Yuan Rising? Where there's smoke there's fire with BRICS new payment system and the PBOC's new Yuan Pool.

Financial inclusion increasing with China's past tied to payment success

This week:

1. BRICS new payment system

2. China’s yuan pool pushes back against the dollar

3. Yuan Rising? Where there’s smoke there’s fire

4. China’s past and payment

5. Financial inclusion improving

1. BRICS new payment system

BRICS nations are looking at building a parallel payment system to counter US dollar hegemony and CBDCs are likely part of the plan.

This story didn’t get a lot of play in the Western media, in fact, the BRICS meeting was pretty much ignored in my news feeds.

Two solid articles on this topic are: SCMP: Here and from ING: Here

The key statement came from none other than Russia’s Putin himself:

“The issue of creating an international reserve currency based on a basket of currencies of our countries is being worked out.”

The BRICS also issued a communication that said that:

“It was working on setting up a joint payment network to cut Reliance on the Western financial system. The BRICS countries have been also boosting the use of local currencies in mutual trade.”

I don’t blame you if you think this is never going to happen or will simply be too small to bother with.

There are, however, three problems with thinking that:

1️⃣ BRICS nations have talked about this since 2019, so it isn’t solely a response to sanctions. It's part of a deeper desire for monetary independence and the savings of using native currencies over the dollar.

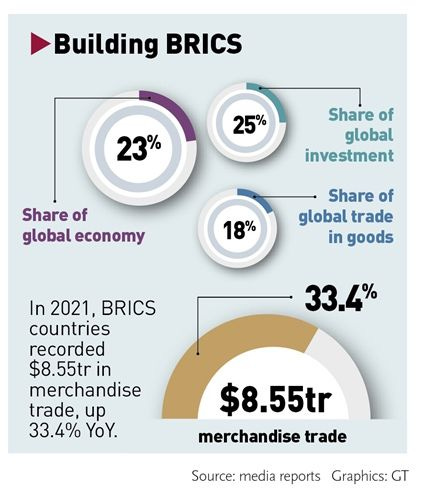

2️⃣ BRICS make up 23% of the global economy and 25% of global investment. To simply write them off as too small to be bothered seems short-sighted. That is one of the reasons they formed the BRICS alliance in the first place!

3️⃣CBDC! By next year Russia, China and India will all have working CBDCs. South Africa and Brazil are also in advanced stages of development. Tell me this isn't a perfect use case for a CBDC? I know some may think this preposterous, but I think all of these nations have everything to gain and nothing to lose by trying.

That this story got no news coverage was to me also interesting. The BRICS meeting was given the “royal treatment” in the Chinese press but nothing in the West and only one article in the venerable Wall Street Journal!

Takeaway

That nations representing 23% of the world economy want to reduce dollar use is nothing to take lightly. All are key contributors to the global economy and you can’t blame them for wanting to manage their risk from sanctions.

That it wasn't well covered in the news also speaks volumes!

I have said before on these pages that sanctions are a double-edged sword that cuts both ways. There is a cost to the US for using them and motivating nations to avoid the dollar is certainly expensive even if the impact is not immediate.

Who knows what the BRICS will come up with but what if they form a new BRICS digital currency trading mechanism?

If the BRICS nations do, and it won't be overnight, then the old expression, "Revenge is a dish best served cold," would seem to fit!

2. China’s yuan pool pushes back against the dollar

China sets up a liquidity facility with the BIS to promote RMB use with local partners in a small but significant move against dollar hegemony.

Download press release: Here Excellent South China Morning Post article: Here

Rome wasn’t built in a day and no doubt that People’s Bank of China looks at its struggle to reduce dollar dependence as a long-term project. Remember, when China thinks “long-term” they mean it!

Facility participants are central banks from Indonesia, Malaysia, Hong Kong, Singapore, and Chile and the purpose of the reserve is to ensure that none of the central banks can run short on RMB due to market volatility.

