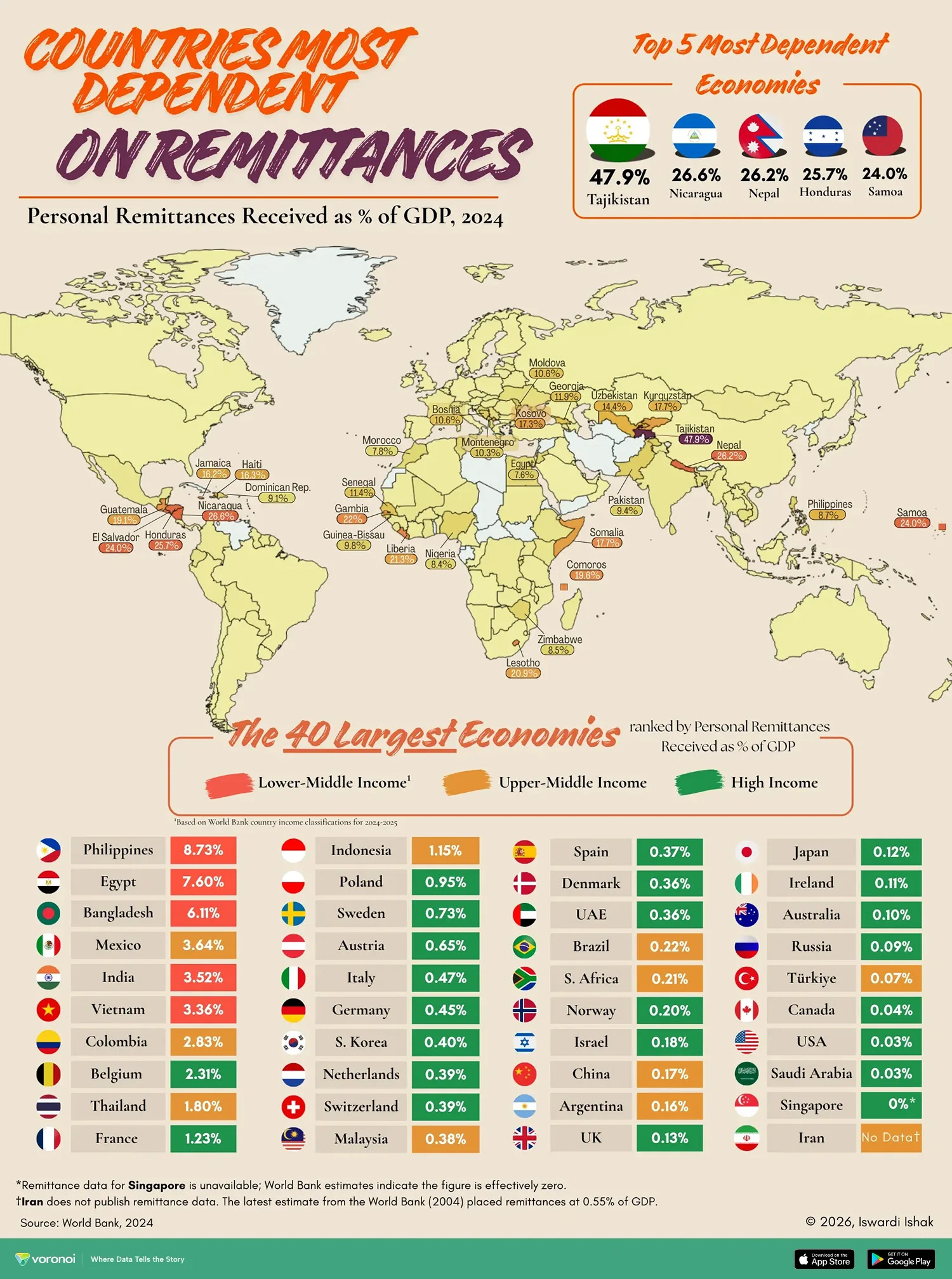

Economies Most Dependent on Remittances

Key Takeaways

Tajikistan is the world’s most remittance-dependent economy, with inflows equal to 47.9% of GDP in 2024.

Several smaller economies rely on remittances for a quarter or more of GDP, including Nicaragua, Nepal, Honduras, and Samoa.

By comparison, the global average is just 0.82%, showing how concentrated remittance dependence is.

Remittance dependence is highest in smaller or lower-income economies where a significant share of the workforce migrates abroad. The money sent home supports household spending, education, housing, and basic consumption, giving remittances an outsized role in the domestic economy.

Larger economies like India and Mexico have massive remittance inflows in absolute terms, but remittances are a smaller part of GDP. Large economies have more diversified sources of income, diluting the relative impact of remittances.

The cost of sending these remittances represents a tax on some of the world’s poorest workers. The global average cost for sending $200 in remittances was 6.49% in Q1 2025, according to the World Bank, meaning about $13 on a $200 transfer.

The G20 Cross-Border Payment Roadmap is designed to decrease these costs but has had limited success in actually reducing fees. In fact, they haven’t gone down in several years.

This leaves the world’s poorest households funding a remittance industry valued at $121 billion in revenue in 2025, projected to nearly double to $270 billion by 2034.