The US-EU Digital Money Split: Two Incompatible Standards, One Bill We All Pay

On the same day the EU advanced the digital euro, the US banned CBDC research until 2030.

Book Rich. Bring the speed of Asia to your next event HERE

Thanks for reading the “Cashless” newsletter, an insider’s view on Asia’s fintech, CBDC, and AI for anyone serious about “the Asia Century.” I’m Rich Turrin, and these are my hard-hitting insights designed to help you — whether you’re in finance, tech, or consulting — stay ahead of the pack. Free is great. Premium is your unfair advantage.

Topics:

The US and EU’s Digital Money Split Will Cost Us All

Tokenization and AI Won’t Kill the Middleman: The Casino Always Wins

Stablecoin Yield: Crypto Exchange Disclosures Are Nearly Criminal

WEF: Banks Are Measuring AI ROI With One Number They Need Four

AI-First: Impermanence by Design

Dive into the Knowledge Vaults — Start with a Free Read

Chart, Art and Sponsor of the Day — Tether: 100 Employees, No Audit, and More U.S. Debt Than Most Nations. What Could Go Wrong?

Happy Sunday,

I’ve been watching fintech long enough to know when a week is telling you something. This was one of those weeks, and the message was fragmentation, quietly killing the narrative that our tokenized, AI-powered future will arrive smoothly and serve all.

On the same day the EU advanced the digital euro, the US banned CBDC. I facepalmed. Not because it was surprising, but because it confirmed what I’ve been watching build for months. The West isn’t slowing down on digital finance. It’s fragmenting into two incompatible visions of what digital money should even be.

When financial markets fragment, the resulting goods and services always cost more.

That’s the thread this week. Clearinghouses were supposed to be made obsolete by tokenization. Instead, a fragmented landscape of competing chains and incompatible standards keeps them indispensable. Maintaining tokenized and traditional platforms costs more.

Banks know what AI demands, but most aren’t doing it, fragmenting the market into haves and have-nots. Stablecoins promised a new paradigm and delivered misleading disclosures that are nearly criminal, fragmenting users into the informed and the exposed, who one day may pay dearly.

The disruption narrative took a beating this week. Fragmentation is the story, and I expect more of it, not less.

Thanks for reading. I’m grateful you’re here.

Rich

P.S. You read it, I write it. If there’s a topic I’m missing or a report I ought to know about, tell me. The best ideas come from readers.

The US and EU’s Digital Money Split Will Cost Us All

On the same day the EU voted to advance the digital euro, the US banned CBDC.

On the same day the EU voted to advance the digital euro, the US buried a four-year CBDC ban inside a housing bill. The timing is stunning. The EU wants out of Visa and Mastercard dependency, with a digital euro pilot launching Q3 this year and a full rollout in 2029. The US, meanwhile, is blocking even wholesale CBDC research. Two of the world’s biggest trading partners are now on diverging payment rails, and we’ll all pay for it.

Yours Free — For Now

This one is free for now, but it goes behind the paywall later this week. It’s too important not to share. If you’ve been curious about what premium gets you, this is exactly the kind of tight analysis waiting for you on the other side.

Tokenization and AI Won’t Kill the Middleman: The Casino Always Wins

Technology changes but the grip of exchanges and clearinghouses on markets doesn’t.

Everyone said tokenization would kill the middleman. Put assets on a blockchain, automate settlement, and goodbye clearinghouse. Wrong. The Oliver Wyman Global Market Infrastructure Report shows that only 5% of FMI revenue gets structurally eliminated. The casino always wins. AI makes it worse: it pushes FMI profit margins from 54% to 63% while generating $9 billion in new revenue. Turns out, no one owns market data like the DTCC and CME. Technology changes. The house doesn’t.

Stablecoin Yield: Crypto Exchange Disclosures Are Nearly Criminal

Exchanges have quietly redefined “earn” and “principal protection”

Crypto exchanges call it “earn.” They call it “principal protected.” Neither means what you think. New BIS research exposes two completely different yield products hiding under the same label on Coinbase and Binance, with radically different risk profiles. And “principal protection”? That means token quantity, not dollar value. Gemini Earn users learned this the hard way when Genesis collapsed and their holdings became unsecured bankruptcy claims. The disclosures are nearly criminal.

Why This One Is Behind the Paywall

This is the kind of analysis you won’t find anywhere else. I read the fine print so you don’t have to, and what I found in those exchange disclosures should make every stablecoin holder uncomfortable. Go Premium, your unfair advantage starts here.

WEF: Banks Are Measuring AI ROI With One Number They Need Four

Human-AI collaboration? How many humans are needed is the question.

Banks measure AI ROI with one number: how many jobs can we cut? The WEF says that’s wrong and you need four. Three of them are non-financial. Consider that 73% of banking employees’ time could be affected by AI, yet only 19% work in teams that experiment with it together. The real ROI question banks aren’t asking: what happens when AI agents start sweeping deposits to competitors automatically? That number may be the most important one of all.

AI-First: Impermanence by Design

Being LLM model agnostic is the only AI strategy that doesn’t age badly.

Only 25% of companies say AI is having a transformative effect, despite $250 billion invested globally in 2025. The WEF spent a year inside 50 of the world’s most advanced AI-first enterprises to find out why. The answer hits hard: 84% of companies haven’t redesigned jobs around AI at all. I break down the one building block most managers get dangerously wrong, and why betting on a single AI vendor is the 1970s IBM mainframe mistake dressed in new clothes.

Dive into the Knowledge Vaults — Start with a Free Read

Knowledge Vaults are your curated edge across six high-impact themes: AI, banking, CBDC/tokenization/payments, stablecoins, macrotrends, and Asia.

Every resource inside is hand-picked with only the highest-quality, most valuable material I uncover, no filler.

These vaults are living documents, updated weekly and expanding.

Premium members get exclusive access to all six Knowledge Vaults, and first access to everything added going forward.

New This Week in the Stablecoin Vault: Eight Uploads

New to the Stablecoin Vault this week: the stablecoin wars are no longer theoretical, and every bank, payments company, and fintech still in watch-and-wait mode is already behind. The three-way contest between stablecoins, CBDCs, and tokenized deposits is being decided right now, the Gulf is lapping the West on digital money infrastructure, and a $321 billion market is quietly dismantling the $40 billion annual revenue pool that correspondent banks have taken for granted for decades. You need to be inside this vault.

🔓 Every week I give members a free read of the first two articles.

Free to Read in the Vault

Stablecoins, CBDC, or Tokenized Deposits?

The real winner of the digital money race may be none of the above: a UNSW Law paper makes a brutal case for tokenized bank deposits, and JPMorgan is already calling its deposit token a superior alternative. If you’re building on stablecoin rails, you need to read this first.

The Gulf didn’t stumble into digital money. It engineered sovereign rails first and invited the private sector in second, with the UAE’s AE Coin already live in taxis, courts, and airlines and mBridge cutting cross-border settlement costs by up to 50%. Nobody else is building like this.

Read both free. Then decide if six vaults are worth it.

Click on the Vault link below👇

The Knowledge Vault: Stablecoins 2026

Knowledge Vaults are your curated edge across five high-impact themes: AI, banking, CBDC/tokenization/payments, stablecoins, and Asia.

Chart, Art, and Sponsor of the Day!

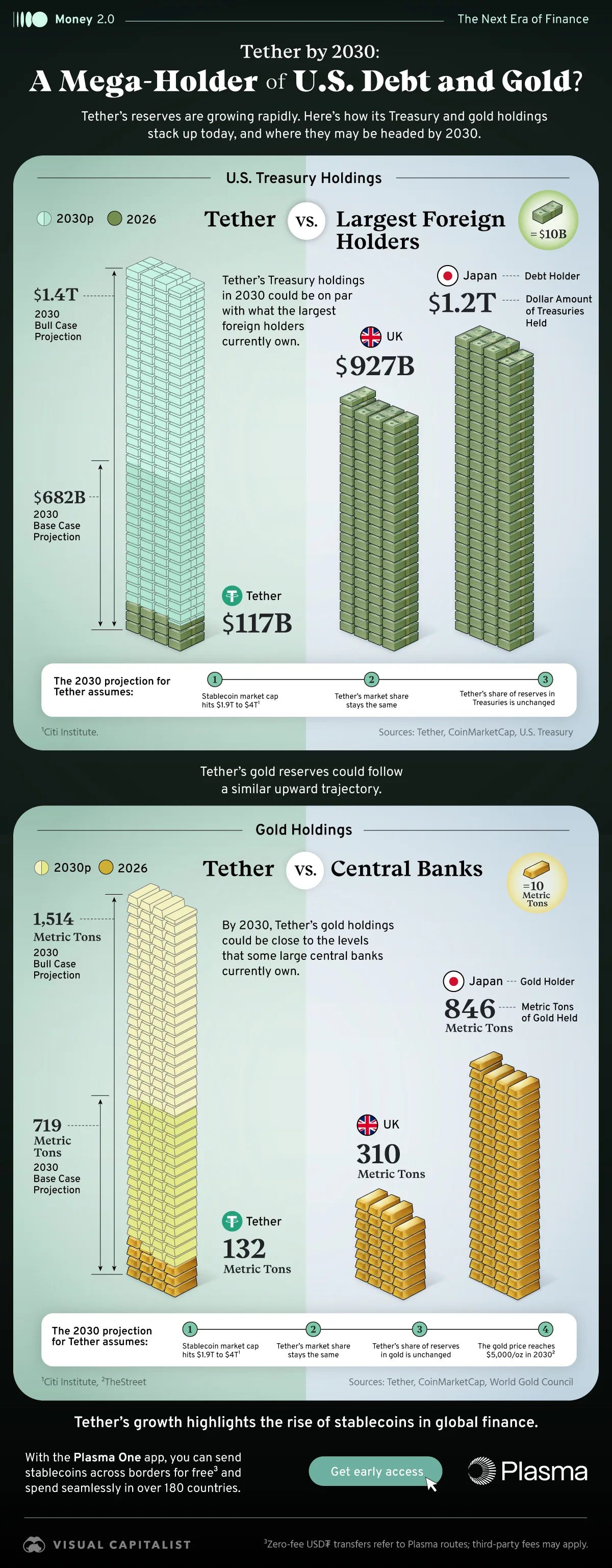

Chart of the Day ✦ Tether: 100 Employees, No Audit, and More U.S. Debt Than Most Nations. What Could Go Wrong?

Stablecoin advocates spent years telling us USDT would liberate us from the tyranny of Visa and Mastercard. What they built instead is a sovereign-scale reserve holder answerable to no central bank, no regulator, and no government, that won’t even get an audit.

The difference between Tether and the nations it’s catching up to is what the money is doing. A country’s reserves and a bank’s deposits are in motion, funding loans, trade, and economic growth.

Tether’s $117 billion sits parked in Treasuries, earning yield for its owners while contributing nothing to the real economy. In 2024 that yielded roughly $13 billion in profit, more than BlackRock, generated by around 100 employees. It’s the most profitable toll booth in financial history.

Banks and credit card companies are not sympathetic characters, but Tether makes them look like saints.

Tether currently holds $117 billion in U.S. Treasuries, already ahead of most sovereign holders

By 2030 base case, that grows to $682 billion, closing in on the UK’s $927 billion

Bull case hits $1.4 trillion, surpassing Japan as the largest foreign holder of U.S. debt

At $1.4 trillion, Tether would hold enough U.S. debt to move Treasury yields simply by buying or selling, with no Fed oversight and no accountability

Gold tells the same story: 132 metric tons today, potentially 1,514 metric tons by 2030, dwarfing the UK’s entire reserve of 310 metric tons

National reserves move. Bank deposits move. Tether’s assets sit still, at sovereign scale, with none of the oversight that comes with it

Sponsored by Backbase:

Cashless is proud to be brought to you by Backbase this month, and it’s a natural fit.

I’ve written for years about how legacy systems are the single biggest obstacle to AI adoption at banks.

Backbase offers something banks have been waiting for: a path to becoming AI-native institutions without ripping out their core systems.

Thank you to Backbase for supporting Cashless and its readers, who live at the intersection of AI and finance.

For more information, visit the Backbase website to learn more about their “AI-Native Banking OS that unifies your frontline.” HERE

Read my article on bank customer retention and why falling behind on AI is not an option when clients are ready to walk. I explain what options banks face, and why Backbase gives many banks the only sensible option to go AI-native.

Art of the Day: Decalcomania (The Transference), Rene Magritte, 1966

“Art evokes the mystery without which the world would not exist.” “It is not my intention to make anything comprehensible.” Rene Magritte

What you see: A man in a bowler hat and red curtain stand side by side. The curtain and the man seem to be mirror images of each other — the man’s silhouette is “transferred” onto the curtain, and vice versa. Through the gap where the man’s body should be opaque, you see the sea and sky beyond. His back is turned; we never see his face.

The core meaning — presence and absence: The painting is a meditation on what it means to be something. The man and the curtain occupy the same visual space, yet are interchangeable. What makes a person distinct from his surroundings? Magritte suggests: perhaps nothing. The boundary between self and world is arbitrary, even illusory.