This “liquidity arrangement” is nothing more than a rainy day fund with each participant contributing RMB 15bn (US$2.2 bn) to the fund which they can borrow against or drawdown.

The US Fed in a related but different mechanism runs “liquidity swap lines” to ensure that there are no international shortfalls in dollars that create market disruption.

The reserve will not miraculously increase RMB use. What it will do is make using the RMB more convenient as it removes the need for central banks to tightly monitor or restrict RMB use. Any shortfalls can be taken from the reserve.

1️⃣ The countries participating are all regional players which supports my view in Cashless that before the RMB goes global, it will go local first becoming a “regional reserve currency.”

2️⃣ This facility is a direct result of US sanctions on Russia which according to some circles surprised China’s PBOC with their severity and reinforced China’s resolve to promote the RMB.

3️⃣ “Sanctions have disrupted the global financial order … and they will accelerate de-dollarisation,” Citic Securities, a leading Chinese investment bank, wrote in its midyear outlook last week.

4️⃣ Watch also that China has signed currency swap agreements with 40 countries, in an attempt to internationalize the yuan.

5️⃣ Don’t be surprised when these countries also wind up first on the list for using the digital yuan! Indonesia in particular has been vocal about increasing RMB use.

Takeaway

Many will look at this and say “the RMB is only 2.79% of global FX reserves and there is nothing to fear.

Short-term, you’re correct none of this provides the RMB with a magic bullet.

Long-term, you might be in for a surprise with the growing use of RMB in BRI and RCEP countries.

The RMB is likely to become a key regional currency and the digital yuan will contribute to this effort.

Evidence for this transition comes from nations like Indonesia and Malaysia who are vocal about wanting to use fewer dollars.

If China can help them do that by making the RMB easier to use it will be a win for all.

3. Yuan Rising? Where there’s smoke there’s fire

Long-form article!

Where there’s smoke there’s fire, as the Chinese yuan is used in a major cross-border trade deal the IMF and central banks note a shift, as sanctions give a boost to internationalization.

For the full article go: Here on Substack

The use of Chinese yuan in a cross-border India-Russia trade deal for coal is an interesting story but it’s only one part of an accumulation of stories that have piqued my interest as they signal a changing role for the yuan………….

4. China’s past and payment success

China’s societal values open a window to understanding its success with digital yuan and Alipay+ today.

Link to Any Mok’s article “Looking to China and India’s Past for Future Success”: Here

I am honored to be featured in this beautiful article in Wharton Magazine written by Andy Mok, senior research fellow at the “Center for China and Globalization.”

He writes: “Traditional strategic thought in China has always emphasized the avoidance of direct conflict precisely because such conflict is wasteful and destructive.”

Andy then goes to show two real cases in payments where this “avoidance of conflict” is real.

1️⃣ Digital yuan:

“In his book Cashless: China’s Digital Currency Revolution, Richard Turrin weaves together monetary policy, Chinese political history, technology, and an understanding of the global payments system to... ...foretell a profound change in the relationship that people, companies, and governments around the world will have with money.”

🙏Thank you Andy!

The key to the e-CNY is that by launching the digital currency China is not trying to mount a frontal attack on the dollar. The concept of “avoidance of direct conflict” is present even here. The digital yuan is not trying to take on the dollar in a costly slugfest it would likely lose.

Instead, China is subtly trying to offer a dollar alternative based on utility: “E-CNY is an entry token to a new digital logistics system the likes of which the world has never seen.”

China is tying together payments and logistics, to provide a new value proposition for payment that the US can do little to counter.

Certainly, the US can try to dissuade nations from using e-CNY, but how to respond when users simply say that by using e-CNY they get their goods faster?

2️⃣ Alipay+

Here again, Andy points out that “ Ant Group has adopted a distinctively traditional Chinese approach in its strategy to expand globally.” Alipay isn’t taking on native payment providers in their own markets, which would lead to “marketing battles and collateral damage.”

Instead, Alipay+ is setting itself up as a helpful and non-competitive systems integrator capable of providing global connectivity for payment systems that are highly regional.

Again as with the e-CNY, we see an avoidance of conflict by changing the value proposition. There is no conflict with regional mobile wallets because who else can build a QR code international mobile wallet transfer system?

Takeaway

Much of our analysis of new fintech relies on technical specifications or capabilities. These metrics are useful but don’t tell the whole story.

What is missing is some consideration for the culture behind it.

Culture matters, even in tech.

5. Financial inclusion improving!

The World Bank Findex survey shows progress is being made in financial inclusion although we have a long way to go with 1.4 billion unbanked!

Globally, in 2021, 76 percent of adults had an account at a bank or regulated institution. Download the Global Findex Database: Here

Fintech desperately needs some good news! Crashing crypto markets and falling fintech unicorn valuations are in the news daily and make for hard reading.

The World Bank's Global Findex Database delivers good news!

Great progress in financial inclusion:

🟢 Globally, 76% of adults had an account, with account ownership increasing by 50% in the 10 years with most gains attributable to digital access

🟢 71 % of adults in developing economies now have a formal financial account, compared to 42 % a decade ago

🟢 The gap in access to finance between men and women in developing economies has fallen from 9 percentage points to 6.

🟢 Mobile money has become an important enabler of financial inclusion in Sub-Saharan Africa—especially for women. 55% of adults had an account, including 33 % with a mobile money account

🟢 The share of adults making or receiving digital payments in developing economies grew from 35 percent in 2014 to 57 percent in 2021,

Lots more work to do:

🔴 Globally, about 1.4 billion adults are still unbanked

🔴 54% of the unbanked—740 mn people—live in only seven economies: Bangladesh, China, Egypt,India, Indonesia, Nigeria & Pakistan

🔴 Women, along with the poor, are more likely to lack identification or a mobile phone, to live far from a bank branch, and to need support to open and effectively use a financial account. (see India below on ID)

🔴1-in-5 adults in developing economies who receive a wage payment into an account paid unexpected fees on the transaction.

🟡 more than one-third of adults in developing economies who paid a utility bill from an account did so for the first time after the start of the COVID-19 pandemic—evidence of its impact on digital adoption

India and China:

🟡 China and India claim large shares of the global unbanked population (130 mn and 230 mn, respectively) because of their size

🟡 Between 2011 and 2017 growth in account ownership was focused mainly in China and India, India 35-79%; China 63-79% of the population got accounts.

🟡 In India, account ownership more than doubled in the past decade, from 35% in 2011 to 78% in 2021. Due in part to a policy launched in 2014 that leveraged biometric identification cards to boost account ownership among unbanked adults.

🟡 In China, 82%of adults made a digital merchant payment in 2021, including over 100 mn adults (11%) who did so for the first time after the start of the pandemic.

Solutions:

Expand financial inclusion through better access to formal identification and mobile phones.

But phones alone are not the answer even with high mobile penetration people remain unbanked.

For example, half of the unbanked adults in South Asia and Sub-Saharan Africa have a mobile phone!

Education is the missing link, in that mobile users need to be taught how to use financial services so that they feel confident in their abilities.

Thanks for reading

Be in control of your future, subscribe!

More of my writing, podcasts, and media appearances here on RichTurrin.com

Rich Turrin is the international best-selling author of "Cashless - China's Digital Currency Revolution" and "Innovation Lab Excellence." He is an Onalytica Top 100 Fintech Influencer and an award-winning executive previously heading fintech teams at IBM following a twenty-year career in investment banking. Living in Shanghai for the last decade, Rich experienced China going cashless first-hand. Rich is an independent consultant whose views on China's astounding fintech developments are widely sought by international media and private clients.

Please check out my books on Amazon: